Definition & Meaning

Form 1120-W is a worksheet issued by the Internal Revenue Service (IRS) specifically for corporations to estimate their tax obligations for the 2013 tax year. This form is designed as a calculation tool rather than a submission requirement. It helps corporations determine the amount of estimated tax they need to pay throughout the year to avoid penalties and interest on underpayment. Utilizing this form can assist corporations in managing their tax liabilities effectively, ensuring that they make accurate and timely estimated tax payments.

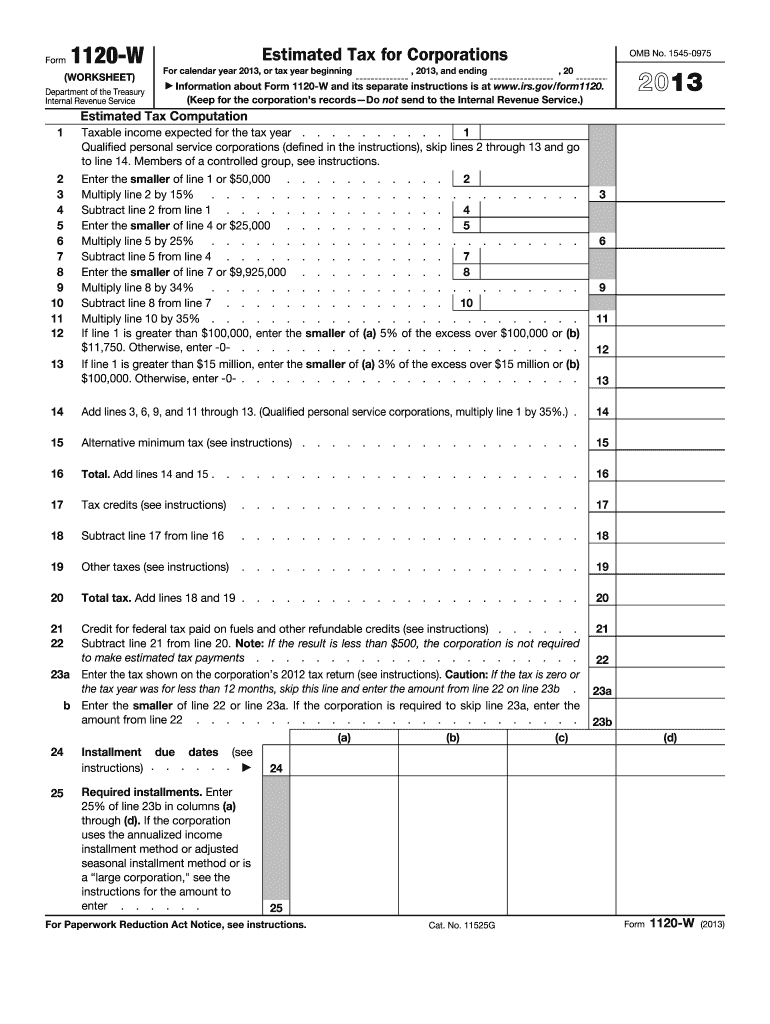

How to Use Form 1120-W for 2013

To utilize Form 1120-W effectively, corporations must first gather information about their expected income, allowing them to compute taxable income. This form provides sections to calculate the estimated tax by taking into account dividend distributions, corporate tax rates, and any applicable credits. Corporations should follow these steps:

- Estimate Taxable Income: Compile your total income anticipated for the 2013 tax year.

- Calculate Tax Liability: Apply tax rates to determine the estimated tax liability.

- Review Tax Credits and Deductions: Consider any available tax credits or deductions and incorporate these into your calculations.

- Determine Estimated Payments: Based on the liabilities and credits, compute the required estimated tax installments.

This detailed approach ensures accurate projections and helps in aligning the tax payments with actual earnings.

How to Obtain Form 1120-W for 2013

Corporations can access Form 1120-W online through the official Internal Revenue Service website. Download the form directly in a printable PDF format, ensuring it is legible and complete. Alternatively, tax professionals and software platforms also provide access to this form as part of their tax preparation services. Keeping a digital version of the form allows easy modifications and updates as financial circumstances change throughout the year.

Steps to Complete Form 1120-W

Completing Form 1120-W involves several steps to ensure accurate calculations:

-

Input All Sources of Income: Begin with a thorough listing of projected income sources, including revenue streams and gainful transactions.

-

Compute Adjusted Gross Income: Adjust for recognized deductions and credits that the corporation is eligible for.

-

Apply Corporate Tax Rates: Use the appropriate tax rates stipulated for the year 2013 to apply to the calculated taxable income.

-

Review for Completeness and Accuracy: Carefully check entries for miscalculations and ensure all required fields are filled.

-

Determine Due Installments: Divide the total estimated tax by the number of installments due, ensuring each payment is correctly timed.

By following these structured steps, corporations can maintain compliance with IRS requirements while effectively managing fiscal responsibilities.

Key Elements of Form 1120-W for 2013

The form encompasses various critical components and sections that need careful attention:

- Taxable Income Calculation Sections: Outlining gross income, deductions, and reductions.

- Alternative Minimum Tax Calculations: Handling adjustments if subject to alternative minimum tax scenarios.

- Installment Payment Schedules: Inclusion of dates and amounts for required tax installments.

- Integration of Tax Credits: How available tax credits are applied to the estimated liability.

Each element is designed to ensure corporations can thoroughly calculate their tax payment requirements, thereby minimizing compliance issues.

Who Typically Uses Form 1120-W for 2013

Form 1120-W is predominantly utilized by corporate entities that anticipate a minimum income subject to federal taxes. This includes:

- Large Corporations: With substantial taxable revenues.

- SMEs: Small to medium enterprises that are structured as corporations.

- Multi-State Corporations: Operating across different states with varied tax obligations.

Each corporation type should tailor the use of the form to their respective financial scenarios, ensuring accurate tax calculations.

IRS Guidelines for Form 1120-W

The IRS provides specific guidelines on the utilization of Form 1120-W, emphasizing compliance and accuracy. These guidelines cover:

- Estimated Payment Thresholds: Minimum payment requirements to be met.

- Reporting Changes: How corporations should handle significant income changes during the fiscal year.

- Penalties: Conditions under which penalties apply for underpayment.

Adhering to these IRS guidelines ensures corporations remain compliant and reduce the risk of incurring penalties.

Filing Deadlines and Important Dates

To prevent penalties, corporations must adhere to specified deadlines for estimated tax payments:

- Quarterly Installments: Payments due around April 15, June 15, September 15, and January 15 of the subsequent year.

- Record-Keeping: Corporations should maintain records and calculations used in completing the form to facilitate any IRS audits or queries effectively.

Meeting these deadlines is crucial for maintaining good standing with IRS requirements and avoiding financial detriments due to missed payments.