Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send irs rollover chart via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out the IRS Rollover Chart with Our Platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the IRS Rollover Chart in the editor.

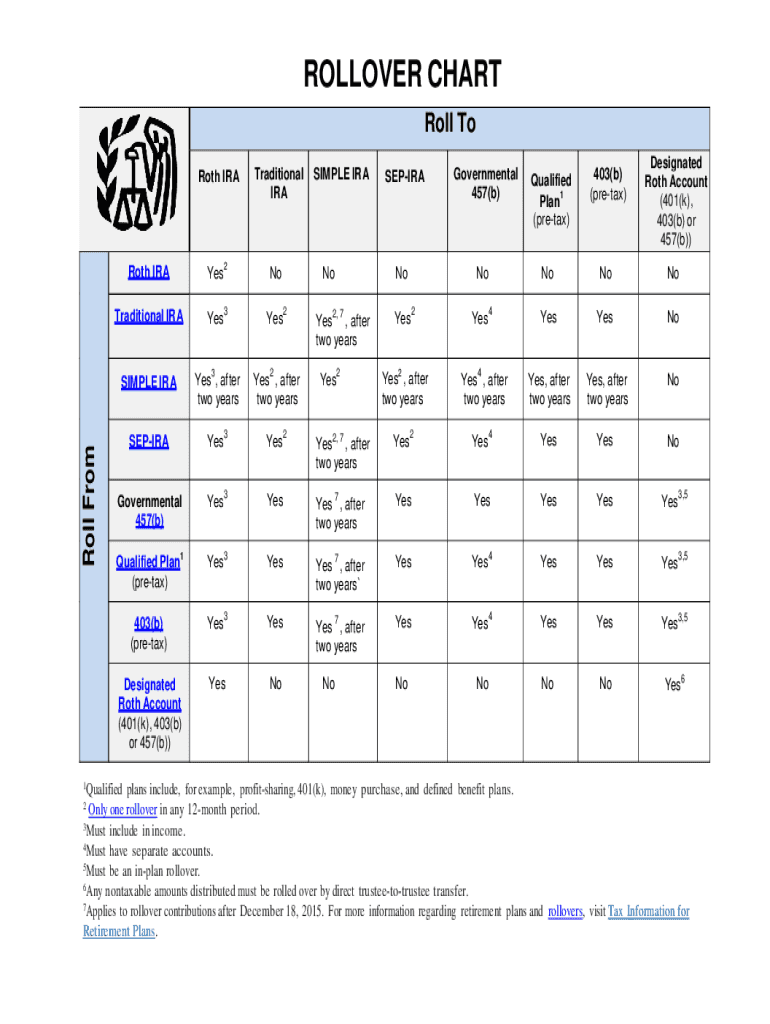

Begin by identifying the 'Roll From' and 'Roll To' columns. These sections indicate which types of retirement accounts can accept rollovers from others.

Locate the specific account types you are interested in, such as Roth IRA, Traditional IRA, or SIMPLE IRA. Each cell will indicate whether a rollover is allowed (Yes/No) and any conditions that apply.

Fill in your details based on your current retirement account type and the desired rollover destination. Use our platform's text fields to input any necessary information.

Review all entries for accuracy. Ensure that you understand any notes regarding timeframes or additional requirements, such as waiting periods for certain rollovers.

Start using our platform today to easily fill out your IRS Rollover Chart for free!

Direct rollover Funds are transferred directly from your old 401(k) plan to a new 401(k) plan or IRA without any immediate tax implications. Indirect rollover: Funds are distributed directly to you and then you deposit them into a new 401(k) plan or IRA within 60 days to avoid taxes and potential penalties.

What are the new rules for 401k in 2025?

Highlights of changes for 2025. The annual contribution limit for employees who participate in 401(k), 403(b), governmental 457 plans, and the federal governments Thrift Savings Plan is increased to $23,500, up from $23,000.

Where can I roll over my 401k without penalty?

If you have money in a designated Roth 401(k), you can roll it directly into a Roth IRA without incurring any tax penalties.

What is the 5 year rule for IRA rollover?

If your investing and tax strategy for retirement includes tax-advantaged Roth accounts, youve probably heard about the IRSs five-year rule. The simple version says the Roth account needs to have been funded for five years before you withdraw any earningseven after youve reached age 59or you could owe taxes.

What are the new rules for 401k withdrawals?

Financial emergencies: The SECURE 2.0 Act added this new exception in 2024 that allows one penalty-free retirement account distribution of up to $1,000 per year to cover emergency expenses. These are defined as unforeseeable or immediate financial needs relating to personal or family emergencies.

rollover chart

IRS rollover chart 2026Irs rollover chart pdfIrs rollover chart 2025IRS rollover rulesIrs rollover chart roth ira401k rollover to IRA401k rollover rules403b rollover into IRA

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

The easiest way to borrow from your 401(k) without owing any taxes is to roll over the funds into a new retirement account. You may do this when, for instance, you leave a job and are moving funds from your former employers 401(k) plan into one sponsored by your new employer.

What does the IRS consider a rollover?

A rollover occurs when you withdraw cash or other assets from one eligible retirement plan and contribute all or part of it, within 60 days, to another eligible retirement plan.

What is the time limit for an IRS rollover?

When should I roll over? You have 60 days from the date you receive an IRA or retirement plan distribution to roll it over to another plan or IRA. The IRS may waive the 60-day rollover requirement in certain situations if you missed the deadline because of circumstances beyond your control.

rollover chart irs

20 INTERNAL REVENUE CODE (IRC) LIMITS AND

LIMITS AND COMPARISON CHART Page. Eligible rollover in from another employers 403(b), 401(k) or governmental 457(b) plan. ROLLOVER DISTRIBUTIONS. Eligible

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.