Definition and Purpose

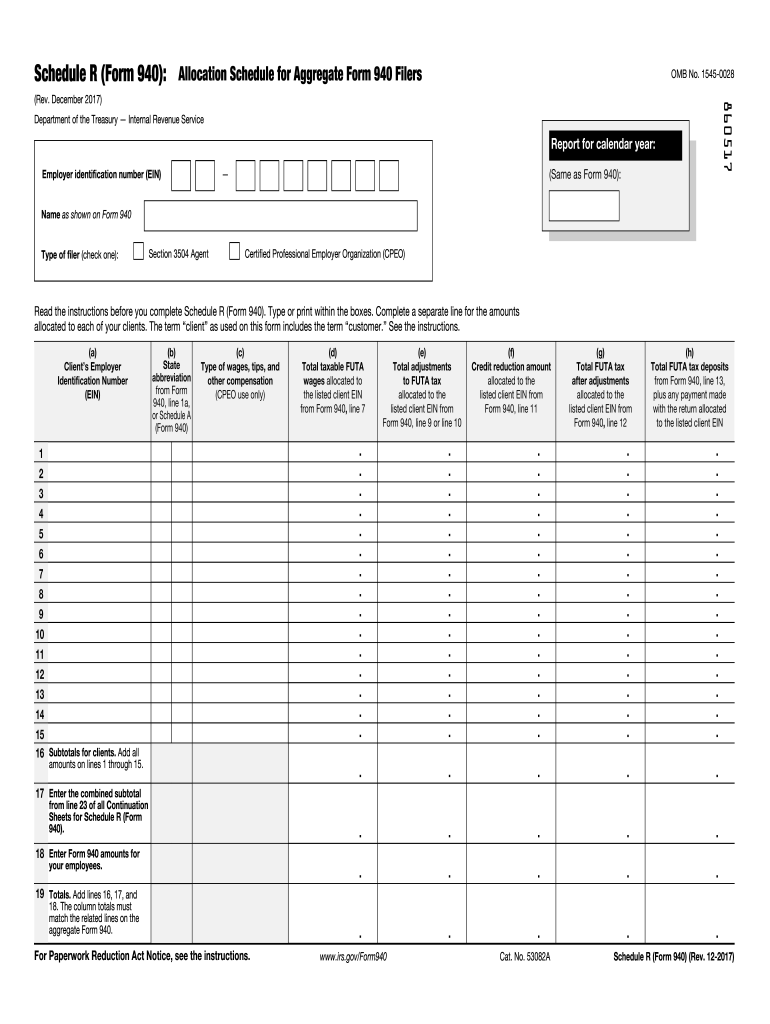

Schedule R (Form 940) is an essential tool for aggregating Form 940 filers. This form is typically used by agents representing multiple entities, such as home care service providers, to allocate the necessary financial information reported on the aggregate Form 940, known as the Employer's Annual Federal Unemployment Tax Return. This allocation includes crucial detail requirements like employer identification numbers (EINs) of clients, taxable wages subject to the Federal Unemployment Tax Act (FUTA), adjustments to the FUTA tax, and total tax deposits. Each layer of financial data is pivotal in ensuring that the tax burden is distributed accurately across clients for whom the agent files Form 940. The Schedule R must be submitted annually in conjunction with the aggregate Form 940. Keeping these details correct aids in maintaining compliance and facilitates accurate record-keeping for associated entities.

How to Use Schedule R

Utilizing Schedule R involves several key steps. The process starts with gathering the necessary employee and wage data from each client under the agent’s authority using their respective EIN. Follow these steps:

- Collect Data: Ensure all necessary information regarding taxable FUTA wages and tax adjustments are in order.

- Client Allocation: Assign these figures accurately to the respective clients being represented.

- Verify Information: Double-check all entries for accuracy to avoid IRS discrepancies.

- Submit with Form 940: Attach Schedule R to the completed Form 940 before submission to the IRS.

Thorough completion ensures each entity is appropriately represented, mitigating potential liabilities.

Obtaining Schedule R

Accessing Schedule R is straightforward and can be done through several methods:

- IRS Website: Download directly from IRS.gov in the forms and publications section.

- Tax Software Providers: Many online tax services integrate these forms for ease of completion.

- Professional Services: Accountants and tax professionals typically provide these forms and assist in their completion.

Having quick access to the necessary forms ensures that agents can prepare the required documentation without delays, maintaining compliance with federal deadlines.

Completing Schedule R

Filling out Schedule R requires diligence and attention to detail:

- Enter Aggregate Employer Information: Include primary agents' details and aggregate wages.

- Distribute Employee Wages: Allocate wages, adjustments, and tax deposits to the correct client EIN.

- Calculate Tax Liabilities: Use precise financial data to calculate each entity’s FUTA tax contribution.

- Review and Confirm Details: Ensure all fields match the clients’ financial records to prevent errors with the IRS.

- Attach Proper Documentation: Confirm that all supporting documents are attached before filing.

Adhering to these steps limits errors and ensures a smooth filing process.

Eligibility and Typical Users

Schedule R is intended for agents, particularly those in payroll or employment services, who report on behalf of multiple clients. Primary users include:

- Third-party payroll processors: Entities managing payroll tasks for other companies.

- Home care agencies: Organizations overseeing employment taxes for individual care recipients.

- Professional Employment Organizations (PEOs): Providing various employee management services, including tax filing.

These users leverage Schedule R to allocate tax burdens in a manner consistent with IRS requirements.

Key Elements of Schedule R

The form includes several essential components:

- Client EINs: Identification numbers for each entity on whose behalf taxes are filed.

- Wage Allocations: Details specifying each client's taxable and total wages.

- FUTA Adjustments: Any changes in tax liabilities or credits applicable.

- Deposit Details: Records of taxes deposited on behalf of each client.

Accurate entry of these elements is critical to fulfill federal obligations and ensure compliance.

Filing Deadlines and Important Dates

The Schedule R must align with Form 940’s deadlines:

- Annual Filing: Due by January 31 of the year following the reporting tax period.

- Postmarked Date: If mailed, ensure it is postmarked by January 31.

- Online Submissions: Must be completed by the deadline via IRS-approved e-file providers.

Agents should remain vigilant regarding these deadlines to avoid penalties for late submissions.

Penalties for Non-Compliance

Failing to file Schedule R correctly can result in notable repercussions:

- Monetary Fines: Inconsistent or late filings may incur IRS penalties.

- Increased Scrutiny: Untimely filing increases the likelihood of audits or further investigation.

Maintaining timely and accurate submissions helps avoid these penalties and supports compliant financial management.