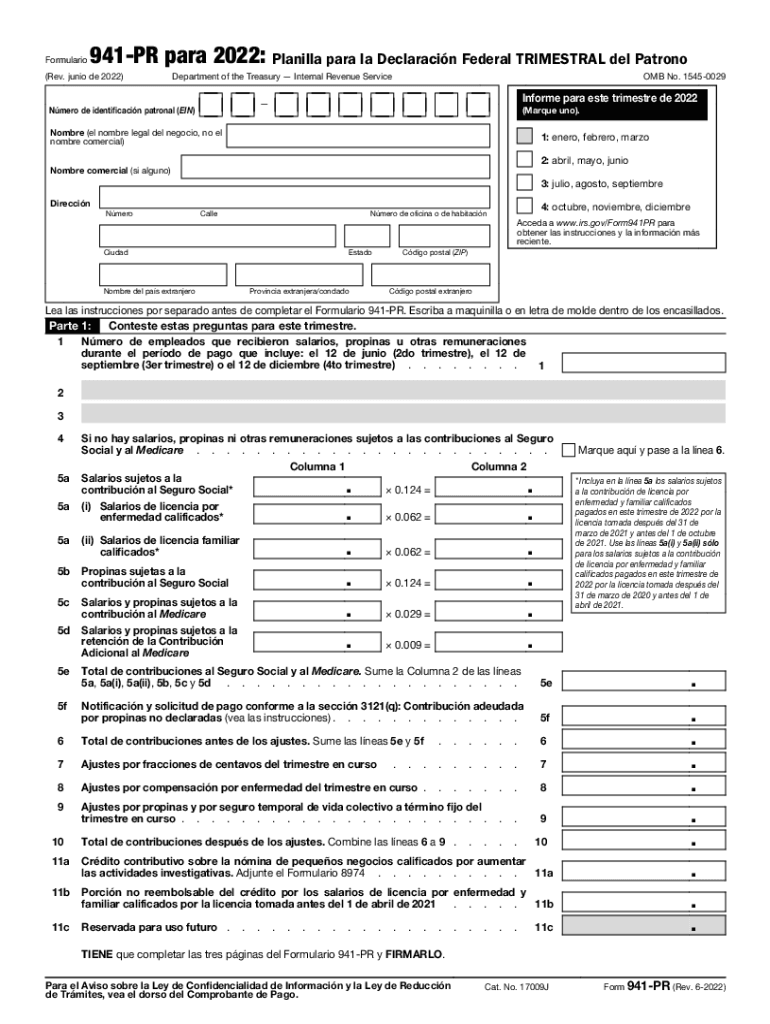

Definition and Purpose of Form 941-PR

Form 941-PR, the Employer's Quarterly Federal Tax Return (Puerto Rican version), is essential for employers in Puerto Rico to report wages, tips, and other compensation paid to employees. This form also mandates the reporting of Social Security and Medicare contributions. Issued by the U.S. Department of the Treasury and the IRS, it is an updated version from June 2022, specifically tailored to meet the needs of employers operating in Puerto Rico.

Key Reporting Elements

- Employee Compensation: Includes wages, tips, and other forms of earnings.

- Social Security & Medicare Taxes: Employers must calculate and report these contributions accurately.

- Tax Credits: Any applicable refunds or credits, such as the employee retention credit, may be claimed here.

Eligible Users of Form 941-PR

This form is primarily used by businesses operating in Puerto Rico. Employers, typically ranging from small businesses to large corporations, must file this form. Non-profit organizations and government entities in Puerto Rico might also be required to file if they have employment tax liabilities.

Typical Users

- Small and Large Businesses: Any size business in Puerto Rico paying employee compensation.

- Non-Profits and Government Entities: If such entities have taxable employee wages, they must also file.

- Self-Employed Persons: Those with employees may need to comply with this filing requirement.

Steps for Completing Form 941-PR

Completing this form requires detailed information and accuracy. Employers must follow a series of steps to ensure all necessary data is accurately reported.

Step-by-Step Process

- Gather Information: Start by compiling records of wages paid and taxes withheld.

- Report Employee Count: Enter the total number of employees who received wages during the quarter.

- Calculate Taxes: Calculate the amount of Social Security and Medicare taxes due.

- Document Adjustments: Note any tax adjustments from prior quarters.

- Claim Credits: Include any qualified tax credits, such as tax exemptions for eligible employment.

- Sign and Date: Ensure the form is signed by an authorized individual to verify its accuracy.

IRS Guidelines and Instructions

The IRS provides specific instructions for properly filling out Form 941-PR, which details each section methodically.

Important IRS Instructions

- Line-by-Line Guidance: The IRS offers instructions to assist employers in understanding each section.

- Common Mistakes: Highlight areas where errors frequently occur, such as miscalculations or missed credits.

- Contact Resources: Information on how to contact the IRS for assistance or clarification.

Filing Deadlines and Important Dates

The Form 941-PR must be filed quarterly, with strict adherence to deadlines to avoid penalties.

Quarterly Deadlines

- First Quarter: Due by April 30

- Second Quarter: Due by July 31

- Third Quarter: Due by October 31

- Fourth Quarter: Due by January 31 the following year

- Extensions: An automatic 10-day filing extension applies if you have timely deposit history for your tax liabilities.

Penalties for Non-Compliance

Failing to comply with the requirements or deadlines of Form 941-PR can result in significant penalties.

Non-Compliance Consequences

- Late Filing Penalties: Accrue when forms are not submitted by due dates.

- Inaccurate Reporting: Penalties for incorrect or incomplete information.

- Underpayment of Taxes: Additional fees may apply for any unpaid tax amounts.

Submission Methods

Employers have several options for submitting Form 941-PR to facilitate ease of filing.

Available Submission Options

- Electronic Filing: Through the IRS e-file system for a quick submission process and faster turnaround.

- Mail Submission: Physical mailing of completed forms, though this might take longer for processing.

- In-Person: Submission directly at IRS offices might be available for specific cases.

Important Terms Related to Form 941-PR

Understanding key terms associated with Form 941-PR helps ensure accuracy and compliance.

Key Terminology

- Tax Liabilities: The total amount of tax obligations calculated.

- Adjusted Tax Returns: Corrections or amendments made from previous returns.

- Quarterly Reporting: The requirement to submit this form every three months, summarizing the previous quarter's activity.

Each section presented provides comprehensive insight essential for any employer navigating the Form 941-PR to ensure compliance and accurate reporting of employee-related taxes in Puerto Rico.