Definition and Meaning

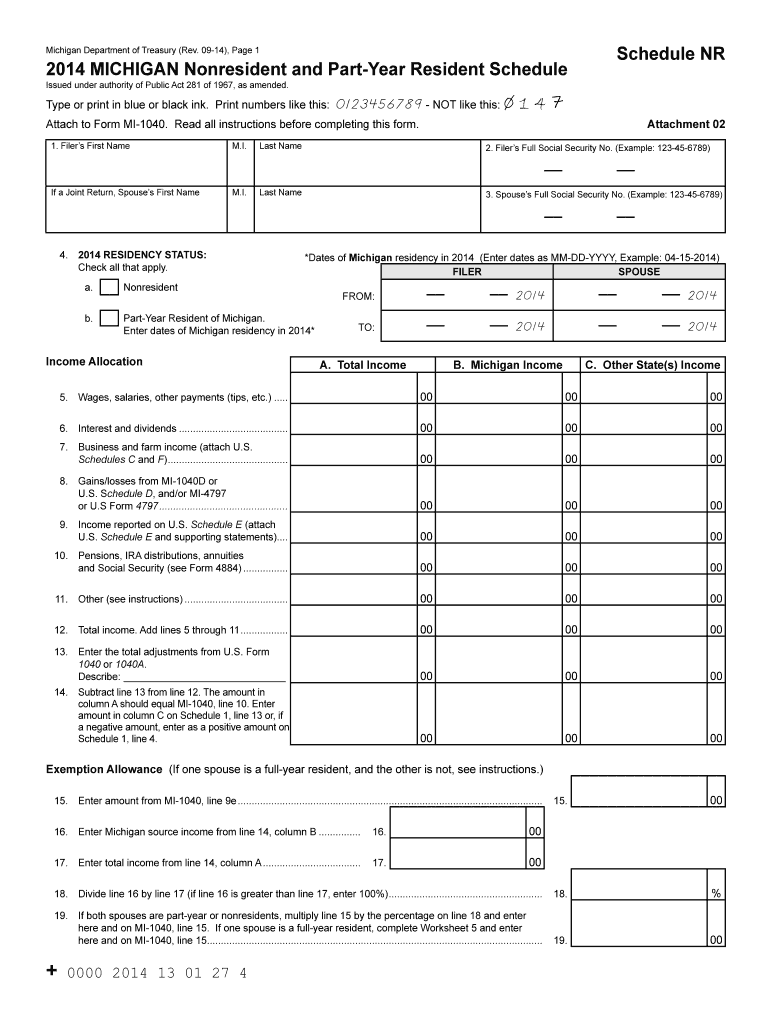

Business and farm income refers to the earnings derived from business activities and agricultural operations that need to be reported for tax purposes. This category of income is typically included in your federal and state tax returns and is critical for determining your overall tax liability. Understanding the specifics of how this income is categorized and reported can help optimize your tax outcomes.

- Business Income: Includes profits from selling goods or services, rents, royalties, and any other income generated from your business operations.

- Farm Income: Covers earnings from farming activities such as livestock, crop production, and any related agricultural services.

Properly classifying these income types ensures that deductions are accurately applied, and tax credits are appropriately claimed.

How to Use the Form

Understanding how to utilize the form "Business and Farm Income (Attach U)" is crucial for accurate income reporting and tax compliance. This form is typically used to:

- Document both the income and expenses associated with your business and farm operations.

- Calculate the taxable income derived from these activities.

- Ensure compliance with federal and state tax guidelines by attaching it to your regular tax forms.

To use this form effectively, gather all relevant financial records, such as sales receipts, expense invoices, and bank statements. This documentation will support the figures you report and streamline the filing process.

Steps to Complete the Business and Farm Income Form

Filling out the "Business and Farm Income (Attach U)" form requires careful attention to detail. Follow these steps for a thorough completion:

- Collect Financial Records: Gather all documentation related to your business and farm income and expenditures.

- Enter Income Details: Record the total income from business and farm operations, making sure to categorize it under the appropriate sections.

- Document Expenses: Itemize deductible expenses incurred during your business and farming activities, such as equipment costs, supply purchases, and operational expenses.

- Calculate Totals: Compute the net income by subtracting total expenses from total income.

- Verify Information: Double-check all entries for accuracy to prevent audit-triggering anomalies.

- Attach to Tax Return: Ensure the completed form is annexed to your personal or business tax return before submission.

Each of these steps is critical for accurate reporting and maximizing applicable deductions.

Who Typically Uses the Form

The "Business and Farm Income (Attach U)" form is typically used by individuals and entities engaged in business or agricultural operations. This includes:

- Self-Employed Individuals: Owners of small businesses who report income and expenses directly on their tax returns.

- Farmers and Ranchers: Operators of agricultural enterprises of varying scales.

- Business Partnerships: Partnerships reporting income shared between partners.

- Limited Liability Companies (LLCs): Business entities that opt for pass-through taxation where business income is reported on personal tax returns.

These users benefit from understanding the form's requirements to ensure comprehensive income reporting.

Key Elements of the Business and Farm Income Form

The form includes several critical sections that must be attentively completed:

- Income Section: This segment is dedicated to reporting all business and farm revenue streams.

- Expense Deduction Section: Here, you itemize all qualifying expenses and deductions related to your operations.

- Net Profit Calculation: This part determines the taxable income after deductions.

- Certification: A declaration ensuring all the information provided is true and correct.

Accurate data entry in these sections is essential for minimizing errors and optimizing tax savings.

IRS Guidelines

The IRS provides comprehensive guidelines on how to report business and farm income. Fundamental elements include:

- Record-Keeping Requirements: Maintaining detailed and organized records for all income and expenses is crucial.

- Form Attachments: The form must be appended to the appropriate sections of your federal and state tax returns.

- Deduction Limits: Adhering to rules on deductible expenses is vital for compliance and avoiding penalties.

Familiarize yourself with IRS publications to ensure you meet all reporting requirements.

Required Documents

Before completing the "Business and Farm Income (Attach U)" form, gather all necessary documentation to support your entries:

- Expense Receipts: These provide evidence of deductible expenses.

- Bank Statements: Offer proof of cash flows related to business activities.

- Sales Invoices: Important for accurate recording of income.

- Lease Agreements: If relating to business properties or farm equipment.

Having these at hand will facilitate efficient and precise form completion.

Penalties for Non-Compliance

Failing to properly report business and farm income can lead to several repercussions, including:

- Fines and Interest: Underreporting income or claiming false deductions can result in financial penalties.

- Audit Risks: Incorrect or incomplete filings increase the likelihood of an IRS audit.

- Legal Consequences: Continued non-compliance may lead to more severe legal action.

Comprehensively and accurately completing the form minimizes these risks and fosters a smooth tax filing process.