Definition and Meaning

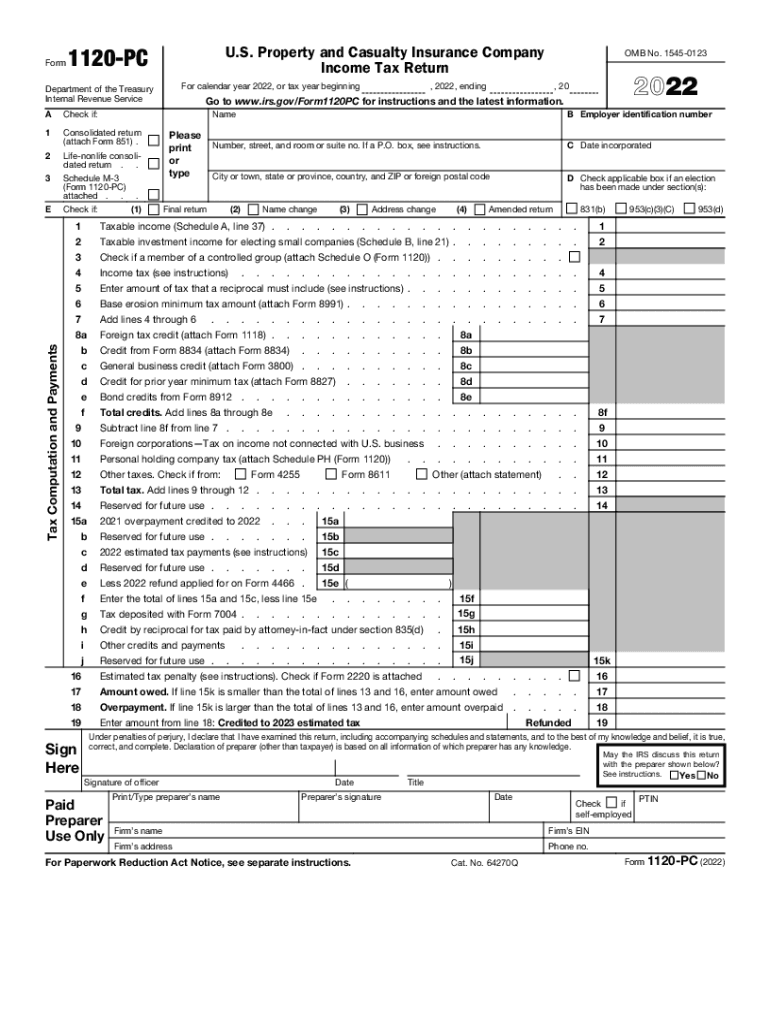

The Form 1120-PC, U.S. Property and Casualty Insurance Company Income Tax Return, is a federal tax form used by U.S.-based property and casualty insurance companies. This form allows such companies to report their taxable income, compute taxes owed, and provide necessary details to the Internal Revenue Service (IRS) for compliance with tax regulations. It includes sections for reporting crucial financial data such as premiums earned, losses incurred, and dividends received. Understanding the specific elements of this form is essential for any returns filed for the taxable year, ensuring they meet legal and fiscal obligations.

How to Use the Form 1120-PC

Using Form 1120-PC involves several steps to collect and accurately input data. Companies must gather detailed records of their financial transactions for the reporting year. This includes premiums collected, claims paid, and other relevant financial activities. The form is structured to guide the reporting of this information systematically. Precise figures must be entered in designated fields to avoid discrepancies. Reviewing this information by a financial expert or accountant is advisable, as incorrect data may lead to penalties or audits.

Steps to Complete Form 1120-PC

- Gather Financial Documents: Ensure access to comprehensive financial records, including receipts for premiums and documentation of claims.

- Fill Out the Sections: Enter data accurately in the form’s sections, which cover income, deductions, and tax computation.

- Review for Accuracy: Double-check entries for any potential errors.

- Consult a Professional: Seek advice from a tax professional if needed.

- Submit and Retain Copies: File the form by the IRS deadline and keep copies for future reference.

Who Typically Uses Form 1120-PC

Property and casualty insurance companies primarily use this tax form. These companies include those that offer various types of insurance, such as automobile, home, and liability insurance. The form can also be used by organizations that underwrite non-standard policies like earthquake or flood insurance. It is crucial for these organizations to adhere to this form for accurate federal tax reporting, thereby ensuring compliance with IRS mandates.

Key Elements of the Form 1120-PC

Form 1120-PC includes several core components that aid in reporting the financial status of an insurance company:

- Income Section: Documents all income generated from underwriting and investment activities.

- Deductions: Outlines eligible deductions such as losses incurred and operational expenses.

- Tax Computation: Establishes the total tax liability after all deductions and credits have been applied.

Important Terms Related to Form 1120-PC

- Premiums Earned: Total revenue from insurance policies sold.

- Losses Incurred: Expenses related to claims paid out during the fiscal year.

- Retained Earnings: Profits not distributed as dividends and reinvested back into the company.

IRS Guidelines

The IRS provides specific guidelines to file Form 1120-PC correctly. These regulations include instructions on calculating taxable income, allowable deductions, and tax credits pertinent to insurance companies. Adhering to these guidelines ensures compliance, minimizing risks of penalties. The IRS updates these guidelines periodically, so companies should stay informed about any changes to maintain accurate filings.

Filing Deadlines and Important Dates

Typically, Form 1120-PC must be filed by the 15th day of the fourth month after the end of the tax year. For most companies using a calendar year, this deadline falls on April 15. Filing extensions may be available; however, companies need to meet requirements and file requests promptly to avoid late fees or penalties.

Penalties for Non-Compliance

Failure to comply with filling and submission of Form 1120-PC can result in significant penalties. These may include fines based on the unreported tax amount or daily charges for delayed submissions. Additionally, the IRS could impose interest on unpaid taxes if late filings affect the timely payment. Companies should diligently adhere to filing schedules and instructions to prevent non-compliance repercussions.

Software Compatibility

Various tax software platforms, such as TurboTax and QuickBooks, can assist insurance companies in preparing and filing Form 1120-PC. These platforms offer tools to simplify data entry, automate calculations, and e-file directly with the IRS. Using such software can minimize human errors and streamline the filing process, especially for companies handling complex financial transactions.

State-Specific Rules

While Form 1120-PC is a federal tax form, insurance companies must be aware of state-specific tax regulations and reporting requirements. Different states might have varying guidelines regarding deductible expenses or tax rates. Thus, companies should familiarize themselves with these rules and consider consulting state taxation authorities or professionals to ensure their federal and state tax submissions do not conflict.

Providing in-depth, structured guidance on Form 1120-PC ensures that U.S. Property and Casualty Insurance Companies meet compliance obligations and effectively manage their tax-related tasks.