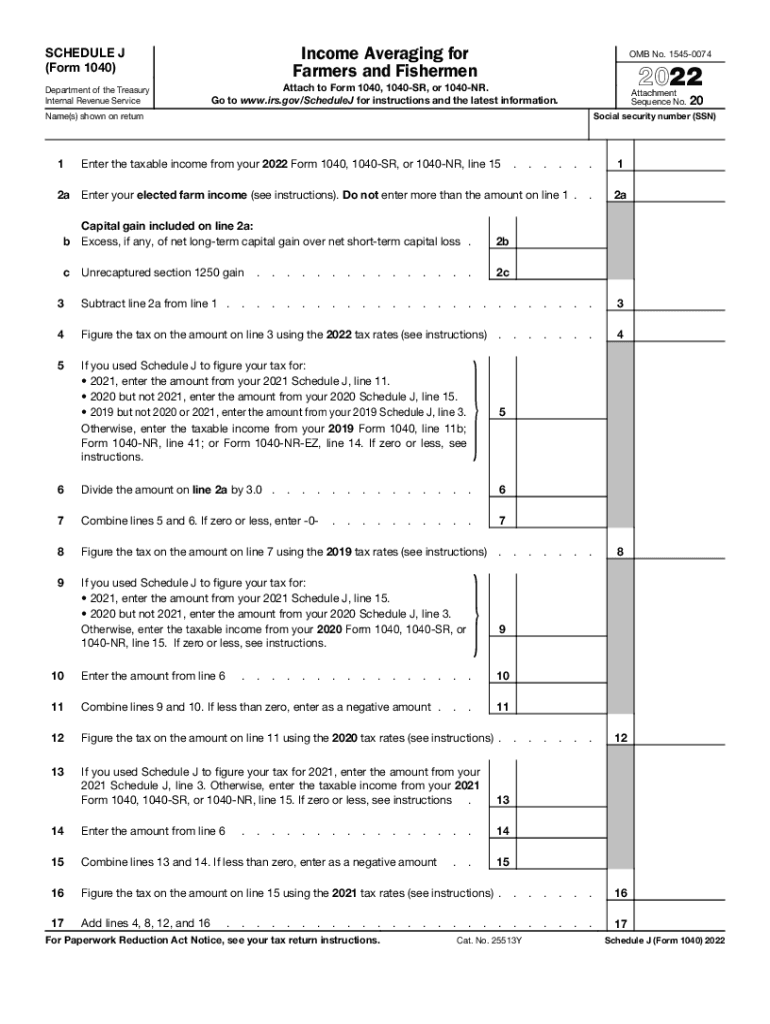

Definition and Purpose of Schedule J (Form 1040)

Schedule J (Form 1040) is a tax form used specifically by farmers and fishermen in the United States to calculate their income tax through a method known as income averaging. This form allows eligible taxpayers to average their taxable income over the previous three years, which can result in a lower tax liability in years when their income fluctuates significantly. Income averaging can be particularly beneficial for farmers and fishermen whose earnings are typically unstable due to factors like weather, market conditions, and other seasonal influences. By smoothing out the income peaks and troughs over three years, Schedule J helps to stabilize their tax obligations.

How to Use Schedule J (Form 1040)

To use Schedule J, a taxpayer must first determine their eligibility. Only those whose income comes largely from farming or fishing can use this form. The taxpayer calculates what portion of their current year's income qualifies as "elected farm income." Then, this amount is spread across the prior three tax years to determine how the tax liability would have looked with a more stable income over time. Completing Schedule J involves a series of calculations that require information from the taxpayer’s previous tax returns, including total taxable income and capital gains for those years.

Eligibility Criteria for Schedule J

Eligible individuals include those whose principal source of income is from farming or fishing. Specifically, two-thirds of their gross income for the year must come from farming or fishing activities. Additionally, individuals must have filed a Form 1040, 1040-SR, or 1040-NR for the year they are averaging income. Eligibility is impacted by how one defines farm income; this includes income from the sale of crops, livestock, farm rental income, and other related activities.

Important Terms Related to Schedule J

- Elected Farm Income: The portion of current year income designated by the taxpayer as farm income for averaging purposes.

- Taxable Income: Income remaining after deductions are applied to the gross income.

- Capital Gains: Profits from the sale of farm property, which must be included in income calculations.

- Prior Year Tax Rates: Historical rates used for determining the tax liabilities for the elected farm income.

Steps to Complete Schedule J

- Gather Previous Years' Tax Information: Collect tax returns from the previous three years to assess past taxable income and tax rates.

- Calculate Elected Farm Income: Determine which parts of your current income are classified as farm income.

- Spread Income Across Years: Allocate the elected farm income across the previous three tax years.

- Apply Past Tax Rates: Calculate the tax liability using the rates and brackets from each of the past years.

- Complete Schedule J Form: Fill out the form with the calculated figures, ensuring accuracy in reporting and calculations.

- Attach to Form 1040 Series: Attach completed Schedule J to Form 1040, 1040-SR, or 1040-NR.

Legal Considerations and Compliance

The use of Schedule J must comply with IRS regulations outlined under the Internal Revenue Code. Any inaccuracies or non-compliance in reporting could result in penalties or additional tax liabilities. This emphasizes the importance of carefully verifying all income calculations and ensuring alignment with IRS guidelines. Legal use demands proper record-keeping and accuracy in utilizing historical data to support the averaging process.

Real-World Scenarios and Examples

- Fluctuating Crop Prices: A farmer experiences significant price changes in crops between 2020 and 2022. By averaging income with the more profitable years, they can reduce their 2022 tax burden.

- Fishing Business Affected by Weather: Weather patterns impacted a fisherman's haul, greatly reducing income one year. Using income averaging mitigates the tax effect of this downturn by spreading income over more stable years.

IRS Guidelines and Documentation

The IRS provides detailed instructions for completing Schedule J, which include necessary documentation for income and capital gains. Following these guidelines is critical for accurately reporting and avoiding discrepancies. Taxpayers may need to provide supporting documents, such as sales records, income logs, and tax returns, from the previous years to substantiate their claims on the form.

Penalties for Non-Compliance

Failure to accurately complete Schedule J or file it correctly with the appropriate Form 1040 series can lead to significant penalties. The IRS may impose fines, request back taxes, or increase interest on unpaid taxes if taxpayers fail to legally document and prove their income averaging claims. Keeping precise records and ensuring proper form completion can help avoid these issues.