Definition and Meaning

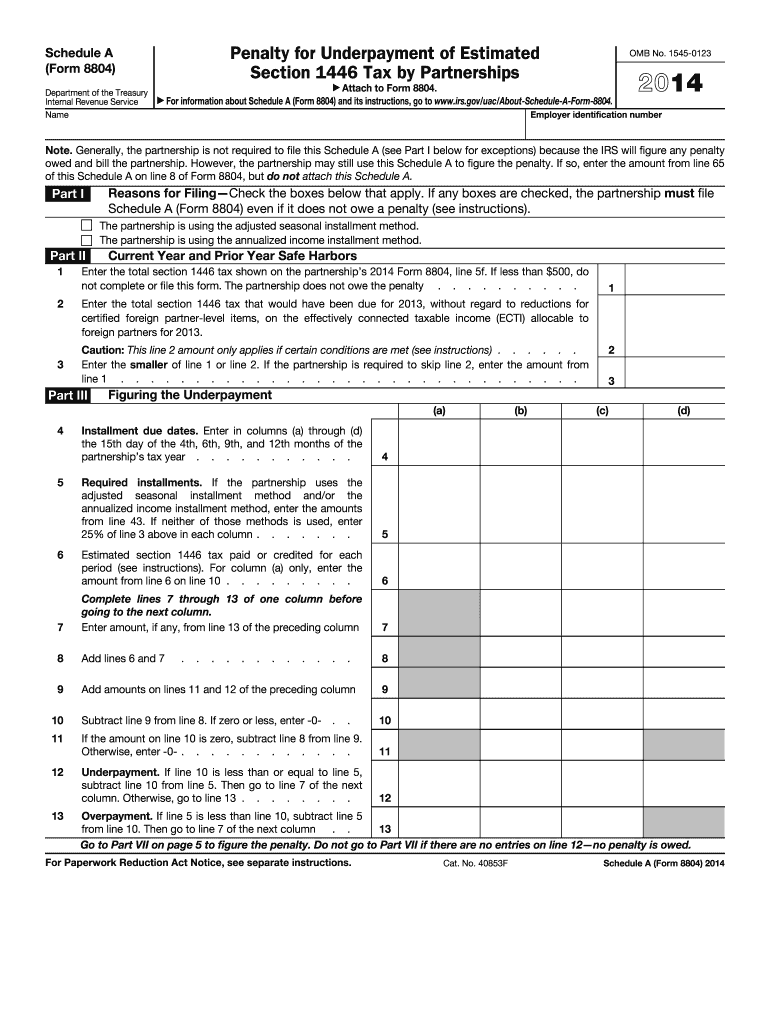

The 2014 Form 8804 (Schedule A), regarding penalties for underpayment of estimated Section 1446 tax by partnerships, serves as a tool for partnerships to calculate any potential penalties owed due to underpayment of tax obligations. This form outlines procedures and requirements for partnerships to estimate and report these tax-related payments accurately, ensuring compliance with IRS regulations. The primary objective is to minimize the risk of penalties from the IRS by accurately assessing any underpayment of estimated taxes, which are paid in installments throughout the year.

Use Cases of the 2014 Form 8804 (Schedule A)

This form is essential for partnerships that anticipate owing federal taxes on allocated income to foreign partners. It allows these partnerships to determine if they have met their tax payment obligations or if there are shortfalls leading to penalties. Partnerships can employ this form to self-assess penalties, providing a clear understanding of their financial liabilities relative to their foreign partners. By using this form, partnerships can proactively address potential penalties, ensuring better financial planning and adherence to tax laws.

Steps to Complete the Form

-

Gather Necessary Information: Before starting, collect financial data, including prior year income, current year income estimates, and tax installment payments made.

-

Safe Harbor Calculations: Calculate current and prior year safe harbors to determine if the tax payments meet safe harbor provisions, which can mitigate potential penalties.

-

Estimate of Payments: Assess payments based on adjusted seasonal or annualized income methods, ensuring accuracy by reflecting actual business income patterns.

-

Fill Schedule A Sections: Enter financial data into relevant sections of Schedule A, ensuring each part aligns with the IRS's requirements for calculating underpayment penalties.

-

Review and Verify: Double-check all entries for accuracy. Ensure that calculations conform to IRS guidelines to prevent potential missteps.

-

File with IRS: Submit the completed Schedule A with Form 8804 to the IRS by the stipulated deadline. Ensure timely submission to avoid additional late filing penalties.

Key Elements of the Form

-

Current Year Safe Harbors: These provide relief by ensuring no underpayment penalty if the partnership’s estimated payments meet certain thresholds based on current income.

-

Prior Year Safe Harbors: Helpful for partnerships experiencing significant income fluctuations, allowing them to base computations on previous year's tax obligations.

-

Installment Due Dates: Highlights installments due throughout the fiscal year, crucial for planning and avoiding underpayment.

-

Underpayment Calculations: Spells out method to compute penalties on any shortfall between estimated tax paid and tax liability owed.

IRS Guidelines and Filing Deadlines

The IRS mandates that partnerships subject to withholding tax on foreign partners file Form 8804 along with Schedule A by the 15th day of the third month following the close of the partnership’s tax year. Guidelines emphasize proper estimates, documentation, and timely filings, with a focus on avoiding underpayments. Penalties accrue on underestimated payments, so accuracy and compliance are imperative.

Required Documents and Submissions

-

Income Statements: For both current and projected years, illustrating taxable income computations.

-

Payment Records: Evidence of installment payments made throughout the fiscal year.

-

Schedule K-1 Forms: Detailing income distribution to partners to substantiate estimated tax payments.

-

Form 8804: The main document for reporting tax withheld and remitted to the IRS.

Partnerships may submit these documents electronically or via mail, provided deadlines and IRS instructions are adhered to.

Penalties for Non-Compliance

Failing to file Form 8804 (Schedule A) or underpaying taxes results in penalties. These include interest on the underpayment amount and additional penalties depending on the extent of non-compliance. Mitigation is possible through safe harbor provisions, underscoring the importance of accurate estimations and timely submissions. Partnerships should diligently monitor all IRS communications to address potential discrepancies promptly.

Digital vs. Paper Version

The IRS supports electronic submission, which offers faster processing and confirmation of receipt compared to paper filing. Online submissions are particularly advantageous, with integrated error-checking features that reduce the risk of arithmetic and data entry mistakes, ensuring more accurate completion of the form. For partnerships using paper versions, meticulous attention to detail during completion is essential to prevent filing delays and penalties.

Business Entity Types Benefiting from the Form

While all partnerships with foreign partners must consider filing, limited partnerships and general partnerships whose members include foreign entities derive significant benefits. These partnerships must compute withholding taxes on distributive shares of partnership income effectively, and this form ensures appropriate tax management and adherence to federal requirements. By applying these calculations efficiently, partnerships can alleviate potential financial liabilities associated with non-compliance.