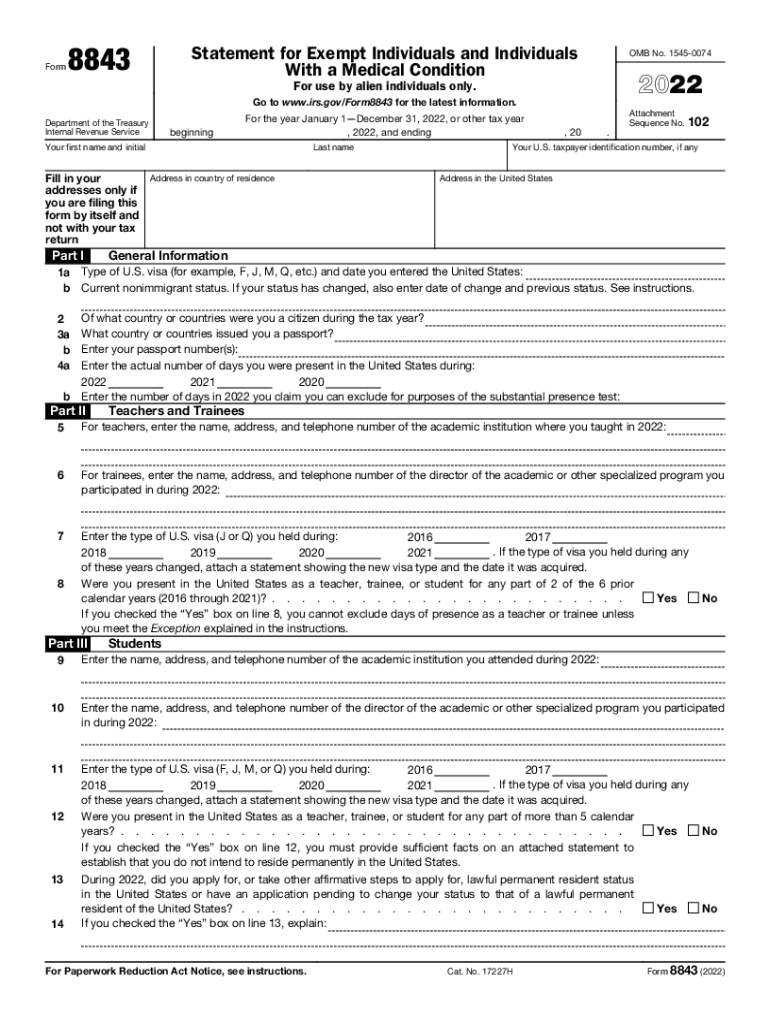

Definition and Purpose of Form 8843

Form 8843 is a statement required for certain alien individuals to explain their claim of exemption for tax purposes in the United States. The form is designated for individuals who are exempted from the counting of days present in the U.S., which affects their tax residency status under the substantial presence test. This includes specific groups such as students, teachers, trainees, and professional athletes participating in charitable events. The form ensures these individuals properly document their exemption status, outlining personal details and visa information to support their claim.

Eligibility Criteria for Form 8843

To determine eligibility for Form 8843, individuals must be nonresident aliens who are present in the U.S. under a visa that allows for exemption from the substantial presence test. Specific groups eligible to file Form 8843 include:

- Students on F, J, M, or Q visas

- Teachers or trainees on J or Q visas

- Professional athletes present for charitable events

- Individuals with medical conditions preventing departure

Each category has unique criteria, which individuals must fulfill to claim the tax exemption.

Steps to Complete Form 8843

Filling out Form 8843 involves several careful steps to ensure all relevant information is accurately reported:

- Section I: Enter personal information, including name, address, and taxpayer identification number.

- Section II: Provide visa details and the category under which you are claiming exemption.

- Section III (if applicable): Complete this part if you are a student, providing the institution's name and related information.

- Additional Sections: Fill out only if applicable to your specific category, ensuring to provide any required attachments or explanations.

- Signature and Date: Review the form thoroughly before signing and dating it.

Submission Methods for Form 8843

Form 8843 can be submitted via various methods, depending on individual preference and convenience:

- Mail: Completed forms can be sent directly to the IRS by mail.

- Online Submission: Available through certain tax prep services and software.

- In-Person: Individuals may also choose to submit their forms through IRS Taxpayer Assistance Centers.

It is crucial to verify deadlines and specific submission guidelines as these can impact processing time.

Filing Deadlines and Important Dates

The deadline for filing Form 8843 coincides with the U.S. tax filing deadline, which usually is April 15. However, nonresident aliens who do not earn income are advised to submit their forms by June 15 to avoid any discrepancies. Those who earn income might be required to adhere to the standard April deadline. It is essential to keep track of these dates and consider filing early to ensure timely processing.

Penalties for Non-Compliance

Failure to file Form 8843 when required may result in complications with the IRS regarding tax residency status. While there is no financial penalty associated directly with not filing Form 8843, neglecting to submit the form can lead to audits or challenges in proving your nonresident status. To avoid these challenges, timely and accurate submission is recommended.

Common Terms Related to Form 8843

Understanding terminology relevant to Form 8843 is crucial:

- Substantial Presence Test: A criterion used to determine tax residency based on the number of days an individual is present in the U.S.

- Exempt Individual: A nonresident alien qualifying for exclusion of their presence days for tax purposes.

- Nonresident Alien: An individual who is not a U.S. citizen or resident alien for tax purposes.

Familiarity with these terms helps in completing the form accurately and understanding its implications.

Digital vs. Paper Versions of Form 8843

Form 8843 can be accessed and completed both digitally and on paper. The digital version allows for online completion, which often integrates with tax software, facilitating straightforward submission. Conversely, a paper form requires manual completion and mailing to the IRS. The choice between these methods should consider convenience, accessibility, and personal preference in managing tax documentation.