Definition & Meaning

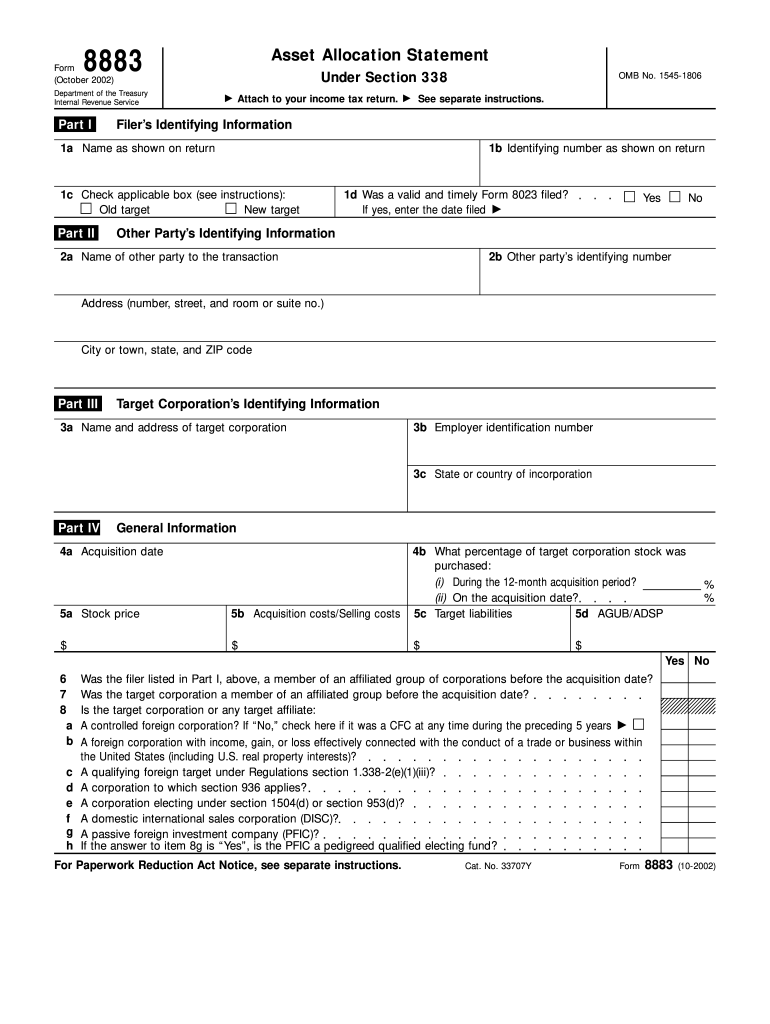

Form 8883, officially titled "Asset Allocation Statement Under Section 338", is a document mandated by the Department of the Treasury, Internal Revenue Service, dated October 2002. It is primarily used by purchasers of corporate stock to report the allocation of assets following certain qualifying stock acquisitions. Section 338 of the Internal Revenue Code allows a corporation that has acquired at least 80% of another corporation's stock to treat the stock purchase as an asset purchase for tax purposes. This form enables the purchaser to document how the internal revenue code is applied in valuing and allocating the acquired assets.

Key Objectives of Form 8883

- Facilitate the adjustment of tax attributes between involved entities.

- Ensure compliance with the regulations under Section 338.

- Support accurate reporting and calculation of tax liabilities for corporate acquisitions.

Steps to Complete the Form 8883

Completing Form 8883 involves a systematic approach and requires attention to detail.

Step-by-Step Instructions

- Identifying Information: Provide the basic information about the filing corporation and the target corporation, including names, addresses, and Employer Identification Numbers (EIN).

- Details of Acquisition: Specify the date of acquisition, and describe the type of transaction—whether a qualified stock purchase or another relevant type.

- Asset Allocation Details: List all assets acquired in the transaction, categorized appropriately, and denote fair market values.

- Use categories such as tangible personal property, real property, inventory, and goodwill.

- Certification and Signature: Ensure the credibility of the form by certifying all provided information is true, complete, and correct to the best of your knowledge before signing.

Common Mistakes to Avoid

- Misclassification of assets can lead to incorrect tax calculations.

- Inaccurate valuations may result in penalties or adjustments by the IRS.

- Omitting necessary signatures can lead to processing delays.

Key Elements of Form 8883

Understanding the primary sections of Form 8883 is crucial in ensuring thorough completion.

Essential Sections

- Section 1: Basic Information

- Lists information regarding the corporation making the purchase and the acquired target corporation.

- Section 2: Transaction Details

- Focuses on the acquisition date and nature of the transaction.

- Section 3: Asset Schedule and Allocation

- Requires detailed entries of asset categories and their fair market valuations.

Detailed Asset Breakdown

- Tangible Property: Encompasses physical assets like machinery and buildings.

- Intangible Property: Includes intellectual property and goodwill.

Who Typically Uses Form 8883

Form 8883 is commonly used in corporate transactions involving significant stock purchases.

Typical Users

- Corporations Acquiring Companies: Especially where an election under Section 338 is made.

- Tax Advisors and Accountants: Assisting clients with complex business acquisitions.

- Legal Advisors: Ensuring compliance and proper documentation during mergers and acquisitions.

Business Entity Types

- C Corporations: Most often engage in transactions requiring Form 8883.

- S Corporations and LLCs: May also be involved when acquiring a majority stake in another corporation.

IRS Guidelines

The Internal Revenue Service publishes specific guidelines to assist in the proper completion of Form 8883.

Important Instructions

- Guidance on Asset Valuation: The IRS provides standards for fair market valuation.

- Filing Instructions: Specific instructions on how to submit the form, including relevant IRS mailing addresses.

- Error Correction: Procedures for submitting corrected forms if errors are identified post-submission.

Benefits of Compliance

- Avoiding Penalties: Adhering to IRS guidelines helps mitigate the risk of financial penalties.

- Ensuring Tax Benefits: Proper allocation of assets can optimize tax outcomes under Section 338.

Filing Deadlines / Important Dates

Timeliness in filing Form 8883 is critical to avoid penalties and ensure compliance.

Critical Dates

- Filing Deadline: Typically coincides with the corporation's tax return due date, including any extensions.

- Transactional Deadlines: Be aware of election timelines under Section 338, which require timely form completion and submission.

Strategies for Timely Filing

- Early Preparation: Start gathering necessary documents and valuations well before the filing deadline.

- Organized Documentation: Maintain a well-organized repository of all transactional documents for easy access during form completion.

Penalties for Non-Compliance

Non-compliance with IRS requirements associated with Form 8883 can lead to various penalties.

Potential Consequences

- Financial Penalties: Incorrect form submission or late filings can result in fines.

- Tax Adjustments: Misreported or misclassified asset allocations can lead to additional tax liabilities.

- Legal Repercussions: Significant non-compliance might necessitate legal recourse or result in IRS audits.

Mitigation of Risks

- Regular Audits: Regular internal audits to ensure compliance with IRS rules.

- Professional Consultations: Engage with tax professionals for reviews and advice.