Definition and Meaning of 1120 IC-DISC Commission

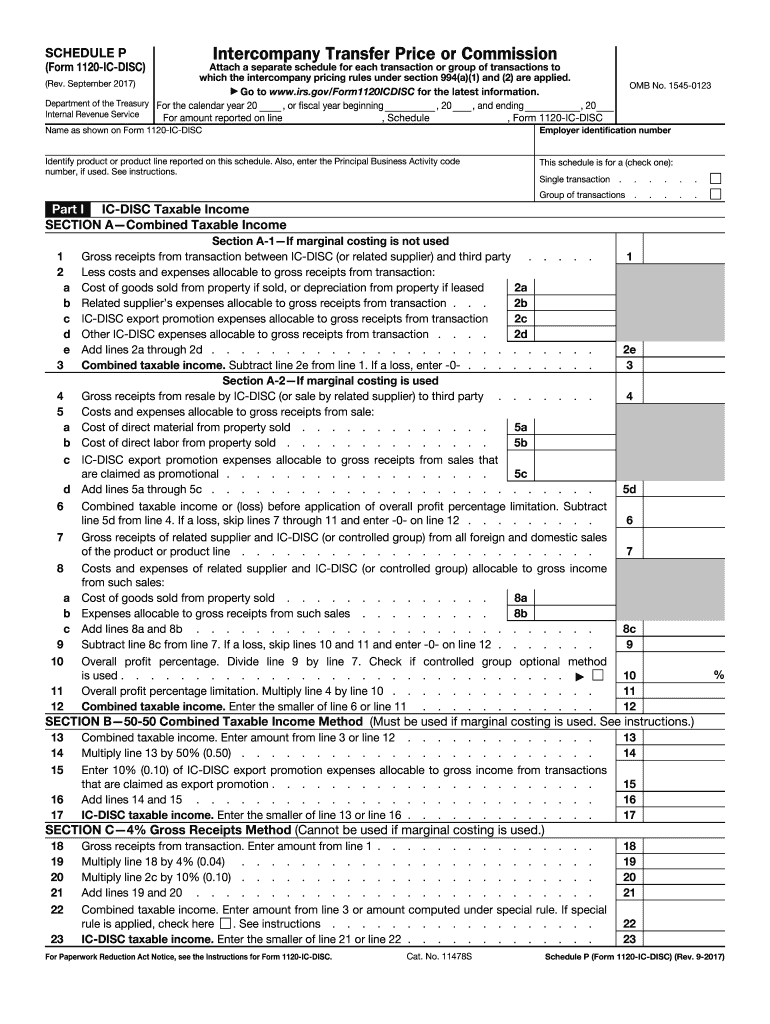

The 1120 IC-DISC Commission pertains to a U.S. tax mechanism that allows certain types of corporations to achieve tax savings by exporting goods or services. The term IC-DISC refers to an "Interest Charge Domestic International Sales Corporation," a special type of corporate entity designed to facilitate the deferral of certain export income to reduce current U.S. tax liability. The 1120 IC-DISC Commission is reported via Schedule P (Form 1120-IC-DISC), which documents transactions for pricing or commissions concerning exports.

Key Features and Benefits

- Tax Deferral: Provides a legal way to defer income tax on export earnings.

- Export Incentives: Encourages U.S. businesses to increase their exports, benefiting from tax reductions or deferrals.

- Eligible Corporations: Primarily targets manufacturers, distributors, and brokers who export U.S. goods or services.

Steps to Complete the 1120 IC-DISC Commission

Filing Schedule P (Form 1120-IC-DISC) involves several detailed steps. A company must follow these carefully to ensure compliance with IRS requirements.

-

Collect Transaction Data:

- Determine all transactions eligible for commission deferral or cost computation.

- Ensure detailed records of intercompany pricing and commissions related to exports.

-

Calculate Commissions:

- Utilize the appropriate pricing methods such as marginal costing.

- Report commission calculations for each transaction or related group.

-

Detail Gross Receipts and Costs:

- List gross receipts derived from eligible export sales.

- Document related costs and expenses to compute the taxable income accurately.

Common Mistakes to Avoid

- Incorrect Calculations: Double-check computations to prevent errors in taxable income reporting.

- Incomplete Transaction Records: Ensure all relevant transactions are thoroughly documented and included.

Required Documents for 1120 IC-DISC Commission

Accurate and complete documentation is crucial when filling out Form 1120-IC-DISC. Businesses should prepare several key documents:

Essential Documents

- Transaction Records: Include all export-related sales and commission agreements.

- Financial Statements: Provide comprehensive income statements and balance sheets.

- Cost Analysis: Detail the costs associated with production and sales of export goods.

IRS Guidelines for 1120 IC-DISC Commission

The Internal Revenue Service (IRS) stipulates specific rules and guidelines for the 1120 IC-DISC commission process. Understanding these can help ensure compliance.

Key Aspects

- Eligibility Requirements: Understand which businesses qualify to establish an IC-DISC.

- Tax Rate Reductions: Be aware of potential reductions in qualified dividends resulting from IC-DISC commissions.

- Compliance Obligations: Follow the IRS’s procedural guidelines to avoid penalties.

Filing Deadlines and Important Dates

Timeliness is critical when filing for 1120 IC-DISC commissions to avoid penalties and ensure proper tax deferral benefits.

- Yearly Deadline: Generally, IC-DISC returns are due by the 15th day of the 9th month following the end of the tax year.

- Extension Options: Corporations can apply for an extension to extend filing deadlines if additional time is required.

Common Examples of Using the 1120 IC-DISC Commission

Understanding practical applications can clarify how the 1120 IC-DISC commission functions across various industries.

Industry Applications

- Manufacturing Sector: Large-scale manufacturers exporting machinery or technology may establish IC-DISCs to defer taxes on international revenue.

- Wholesale Distributors: Those distributing U.S.-produced goods abroad can leverage the commission arrangements for better financial efficiency.

Who Typically Uses the 1120 IC-DISC Commission

This filing mechanism is primarily utilized by specific types of business entities engaged in exporting activities.

Eligible Businesses

- C Corporations: Often leverage IC-DISC for reduced taxable income on export profits.

- Partnerships and LLCs: If structured properly, they can also benefit from IC-DISC regulations to optimize tax outcomes associated with export activities.

Penalties for Non-Compliance with 1120 IC-DISC Commission

Failure to comply with the requirements of filing the 1120 IC-DISC form can result in substantial financial repercussions.

Potential Penalties

- Late Filing Fees: Penalties accrue rapidly for missing submission deadlines.

- Audit Risks: Non-compliance can trigger IRS audits, leading to further scrutiny of the entity's finance operations and potential additional penalties.

Understanding these factors is essential for businesses aiming to leverage the 1120 IC-DISC commission effectively and legally. Proper management of this tax advantage requires rigor and adherence to IRS guidelines to ensure maximum benefit and compliance.