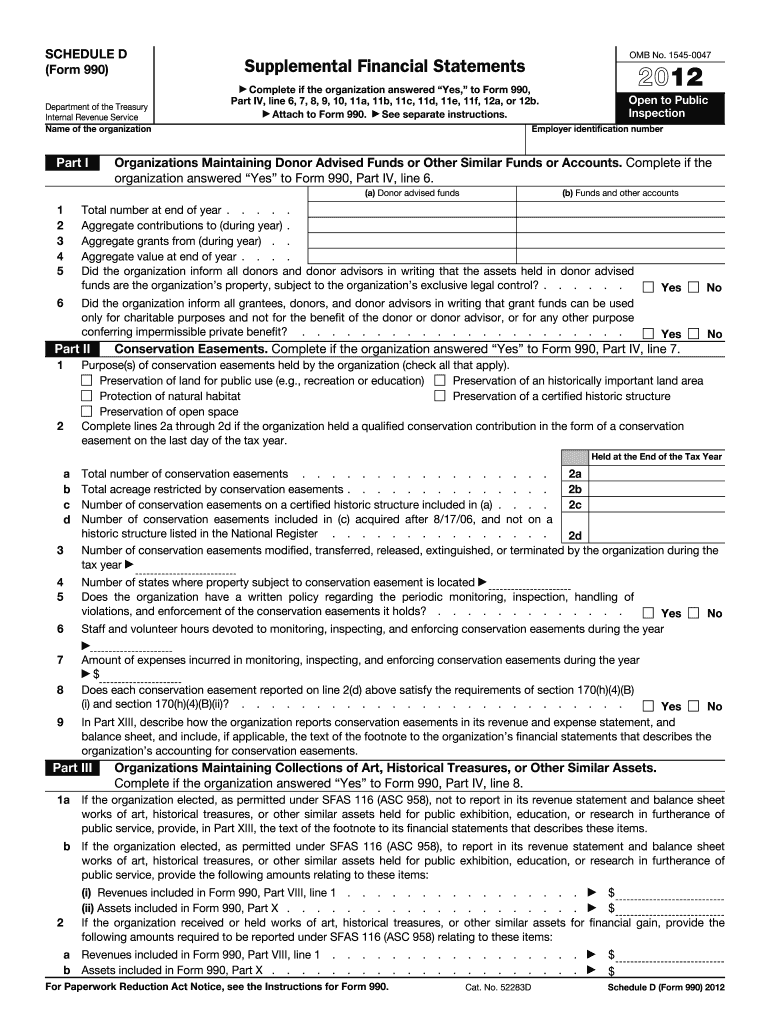

Definition and Purpose of the 2012 Schedule D Form

The 2012 Schedule D form is a critical document used by individuals and businesses to report capital gains and losses on federal tax returns. This form is part of the IRS Form 1040 and provides a detailed record of transactions involving the sale or exchange of capital assets, such as stocks, bonds, real estate, or property. Understanding the purpose of this form is essential for accurately reflecting your financial activities and complying with tax regulations.

Components of the Form

- Capital Gains and Losses Reporting: Schedule D is designed to detail the financial outcomes from the sale of capital assets, distinguishing between short-term (held for one year or less) and long-term (held for more than one year).

- Transactional Summaries: The form requires a summary of all sale transactions, including the dates of acquisition and sale, cost basis, and the proceeds received.

Importance in Filing Taxes

Accurate completion of the 2012 Schedule D form can influence your overall tax liability, as it determines the capital gains tax owed. This document provides a structured framework for taxpayers to report these often complex transactions, highlighting the need for precision and comprehensive record-keeping.

Steps to Complete the 2012 Schedule D Form

Completing the 2012 Schedule D form involves several sequential steps, each requiring careful attention to detail and accurate information.

- Gather Necessary Documentation: Collect all relevant documents, such as brokerage statements, purchase records, and transaction confirmations.

- Calculate Gains and Losses: Separate transactions into short-term and long-term categories, calculating the difference between the purchase price and sale price for each asset.

- Fill Out Part I for Short-Term Transactions: Enter details of each short-term sale in Part I, ensuring the accuracy of dates and financial figures.

- Complete Part II for Long-Term Transactions: Similarly, document long-term sales in Part II, with particular attention to any exemptions or adjustments.

- Summarize Totals in Part III: Sum up your capital gains and losses, integrating them into your overall tax calculations on the Form 1040.

- Review and Submit: Double-check all entries for completeness and accuracy before submission, keeping copies for your records.

Additional Considerations

- Special Scenarios: Be aware of additional forms or schedules that may be necessary if your transactions involve complexities like wash sales or inherited assets.

Legal Considerations for the 2012 Schedule D Form

Adhering to legal guidelines when using the 2012 Schedule D form is essential to ensure compliance and avoid potential penalties.

IRS Regulations

The IRS enforces strict regulations on capital gains reporting, making it critical to follow their instructions when completing the form. Non-compliance can result in audits, additional taxes, interest, and penalties.

- Audit Triggers: Discrepancies or inaccuracies in reporting could lead to audits. Ensuring that your filings match brokerage records and other financial documents helps to reduce this risk.

Key Elements of the 2012 Schedule D Form

Several key elements comprise the structure of the 2012 Schedule D form, each contributing to a comprehensive declaration of capital transactions.

Essential Sections

- Transaction Identification: Each sale or exchange of a capital asset must be accompanied by specific details, such as acquisition date, sale date, cost basis, and net proceeds.

- Special Adjustments: Adjustments might be necessary for specific transactions, including wash sales or qualified dividends, requiring additional forms or entries on Schedule D.

Precise Record-Keeping

Accurate and organized record-keeping is fundamental to completing Schedule D successfully. Consistent tracking of transactions throughout the year will aid in compiling the required information when tax season arrives.

Penalties for Non-Compliance

Failing to comply with the correct usage of the 2012 Schedule D form can lead to significant repercussions from the IRS.

Common Penalties

- Fines and Interest: Inaccurate reporting can result in financial penalties and interest charges on unpaid taxes.

- Audit Risks: Incorrect filings are red flags for audits, potentially exposing you to further scrutiny and financial liabilities.

IRS Guidelines and Requirements

The IRS provides comprehensive guidelines for completing the 2012 Schedule D form, emphasizing the importance of accuracy and completeness.

Key Guidelines

- Documentation: Ensure all transactions are well-documented with relevant records and receipts.

- Time Frames: Distinguish between short-term and long-term transactions, as they are taxed differently.

Examples of Using the 2012 Schedule D Form

Consider practical examples to get a better understanding of how the 2012 Schedule D form functions in real-world scenarios.

Case Study Scenarios

- Individual Investor: An individual buying and selling stocks will report each transaction, showing short-term and long-term gains and losses.

- Real Estate Transactions: When selling a property, owners need to report the cost basis and proceeds, factoring in depreciation and improvements to the property.

Understanding these examples provides clarity on effectively using the form to ensure accurate tax assessment and compliance.