Definition & Meaning

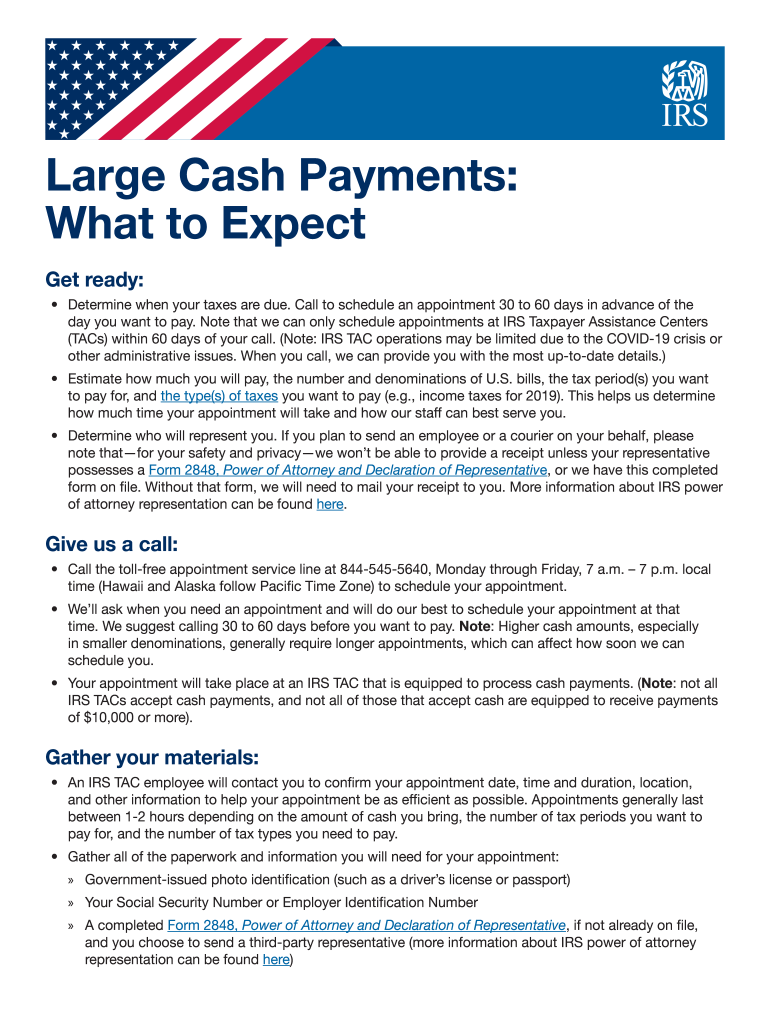

Publication 5436 (EN-SP) (8-2020), titled "Large Cash Payments," is an IRS publication designed to provide comprehensive guidance for individuals and businesses making significant cash transactions with the IRS. This publication helps taxpayers understand the procedures and documentation required to comply with federal regulations concerning large cash payments. It serves as an informational guide to ensure adherence to IRS mandates and legal obligations, thereby preventing potential penalties.

IRS Guidelines

IRS guidelines outlined in Publication 5436 (EN-SP) (8-2020) emphasize the importance of scheduling an appointment at a local Taxpayer Assistance Center for transactions involving large cash payments. Taxpayers should estimate payment amounts and prepare required documentation in advance to facilitate a smooth process. The publication advises taxpayers to bring acceptable forms of identification and all relevant tax documentation to the appointment. It also stresses the need for compliance with updated COVID-19 measures affecting in-person appointments, highlighting the IRS's commitment to health and safety.

Steps to Complete Publication 5436 (EN-SP) (8-2020)

- Schedule an Appointment: Contact your local IRS Taxpayer Assistance Center to arrange an appointment for large cash payments.

- Estimate Payment Amounts: Accurately calculate the amount you intend to pay to avoid discrepancies.

- Gather Necessary Documentation: Compile all necessary tax documents and personal identification required for the transaction.

- Attend the Appointment: Arrive on time with all documents prepared. Expect potential security and health protocols.

- Follow IRS Instructions: Ensure all forms and payments are processed as per IRS guidelines during the appointment.

Required Documents

When completing Publication 5436 (EN-SP) (8-2020), the following documents are essential:

- Valid government-issued identification

- Tax documents, such as tax returns and notices

- Documentation supporting the payment amount, like invoices or financial statements

- Correspondence from the IRS, if applicable

Who Typically Uses the Publication 5436 (EN-SP) (8-2020)

Taxpayers, both individuals and businesses, who need to make large cash payments to the IRS primarily use this publication. This includes corporations with significant tax liabilities, sole proprietors settling annual taxes, or any taxpayer settling sizable tax debts. Those with specific circumstances, such as inheritance tax payments or other non-standard financial situations, also benefit from this guide.

Key Elements of the Publication 5436 (EN-SP) (8-2020)

Publication 5436 (EN-SP) (8-2020) includes several critical components:

- Steps for scheduling appointments at IRS centers

- Procedures for estimating and confirming payment amounts

- Required documentation and identification for transactions

- Information on authentication and security measures during the payment process

Penalties for Non-Compliance

Failure to comply with the guidelines in Publication 5436 (EN-SP) (8-2020) can lead to penalties. These might include fines for late payments, additional interest on outstanding tax liabilities, and potential legal ramifications. It is crucial to follow all instructions meticulously to avoid these drawbacks.

Digital vs. Paper Version

Publication 5436 (EN-SP) (8-2020) is available in both digital and paper formats. The digital version can be accessed on the IRS website, providing ease of access and updates. For those who prefer a physical copy or lack digital access, the paper version can be requested from the IRS, ensuring that all taxpayers can utilize the publication regardless of their technological proficiency.

Software Compatibility

For taxpayers using software for tax preparation, such as TurboTax or QuickBooks, Publication 5436 (EN-SP) (8-2020) provides essential guidance to ensure their software aligns with IRS requirements for large cash transactions. Ensuring compatibility can streamline the process, making it easier to manage records and integrate payments with other financial activities.

Business Entity Types (LLC, Corp, Partnership)

Different business entities, such as LLCs, corporations, and partnerships, may have specific considerations when using Publication 5436 (EN-SP) (8-2020). These businesses must consider their structure's unique liability issues, cash flow mechanisms, and documentation requirements when making large cash payments to the IRS. Each entity type has distinct obligations, making it essential to understand the nuances detailed in the publication entirely.

Important Terms Related to Publication 5436 (EN-SP) (8-2020)

Several terms are crucial for understanding:

- Large Cash Transaction: Refers to any substantial cash payment made directly to the IRS.

- Taxpayer Assistance Center (TAC): An IRS office offering personalized assistance for tax-related queries and transactions.

- Payment Amount Estimate: A calculated projection of the amount required to settle tax liabilities.

Including these definitions ensures clarity and aids in comprehending the publication’s content effectively.

State-Specific Rules for Publication 5436 (EN-SP) (8-2020)

Publication 5436 (EN-SP) (8-2020) includes references to potentially varying state-specific requirements. While federal guidelines provide a baseline, taxpayers should also consider their state’s regulations concerning cash payments to ensure full compliance. This might involve consulting state revenue departments for additional instructions or constraints related to large cash transactions.