Definition and Meaning

The New York State Department of Taxation and Finance Passive Activity Loss form is a specialized tax document used by nonresidents and part-year residents to report passive activity loss limitations on their state tax returns. These losses typically originate from passive income-generating activities, such as rental real estate or limited partnerships, and are subject to specific limitations and reporting requirements distinct from federal guidelines.

Detailed Breakdown

- Passive Activity Income: Income derived from sources like rental properties and businesses in which the taxpayer does not actively participate.

- Loss Limitations: These are constraints imposed by New York State tax regulations aimed at limiting the amount of passive activity losses that can be deducted from state taxable income.

- Purpose: Helps taxpayers accurately compute the allowable passive activity losses that can be claimed in a tax year, ensuring compliance with state tax laws.

Important Terms related to Passive Activity Loss

Understanding the terminology associated with the New York State Department of Taxation and Finance Passive Activity Loss form is crucial for accurate completion.

Key Concepts

- Material Participation: Engagement level determining whether an activity is passive. A taxpayer is considered to have materially participated if they meet certain criteria, impacting how losses can be claimed.

- Aggregation: Combining multiple passive activities for the purpose of calculating net passive income or losses.

- Suspended Losses: Passive losses that exceed passive income and are not deductible in the current year but carried forward to future tax years.

Steps to Complete the Passive Activity Loss Form

Completing the New York State Department of Taxation and Finance Passive Activity Loss form involves several steps that require careful attention to detail.

- Gather Necessary Information: Collect documents related to all passive activities, including financial statements and previous tax returns.

- Calculate Passive Income and Losses: Determine the net income or loss for each passive activity.

- Apply State Adjustments: Adjust the federal calculations according to New York State-specific rules.

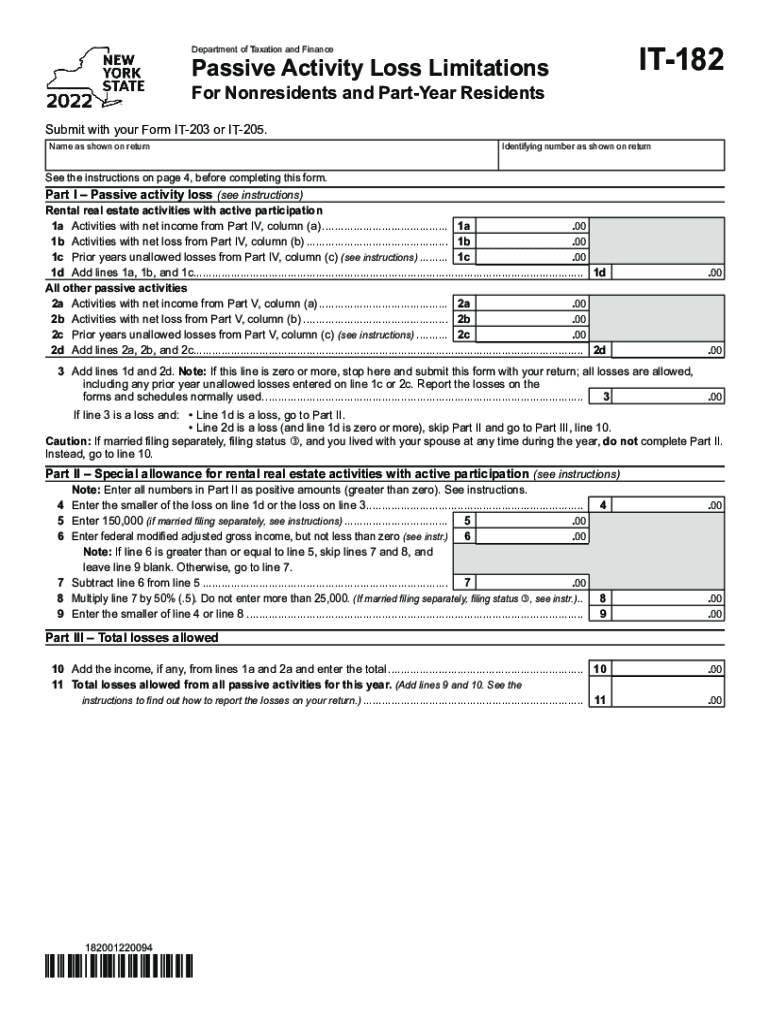

- Complete Form IT-182: Transfer calculated figures to the appropriate sections, ensuring accuracy.

- Review and Submit: Double-check for errors before submission via the appropriate method, whether online, by mail, or in person.

Guidance and Tips

- Seek Assistance: Consider consulting a tax professional if unfamiliar with passive activity loss regulations.

- Use Compatible Software: Software like TurboTax and QuickBooks can be beneficial for calculating and entering complex tax figures.

Key Elements of the Form

The form includes specific sections that need to be correctly filled out to ensure compliance with tax regulations.

- Personal Information: Enter accurate taxpayer information, including name and identification numbers.

- Passive Activity Details: List each passive activity, detailing the income, losses, and participant status.

- State-Adjusted Figures: Input adjustments made from federal to state calculations.

Required Documents

The successful completion of the form requires several key documents.

- Tax Returns from Previous Years: For comparison and calculation accuracy.

- Financial Records for Passive Activities: Including income statements and expense records.

- Federal Passive Activity Loss Worksheet: To serve as a baseline for state adjustments.

Preparing Documents

- Ensure all documents are well-organized and easily accessible.

- Keep digital copies for easy retrieval and submission.

Examples of Using the Passive Activity Loss Form

Various scenarios demonstrate the application of the form for different taxpayers.

Case Studies

- Scenario 1: A part-year resident with multiple rental properties calculates losses to minimize state tax liability.

- Scenario 2: A nonresident engaged in limited partnerships ensures compliance with passive loss limitations by detailed documentation.

State-Specific Rules

New York State has specific rules that differ from federal guidelines for passive activity losses.

Distinctions from Federal Laws

- Nonresidents and Part-Year Residents: These taxpayers must consider state residency status when determining loss limitations.

- Certain Income Types: Didactic rules outline which income types are considered passive under state law.

Penalties for Non-Compliance

Failure to comply with the regulations regarding passive activity losses can lead to financial penalties.

- Late Fees: Imposed for failing to submit the form by the designated deadline.

- Audit Risks: Increased likelihood of audits if discrepancies are found between federal and state submissions.

- Interest Charges: Applied to any underestimated or unpaid tax amounts resulting from incorrect loss reporting.