Definition and Meaning

The "2021 Michigan Adjustments of Capital Gains and Losses MI-1041D" is a form issued by the Michigan Department of Treasury used for reporting and adjusting capital gains and losses for estates or trusts. It must be filed in conjunction with the MI-1041 fiduciary income tax return. The form ensures that accurate calculations and tax adjustments are made in accordance with Michigan's tax regulations, particularly for cases involving federal and state-specific capital gains and losses, including those derived from out-of-state properties or U.S. obligations.

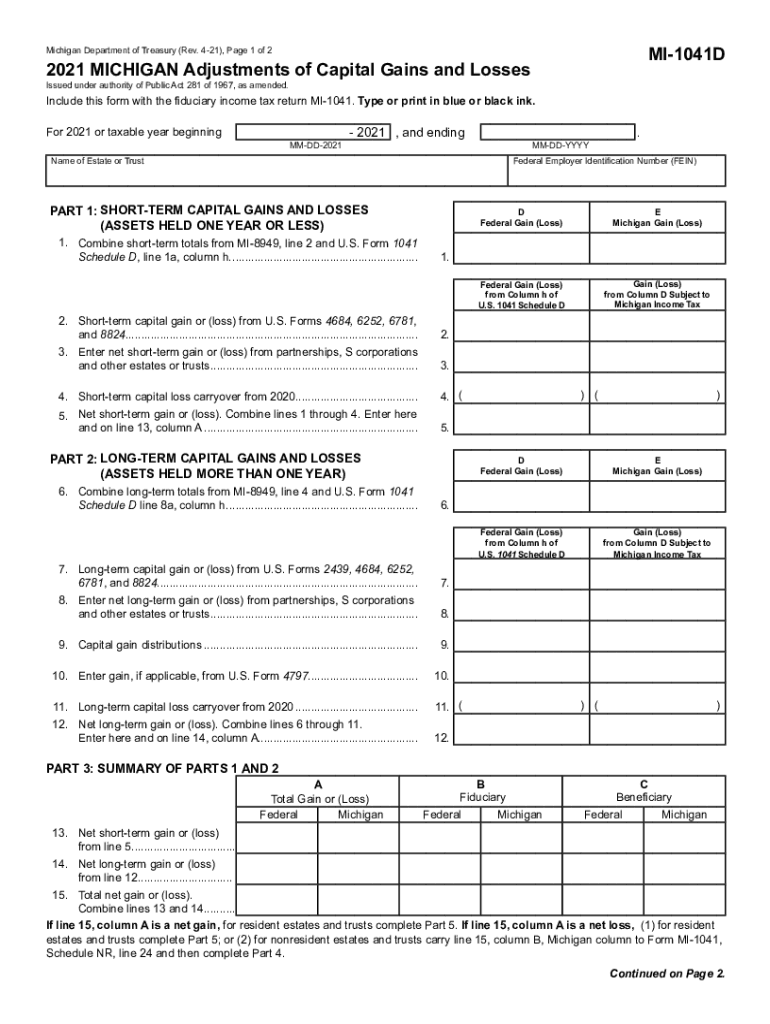

Steps to Complete the 2021 MICHIGAN Adjustments of Capital Gains and Losses MI-1041D

- Gather Necessary Documents: Collect all relevant documents, including transaction records, federal and Michigan tax returns, documentation for properties, and other financial statements.

- Fill in Personal Information: Enter the estate or trust's name, fiduciary name, and other identifying details.

- Report Short-term Capital Gains/Losses: Input details of short-term transactions. Provide descriptions, dates of acquisition and sale, and the gain or loss from each transaction.

- Report Long-term Capital Gains/Losses: Similar to short-term, include all necessary details related to long-term gains or losses.

- Calculate Capital Loss Limitations: Determine the amount of capital losses that can be deducted, based on current tax laws.

- Complete State Adjustments: Adjust figures for any discrepancies between federal and Michigan-specific reporting requirements.

- Review and Submit: Double-check all entries for accuracy, then file the form with the Michigan Department of Treasury.

Key Elements of the 2021 MICHIGAN Adjustments of Capital Gains and Losses MI-1041D

- Short-term Gains and Losses: Requires listing of each transaction with relevant details and total computation of gains or losses.

- Long-term Gains and Losses: Similar section dedicated to transactions held over a year, with appropriate adjustments and summaries.

- Capital Loss Carryover: Instructions for carrying over losses from previous years to offset current-year gains.

- State-specific Adjustments: Sections to adjust federal gains or losses to meet Michigan tax codes.

- Fiduciary Responsibility: Guidelines on how fiduciaries should ensure the accuracy of figures reported.

Important Terms Related to the MI-1041D

- Fiduciary: An individual or entity responsible for managing an estate or trust, especially in relation to handling tax filings.

- Capital Gains: Profits earned from the sale of assets or investments.

- Capital Losses: Losses incurred when the sale value of an asset or investment is less than the purchase price.

- Carryover: The mechanism of moving unused deductions or credits into subsequent years.

State-specific Rules for the MI-1041D

- Transactions involving out-of-state properties must comply with Michigan's specific tax adjustment rules.

- Obligations from U.S. properties need detailed reporting when calculating gains or losses.

- Michigan-specific tax credits or deductions may alter federal figures, requiring additional calculations.

Filing Deadlines and Important Dates

- Filing Deadline: Typically due by April 15 of the year following the tax year in question. Extensions may be available.

- Extensions: File for an extension if more time is needed, although this requires separate application and approval by the Michigan Department of Treasury.

Who Typically Uses the 2021 MICHIGAN Adjustments Form

- Estates and Trusts: The primary users responsible for reporting adjusted capital gains and losses annually.

- Fiduciaries and Tax Preparers: Trusted with the task of ensuring the form's accuracy and compliance with legal standards.

Examples of Using the 2021 MICHIGAN Adjustments of Capital Gains and Losses MI-1041D

- Estate Sale Transactions: When an estate sells a property, the fiduciary reports the transaction details and adjusts for Michigan laws.

- Investment Portfolio Adjustments: Trusts may adjust reported income from stocks or bonds, considering both federal and state regulations.

Legal Use of the MI-1041D

Filing this form is a legal requirement for fiduciaries managing estates or trusts with reportable capital gains or losses. Non-compliance can result in penalties and fines, so it's crucial for fiduciaries to adhere strictly to the guidelines provided by the Michigan Department of Treasury.

IRS Guidelines

Aligns with IRS guidance on capital gains and losses but requires additional steps to comply with Michigan-specific tax laws and reporting standards.

Software Compatibility

The MI-1041D can be completed using various tax preparation software, such as TurboTax and QuickBooks. These platforms often offer tools to import financial data directly, facilitating accurate and efficient completion of the form.

Required Documents

- Transaction Records: Extensive documentation of each sale or exchange of capital assets.

- Federal Tax Returns: Necessary to reference for adjustments and comparisons.

- Trust or Estate Financial Statements: Essential for completing the overall tax return and MI-1041D accurately.

By structuring the content to comprehensively cover the key topics related to the "2021 Michigan Adjustments of Capital Gains and Losses MI-1041D," users can gain a deeper understanding and practical insights for accurately completing the form, effecting a smooth compliance process with Michigan tax regulations.