Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out Partners Distributive Share Items—International - IRS tax forms with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the Partners Distributive Share Items—International form in the editor.

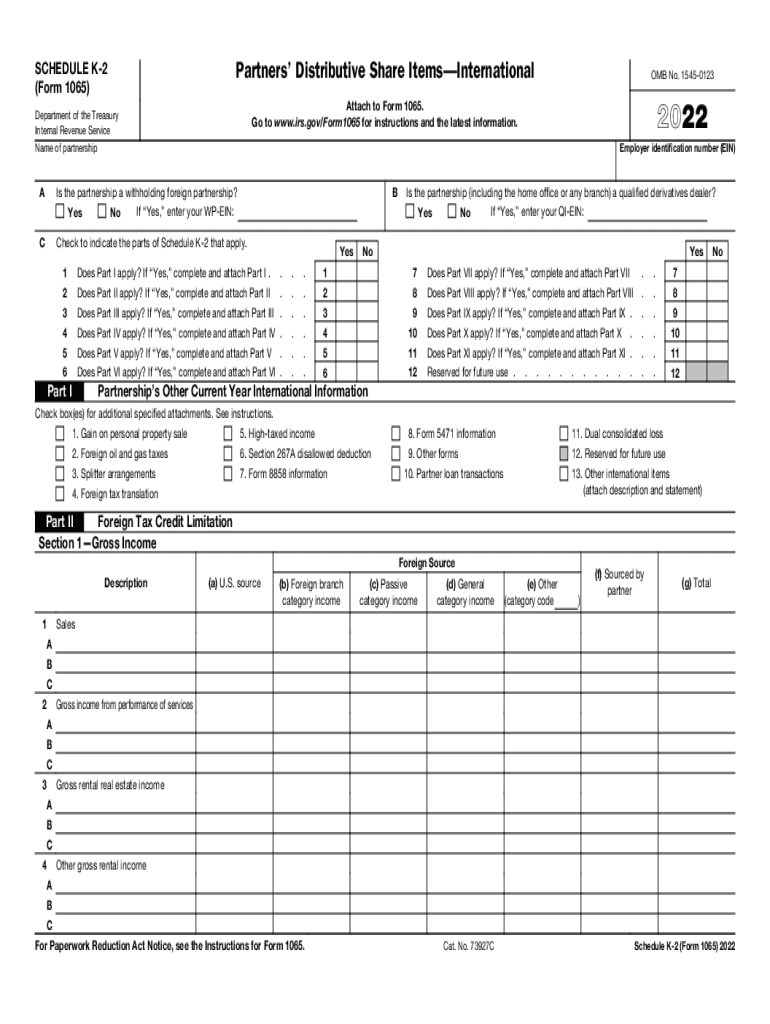

Begin by entering the Employer Identification Number (EIN) and the name of the partnership at the top of the form.

Indicate whether the partnership is a withholding foreign partnership by selecting 'Yes' or 'No' and, if applicable, enter your WP-EIN.

Check the boxes for each part of Schedule K-2 that applies to your partnership. Complete and attach any relevant parts as indicated.

Fill out Part II regarding Foreign Tax Credit Limitation, ensuring you accurately report gross income from various sources including U.S. and foreign categories.

Continue through each section, providing detailed information as required, such as deductions and other international items in Parts III through XI.

Start using our platform today to streamline your form completion process for free!

Fill out Partners Distributive Share ItemsInternational - IRS tax forms online It's free

See more Partners Distributive Share ItemsInternational - IRS tax forms versions

We've got more versions of the Partners Distributive Share ItemsInternational - IRS tax forms form. Select the right Partners Distributive Share ItemsInternational - IRS tax forms version from the list and start editing it straight away!

IRS 1040 Form 2025 release dateIRS tax forms 2025IRS 1040 Form 2026IRS tax forms 2025 PDFIRS tax forms 20262025 IRS tax forms printableIRS Form 1040 for 2025 PDFIRS 1040 Form 2025 Instructions

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

Product Number Form 1065 (Schedule K-2) Title Partners Distributive Share Items - International, Revision Date 2025, Posted Date 01/12/2026. Product NumberRead more

Feb 28, 2022 Granted, it is unlikely that anyone will perish during the preparation of Schedule K-2, Partners Distributive Share Items International.Read more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.