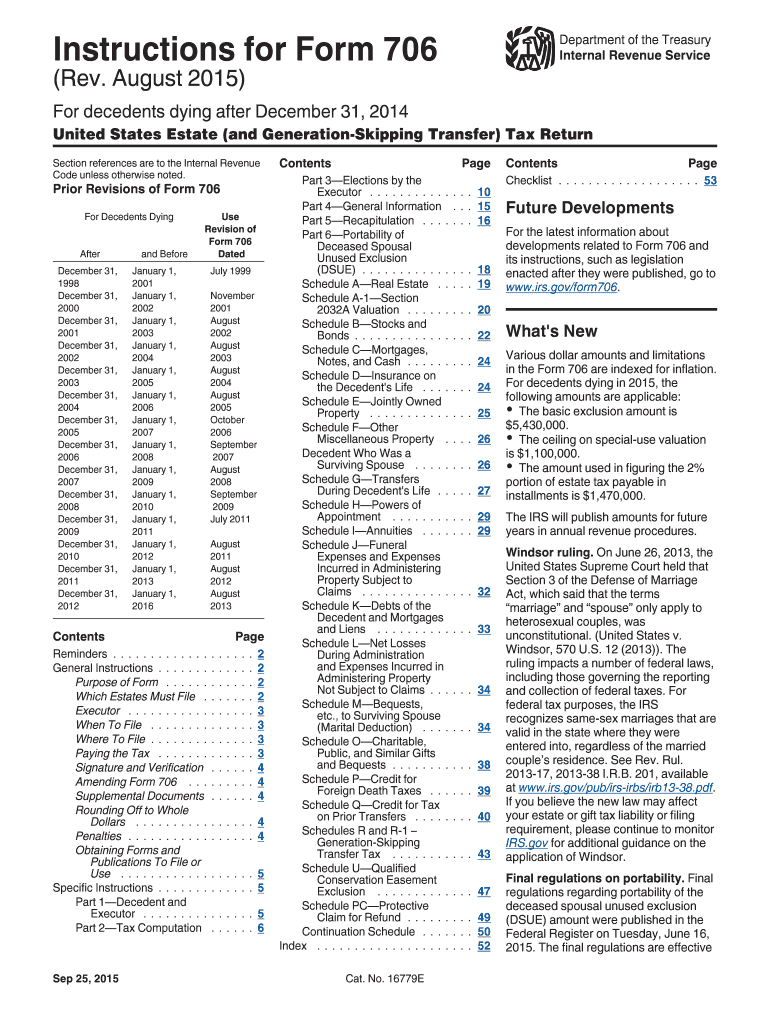

Definition and Meaning of 2015 Form 706

The 2015 Form 706, officially known as the United States Estate (and Generation-Skipping Transfer) Tax Return, is used by executors or administrators to report the estate of a deceased person. This form is specifically applicable for individuals who passed away after December 31, 2014. It provides a comprehensive outline for reporting and computing the due taxes on the transferred estate, including properties and assets, both tangible and intangible. The primary purpose of this document is to determine the estate and any potential generation-skipping transfer taxes owed to the federal government.

Key Components of the Form

- Estate Valuation: It includes valuations for real estate, investments, businesses, and other tangible or intangible assets. Understanding the fair market value is critical for accurate reporting.

- Deductions: This covers expenses such as funeral costs, charitable contributions, and debts owed by the decedent, which can reduce the taxable estate.

- Tax Computation: Detailed sections help calculate the appropriate estate taxes, considering credits and deductions available.

How to Use the 2015 Form 706

The use of Form 706 is primarily by executors tasked with administering a decedent's estate. Here's how it broadly applies:

- Gather Required Information: Start by compiling all necessary documents regarding the decedent's financial details.

- Asset Inventory: An extensive inventory of all assets must be conducted, ensuring they're correctly valued.

- Data Entry: Input data concerning the estate's assets, liabilities, and financial transactions during the tax year in question.

- Filing the Form: After completion, file the form according to IRS guidelines to avoid penalties and ensure compliance.

Filing Tips

- Accuracy Is Key: Double-check values and figures to avoid errors.

- Seek Professional Help: Given the complexity, enlisting a tax professional or attorney is advisable to navigate the process smoothly.

How to Obtain the 2015 Form 706

Acquiring the 2015 Form 706 is straightforward. Here's how:

- From the IRS Website: The form can be downloaded directly and printed from the official Internal Revenue Service site.

- From a Tax Professional: Most CPAs, tax preparers, and estate attorneys can provide a copy.

- IRS Office: Visit local IRS offices for a physical copy.

Direct Download and Printing

Accessing the form online requires reliable internet to ensure the form is printed clear and legibly. Most internet browsers allow users to print the form directly after downloading.

Steps to Complete the 2015 Form 706

Completing Form 706 requires careful precision and understanding:

- Complete Personal Details: Include information about the decedent and executor, including SSNs and domicile state.

- Schedule Fillings: Follow the instructions for each schedule related to the assets reported, like Schedule A for real estate.

- Compute Taxes: Use the tax computation section to determine tax owed.

- Review and File: Finalize the form by reviewing all sections for completeness before submitting to the IRS.

Recommendations for Filing

- Use Tax Software: Consider using tools like TurboTax for completing complex calculations accurately.

- Deadline Awareness: Stay informed about filing deadlines to avoid penalties.

Who Typically Uses the 2015 Form 706

Executors of estates primarily use Form 706 when the estate's total asset value exceeds the estate tax exemption limit, which was $5.43 million in 2015. This group usually includes:

- Estate Attorneys: Handling formal responsibilities on behalf of the family or beneficiaries.

- Family Members: Often a spouse or relative designated as the executor of the estate.

- Professional Executors: Individuals appointed by the decedent in their will to manage asset distribution and tax obligations.

Important Terms Related to 2015 Form 706

Understanding key terms related to Form 706 is crucial for correct completion:

- Decedent: The individual who has passed away.

- Executor: Person responsible for managing the decedent’s estate.

- Generation-Skipping Transfer (GST) Tax: A tax on transfers of property to beneficiaries who are at least two generations younger than the decedent, like grandchildren.

- Gross Estate: The total value of all assets before deducting liabilities.

Real-World Context

These terms highlight responsibilities for the person handling tax compliance, ensuring the estate is managed according to federal regulations.

IRS Guidelines for Filing

IRS guidelines are essential for successfully completing Form 706:

- Documentation: Maintain verifiable records for all reported values and deductions.

- Compliance: Adhere strictly to IRS instructions provided with the form.

- Key Dates: Ensure filings are completed within a nine-month period after the decedent's death unless an extension is granted.

Practicing Diligence

Following IRS procedural tips can help avoid common pitfalls that lead to penalties and legal issues related to estate processing.

Filing Deadlines and Important Dates

Understanding critical deadlines for Form 706 is paramount:

- Initial Deadline: Submit the form and payment within nine months following the decedent's death.

- Extension Options: Executors can request a six-month filing extension if necessary.

Importance of Timely Filing

Meeting deadlines minimizes the risk of incurring interest and penalties on overdue taxes, maintaining the estate's financial health and compliance.

Penalties for Non-Compliance

Failure to comply with IRS regulations regarding Form 706 can result in significant penalties:

- Monetary Fines: Based on the underpayment of the estate or generation-skipping tax.

- Legal Repercussions: Potential for legal actions to recover owed taxes, impacting beneficiaries and heirs.

Avoiding Common Mistakes

Diligence in reviewing the form and understanding the IRS guidelines and thresholds can prevent missteps leading to penalties.