Definition and Purpose of Maine Estate Tax Statement of Value

The Maine Estate Tax Statement of Value, also known as Form 700-SOV, is a critical document utilized for nontaxable estates in the state of Maine. This form is specifically designed to request a discharge of an estate tax lien on Maine property when the estate's total value does not exceed $6.01 million and does not necessitate a federal estate tax return. Understanding the purpose of this form is paramount, as it pertains to the resolution of estate matters within Maine jurisdiction. Its primary function serves as a verification tool that establishes whether an estate falls below the taxable threshold, which in turn facilitates the necessary procedures to release the lien on property tied to the estate.

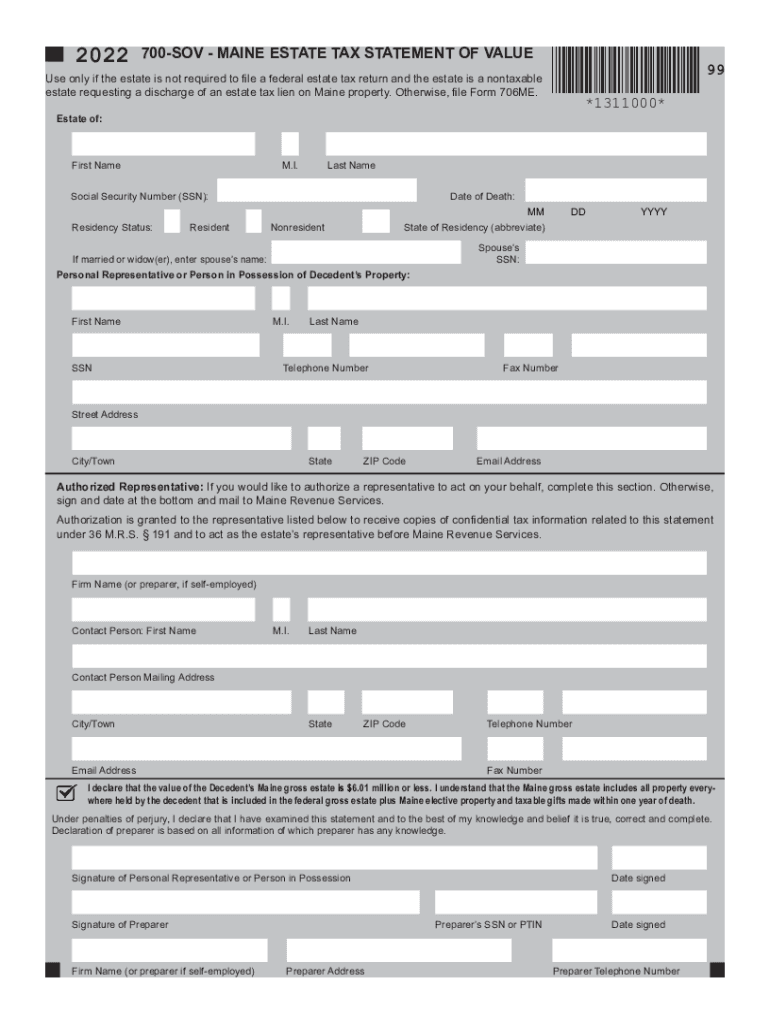

Steps to Complete the Maine Revenue SOV

- Gather Required Information: Start by collecting essential details, such as the decedent's personal information, estate valuation, and any existing liens or claims against the estate.

- Download Form 700-SOV: Access the form through the Maine Revenue Services website or request a physical copy if preferred. Ensure that the latest version of the form is used to meet current regulatory standards.

- Complete Personal and Estate Details: Fill out sections related to the deceased’s personal information and enumerating all pertinent estate assets, including real and personal property.

- Provide Valuation Information: Offer detailed valuation of the entire estate, ensuring that it aligns with the current market value assessments.

- Signer and Representation Identification: Include information of the personal representative handling the estate, specifying their authority and contact details.

- Submit the Form: Once completed, submit the form electronically via the Maine Tax Portal or send a physical copy to the designated mailing address provided on the form's instructions.

How to Obtain the Maine Revenue SOV

To acquire the Maine Estate Tax Statement of Value, individuals and estate representatives can download the form directly from the Maine Revenue Services official website. For those preferring a tangible copy, contacting the Maine Revenue Services through their helpline or visiting a local tax office could also be beneficial methods of obtaining the document. Additionally, professional estate planners or tax advisors often have access to the form and can provide expertise in retrieving and completing it.

Key Elements of the Maine Revenue SOV

The Maine Revenue SOV form comprises several critical elements that must be accurately completed:

- Estate Identifying Information: This section captures all relevant information about the decedent, such as name, social security number, and date of death.

- Valuation of Estate: Requires a comprehensive listing of all estate holdings with appraised values to ensure the estate qualifies as nontaxable.

- Residency Status: Includes clarification on the residency status of the decedent, as it impacts the assessment and processing of the form.

- Authorized Signatories: Details of the personal representative or authorized individual responsible for the estate, validating their position to manage the estate matters.

Legal Use and Compliance

The legal framework surrounding the Maine Revenue SOV is grounded in estate tax laws specific to the state of Maine. Completing and submitting this form serves to confirm the estate's exemption from the state estate tax requirement; thus, ensuring compliance with applicable tax regulations. It is crucial for personal representatives and estate planners to adhere to these regulations to avoid potential legal ramifications, such as penalties or delays in settling the estate.

State-Specific Rules and Regulations

Maine state law dictates specific rules governing estate tax lien discharges. Notable regulations include the stipulation that estates must fall below the $6.01 million valuation to file Form 700-SOV. Additionally, there may be varying time constraints associated with the filing; timely submission is imperative to facilitate prompt processing and resolution of estate matters. It is advisable to consult state guidelines or a tax professional to fully understand these requirements.

Required Documents for Submission

When preparing the Maine Revenue SOV, several supporting documents must accompany the form submission:

- Death Certificate: A certified copy to authenticate the date and identity of the decedent.

- Appraisals or Valuation Reports: Proof of property valuation, underlining the estate’s worth.

- Letters of Administration or Testamentary: Demonstrating the rightful authority of the person managing the estate.

Filing Methods: Online or Mail

Maine offers multiple avenues for submitting Form 700-SOV to accommodate different preferences, including:

- Online Filing: Use the Maine Tax Portal for a streamlined digital submission process, which allows for real-time tracking and faster processing.

- Mail-In Option: For traditionalists, sending a hard copy via mail remains a viable and officially recognized method, though it may entail longer processing times.

Important Deadlines and Filing Dates

Timely submission of the Maine Revenue SOV is critical in ensuring the efficient processing and acceptance of the form. The filing should be completed shortly after the decedent’s passing, typically aligning with general estate settlement timelines. This measure is to prevent delays in handling liens and settling property affairs effectively.