Key Elements of the Utah TC-20S

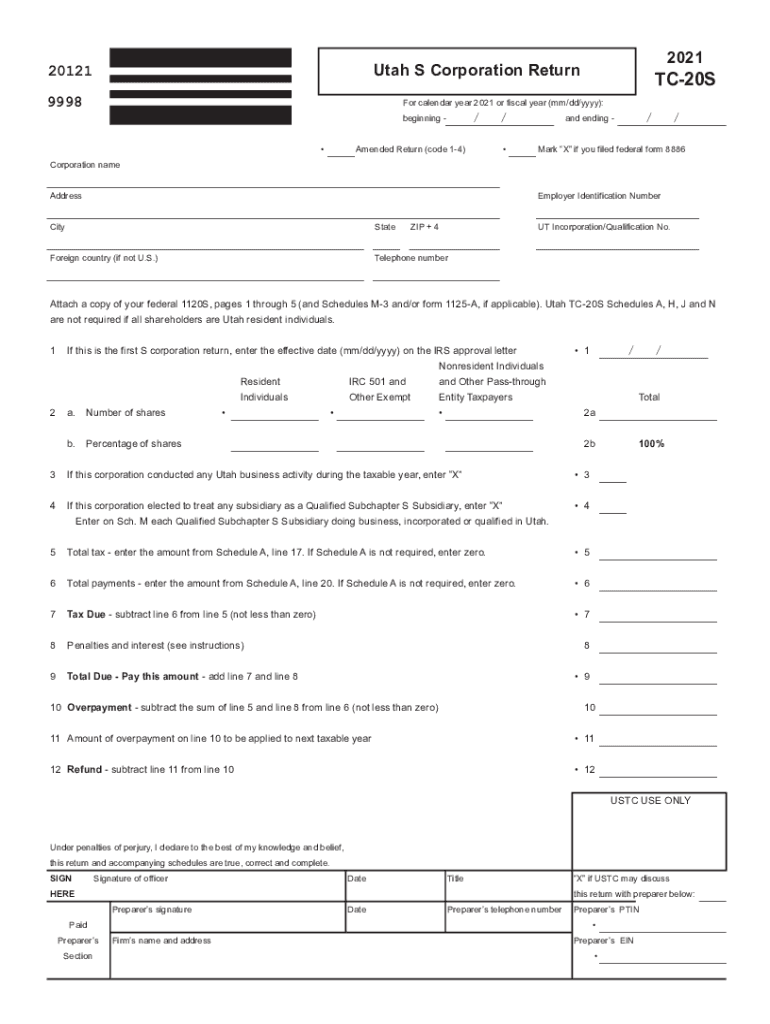

The Utah TC-20S form serves as the S Corporation Return for entities operating within the state of Utah. This document is pivotal for S corporations, as it meticulously outlines various critical financial and identification aspects that must be reported. These include:

-

Corporate Identification: This section requires the disclosure of identifying information about the S corporation, including its legal name and address, federal employer identification number (FEIN), and the state of incorporation. This ensures proper classification and identification by state tax authorities.

-

Income Reconciliation: Details the reconciliation of income reported between federal and state returns, accounting for any Utah-specific modifications. This is crucial for ensuring consistent and accurate reporting of earnings.

-

Tax Calculations: Highlights the method and figures for calculating state-specific taxes, ensuring the correct amount is determined based on Utah's corporate tax laws.

-

Shareholder Distributions: As S corporations pass their income, deductions, and credits to shareholders, documenting these distributions is essential for accurate tax processing.

-

Apportionment of Income: For companies operating in multiple states, this section addresses how income is apportioned to Utah, ensuring that tax liability aligns with Utah statutes.

Steps to Complete the Utah TC-20S

Completing the Utah TC-20S form is a critical task for S corporations to fulfill their state tax obligations. Here is a detailed guide to assist in this process:

-

Gather Necessary Information: Collect all pertinent financial documents, including the corporation’s income statements, schedules from federal tax returns, and records of shareholder distributions.

-

Fill Out Corporate Identification: Input the corporation’s standardized information, such as name, FEIN, and incorporation details, ensuring accuracy to prevent filing issues.

-

Reconcile Income: Transfer pertinent figures from the federal return and make any necessary state-specific adjustments to reflect true income subject to Utah tax.

-

Calculate Taxes Owed: Carefully follow the instructions to compute the taxes owed based on Utah’s tax code, utilizing any applicable credits or deductions.

-

Detail Shareholder Information: Document the allocation of income and deductions to each shareholder, to ensure transparency and compliance with distributive share rules.

-

Review and Submit: Double-check all entered information for accuracy, then submit the form via the chosen method, be it electronic or paper submission.

Who Typically Uses the Utah TC-20S

The Utah TC-20S form is specifically designed for S corporations conducting business within the state of Utah. Entities that are legally classified as S corporations benefit from this form as it allows them to report their allocated income, credits, and deductions to their shareholders without doubly taxing this income at the corporate level. Typically, the users include:

-

Small to Medium-sized Business Owners: Those who have opted for S corporation status aiming to leverage pass-through taxation benefits.

-

Tax Professionals and CPA Firms: Accountants and tax advisors working with S corporation clients in Utah for compliance and optimization of tax matters.

State-Specific Rules for the Utah TC-20S

Operating in Utah requires adherence to unique state-specific tax guidelines that differ from federal regulations. These rules impact the completion of the Utah TC-20S form:

-

Nonbusiness Income Taxation: Utah has specific instructions for reporting nonbusiness income, which may be taxed differently compared to business income, increasing compliance complexity.

-

Utah-specific Deductions and Credits: Certain deductions and credits are exclusive to Utah, requiring careful identification and application to reduce taxable income.

Important Terms Related to the Utah TC-20S

Understanding key terms is essential for correctly completing the Utah TC-20S:

-

Apportionment: The method used to divide income among states where the corporation conducts business, important for calculating state tax liability.

-

Distributive Share: Refers to each shareholder’s portion of the corporation's income, deductions, and credits, crucial for personal tax filings.

-

FEIN (Federal Employer Identification Number): This unique identifier is necessary for all corporate tax filings and must be accurately reported.

Filing Deadlines and Important Dates

S corporations in Utah must be diligent about meeting state-imposed deadlines to avoid penalties:

-

Filing Date: The Utah TC-20S typically shares the same federal deadline, March 15th, but if this date falls on a weekend or holiday, businesses should check for an adjusted due date.

-

Extension Requests: If unable to meet the deadline, corporations may file for a state-approved extension, aligning with federal extension procedures but potentially requiring separate documentation.

Penalties for Non-Compliance

Failure to comply with Utah state tax regulations concerning the Utah TC-20S can result in significant consequences:

-

Late Filing Penalties: Penalties for filing past the deadline without an extension can accumulate rapidly, often based on a percentage of the unpaid tax.

-

Inaccurate Reporting: Misreported information can lead to audits and additional fines, necessitating precise and accurate documentation on the return.

Digital vs. Paper Version of the Utah TC-20S

In an increasingly digital world, the method chosen to file the Utah TC-20S can impact efficiency and accuracy:

-

Digital Submission: Filing electronically can ensure faster processing and confirmation of receipt, while also reducing the potential for errors through built-in validation checks.

-

Paper Filing: Traditional paper submissions remain available, but they might involve longer processing times and lack the immediate feedback afforded by digital systems.