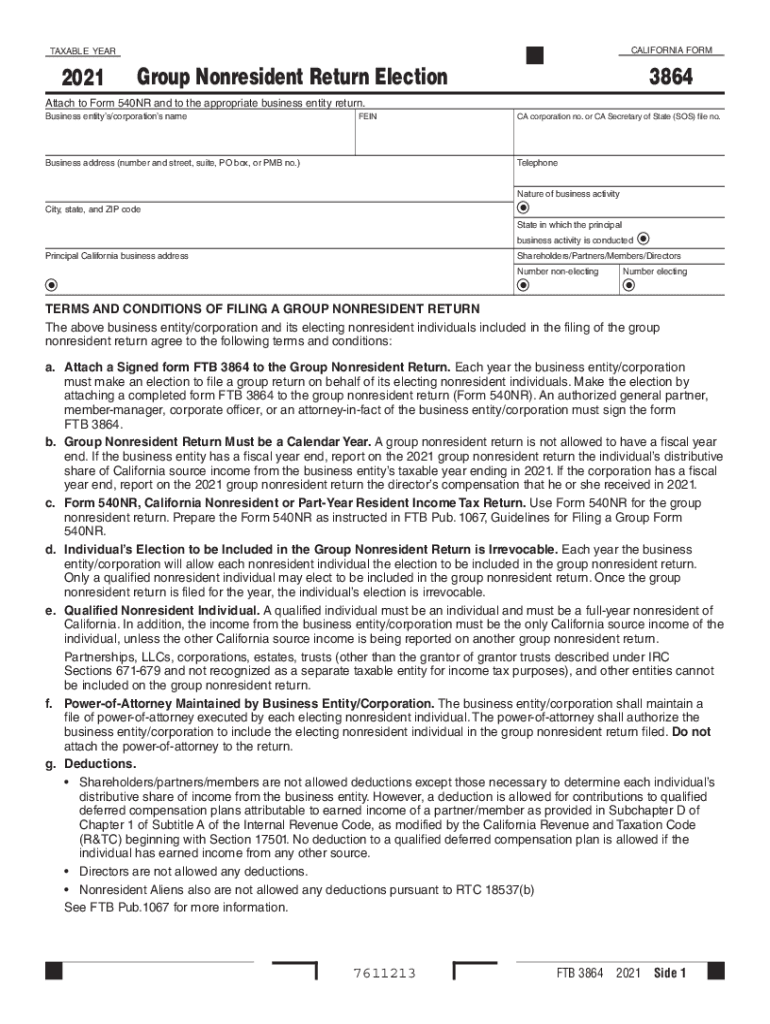

Definition & Meaning

The California Group Nonresident Tax Return, filed through FTB.ca.gov, facilitates the collective filing of income tax returns for nonresident individuals who have income sourced in California. This form is typically used by business entities that elect to file a group nonresident return on behalf of their nonresident partners, members, or shareholders. By consolidating individual returns into a single form, the process is streamlined, allowing for efficient compliance with state tax laws.

How to Use the California Group Nonresident Tax Return

Utilizing the California Group Nonresident Tax Return involves several steps to ensure proper filing. Business entities must first confirm the eligibility of their nonresident participants and gather all pertinent income data. The form is completed by providing comprehensive details about the entity and income distributions among members. Once filled out, it is submitted through the Franchise Tax Board's website. It's crucial to follow the instructions carefully to avoid any errors that could delay processing or lead to penalties.

Steps to Complete the California Group Nonresident Tax Return

- Verify Eligibility: Ensure that all participating nonresident individuals meet the criteria for inclusion in a group filing.

- Compile Income Data: Gather all necessary income and tax information for each electing individual.

- Fill Out the Form: Complete the form with accurate details on income allocation and any applicable deductions.

- Review for Accuracy: Double-check the information to ensure there are no discrepancies.

- Submit via FTB: File the completed form electronically through the FTB website by the specified deadline.

Important Terms Related to California Group Nonresident Tax Return

- Nonresident Individual: A person who resides outside California but earns income from California sources.

- Election: The decision by a business entity to file a group return on behalf of nonresident participants.

- Withholding Agent: The business entity responsible for withholding taxes on behalf of nonresident partners or shareholders.

Filing Deadlines / Important Dates

Just like any tax form, the California Group Nonresident Tax Return must be filed by the designated deadline to avoid penalties. Typically due by April 15th, extensions may be available but must be applied for before this date. Entities are advised to stay informed about potential changes in deadlines, especially in unusual circumstances like natural disasters or changes in tax legislation.

Required Documents

- Form 1065 or 1120-S: These federal forms report income, deductions, and credits of the entity.

- Schedules K-1: These forms list the income allocated to each partner or shareholder.

- Supporting Income Documents: Any relevant documentation that provides proof of income distribution and taxes withheld.

Penalties for Non-Compliance

Failure to file the California Group Nonresident Tax Return on time or inaccuracies within the form can lead to significant penalties. These may include late filing penalties, interest on unpaid taxes, and possible additional fines. Ensuring compliance through accurate filing and timely submission protects the entity from these punitive measures.

Who Typically Uses the California Group Nonresident Tax Return

This form is primarily used by partnerships, corporations, and LLCs that have nonresident partners, members, or shareholders. These entities leverage the form to consolidate the filing process, making it more efficient for managing group returns. This practice is common among businesses with extensive operations in California that involve nonresident investors.

Examples of Using the California Group Nonresident Tax Return

Consider a corporation with nonresident investors from various states. By using the California Group Nonresident Tax Return, the corporation can file a single group return, consolidating the tax obligations of all nonresident investors. This reduces the administrative burden and ensures compliance with California's tax laws efficiently and effectively.