Definition and Purpose of Form 1094-C

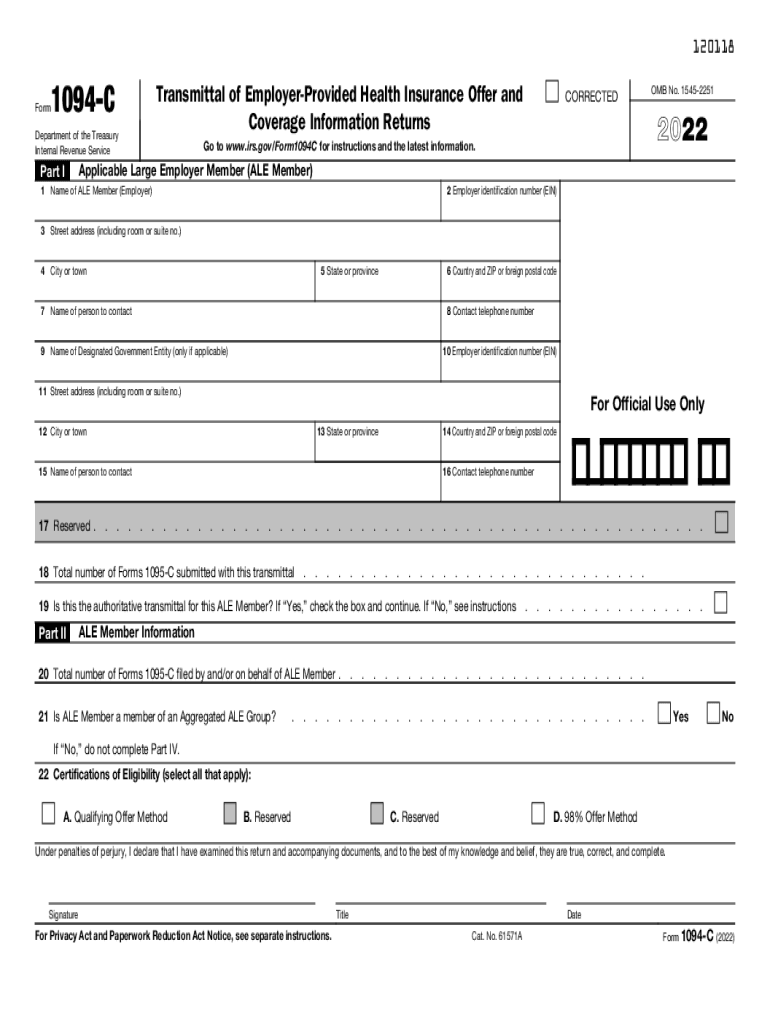

Form 1094-C, known as the Transmittal of Employer-Provided Health Insurance Offer and Coverage Information Returns, is an IRS form used by Applicable Large Employers (ALEs) in the United States to comply with the Affordable Care Act (ACA). This form acts as a cover sheet for Form 1095-C submissions, summarizing employer-provided health coverage to employees. ALEs are defined as employers with at least 50 full-time employees, including full-time equivalent employees, during the previous year.

Key Components of Form 1094-C

- Employer Information: Includes the employer's name, address, and Employer Identification Number (EIN).

- Contact Information: Details of the person responsible for the form's submission.

- Certifications of Eligibility: Statements indicating the employer's compliance with ACA regulations.

- Employee Counts: Information about the number of full-time employees throughout the year.

How to Obtain Form 1094-C

Employers can access Form 1094-C through the IRS website or electronic filing software approved by the IRS. Printable versions are available, but electronic filing is common due to its efficiency. Employers must ensure they have the correct year's version, as tax forms often update annually.

Online and Mail Options

- Electronic Access: Download from the IRS website or authorized software.

- Mail Option: Request a physical copy by contacting the IRS directly.

Steps to Complete Form 1094-C

- Gather Required Information: Collect employer details, employee counts, and health coverage data.

- Fill Out Employer Information: Enter business name, EIN, and contact details.

- Complete Employee Counts: Provide monthly employee counts and indicate whether coverage was offered.

- Certify Eligibility: Choose appropriate certifications of eligibility.

- Review and Sign the Form: Ensure accuracy before signing and dating the form.

Why Form 1094-C is Essential

Form 1094-C is crucial for demonstrating compliance with ACA provisions. By submitting this form, employers ensure they meet legal health coverage requirements, potentially avoiding penalties.

Importance for Compliance

- Legal Requirement: Mandatory for ALEs to report health coverage.

- Penalty Avoidance: Helps prevent ACA-related fines.

Who Typically Uses Form 1094-C

ALEs with 50 or more full-time employees, including nonprofits and government entities, use Form 1094-C. This requirement ensures that eligible organizations report health coverage accurately.

Examples of Users

- Corporations: Large businesses providing employee health benefits.

- Nonprofits: Charitable organizations meeting ALE criteria.

- Government Agencies: Public entities required to comply with ACA mandates.

Penalties for Non-Compliance

Failing to file Form 1094-C or providing incorrect information can result in significant penalties from the IRS. Employers must ensure accurate and timely submissions to avoid these financial repercussions.

Common Penalty Scenarios

- Failure to File: Not submitting the form by the deadline.

- Incorrect Information: Errors in employer or employee data.

- Late Submission: Filing after the stipulated deadline without reasonable cause.

Filing Deadlines and Important Dates

- Electronic Filing Deadline: Typically due by March 31 of the following year.

- Paper Filing Deadline: Generally due by February 28 of the following year.

- Employee Statement Deadline: Forms must be provided to employees by January 31.

Considerations for Timing

- Extension Requests: Employers can apply for a 30-day extension if necessary.

- Proactive Compilation: Gathering data early aids in meeting deadlines efficiently.

Software Compatibility

Form 1094-C is compatible with various tax software programs, including TurboTax and QuickBooks, facilitating accurate and efficient electronic filing.

Advantages of Using Software

- Accuracy: Reduces errors with automated checks.

- Convenience: Streamlines data input and submission processes.

- Integration: Works with existing accounting programs for seamless data transfer.

Examples of Using Form 1094-C

Consider a large manufacturing company employing over 100 workers. The HR department uses Form 1094-C to report health coverage to the IRS, ensuring compliance and avoiding penalties.

Real-World Scenarios

- Retail Chains: Large department stores complying with health coverage laws.

- Educational Institutions: Universities with vast numbers of staff and faculty members.

- Hospital Networks: Healthcare providers managing significant employee benefits.

Summary of IRS Guidelines

The IRS provides specific instructions for completing and submitting Form 1094-C, emphasizing accuracy in data entry and timely submission. Employers should adhere to these guidelines to fulfill their ACA obligations effectively.

Key Guidance Points

- Detailed Instructions: Available on the IRS website for step-by-step assistance.

- Contact Support: IRS support is accessible for questions about form completion.

- Compliance Checks: Regular audits may occur to ensure adherence to filing requirements.

This comprehensive overview offers maximum content coverage on IRS Form 1094-C, focusing on its definition, usage, acquisition, completion steps, importance, audience, compliance penalties, deadlines, compatibility, examples, and IRS guidelines.