Definition & Meaning

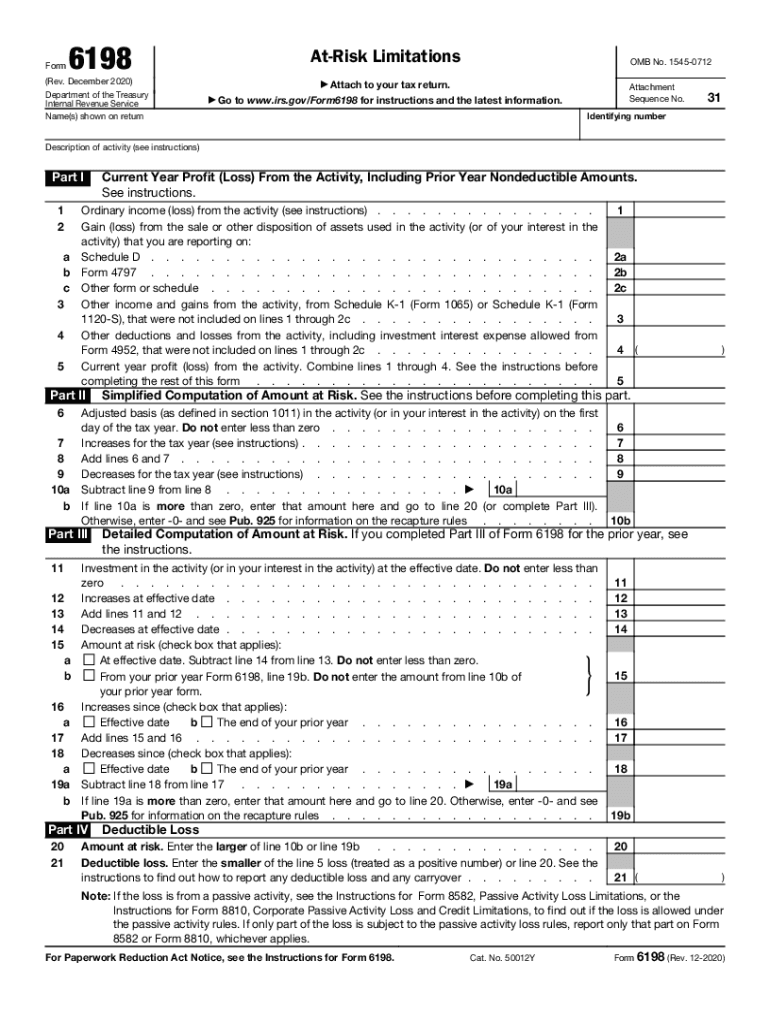

Form 6198, officially known as the "At Risk Limitations Form," is vital for taxpayers engaged in activities that might incur losses. Used by the Department of the Treasury and the Internal Revenue Service (IRS), this form calculates current-year profit or loss, detailing simplified and comprehensive computations of amounts at risk. It helps determine deductible losses and provides a structured method for reporting income, gains, deductions, and any passive activity loss limitations. The form is integral for ensuring compliance with IRS regulations and maintaining accurate financial records.

How to Use the 6198 At Risk Limitations Form

To use Form 6198 effectively, it is essential to understand its purpose and required sections. First, gather all related financial information about the specific activity or activities that incurred a loss. The form includes parts for entering profit or loss data and calculating amounts at risk. Accurate completion ensures you only deduct permissible losses, thereby aligning with IRS expectations. It is recommended that you consult with a tax professional if any section seems complicated to ensure correct filing.

Steps to Complete the 6198 At Risk Limitations Form

- Collect Necessary Documents: Gather documents that detail investment amounts, loans, and losses associated with at-risk activities.

- Enter Personal Information: Provide your name and taxpayer identification number.

- Calculate Current Year Profit or Loss: Fill out the section related to the financial activity’s gains or losses.

- Compute Amounts at Risk: Use the form's guidelines to determine your risk level in each activity.

- Review Passive Activity Limitations: Verify if any passive activity loss limitations apply.

- Consult a Professional if Needed: If complex issues arise, seek guidance from a tax advisor.

- Submit the Form: Once completed accurately, include the form in your tax return submission.

Who Typically Uses the 6198 At Risk Limitations Form

Individuals and entities involved in certain investment activities, partnerships, S Corporations, or sole proprietorships, often use Form 6198. It is particularly crucial for those engaged in at-risk financial ventures, where investments can generate taxable losses or gains. Understanding which business types require the form, such as partnerships and LLCs, and recognizing scenarios where losses may necessitate its use is essential for compliance and strategic tax planning.

IRS Guidelines

The IRS provides specific regulations regarding the use and completion of Form 6198. Tax filers must accurately report every detail about at-risk activities, including the amount invested and losses accrued. Adherence to IRS guidelines ensures the form's proper utilization and prevention of complications such as audits or penalties. Resources from the IRS site or consultation with tax professionals can offer additional insights into these guidelines.

Filing Deadlines / Important Dates

- Standard Tax Filing Deadline: Typically April 15, annually.

- Extensions Available: If required, a taxpayer may apply for an extension, commonly moving the deadline to October 15.

- Critical Review Periods: Ensure to periodically review your at-risk tax position before these dates to allow for any necessary corrections.

Required Documents

To complete Form 6198 successfully, you will need documentation related to your business or investment activities:

- Financial statements and balance sheets

- Previous tax returns

- Loan agreements or financial obligations linked to the activity

- Records of profit and loss statements for the current and past years

Each document should corroborate the entries you make on the form, validating your financial situations.

Penalties for Non-Compliance

Non-compliance with the requirements of Form 6198 can lead to severe repercussions. These may include financial penalties, additional taxes, and potential audits. Failure to accurately disclose at-risk activities or incorrect computations of risks can trigger IRS scrutiny. Being aware of these risks underscores the importance of accuracy and timely submission of the form.

Software Compatibility (TurboTax, QuickBooks, etc.)

Several software solutions, such as TurboTax and QuickBooks, support the completion and submission of Form 6198. These tools offer guided entry options, helping to ensure accuracy by checking calculations and data entry. They also provide reminders about upcoming deadlines and allow integration with other financial records, which simplifies the process of gathering and organizing necessary documentation. Leveraging technology enhances efficiency and helps meet IRS requirements with precision.