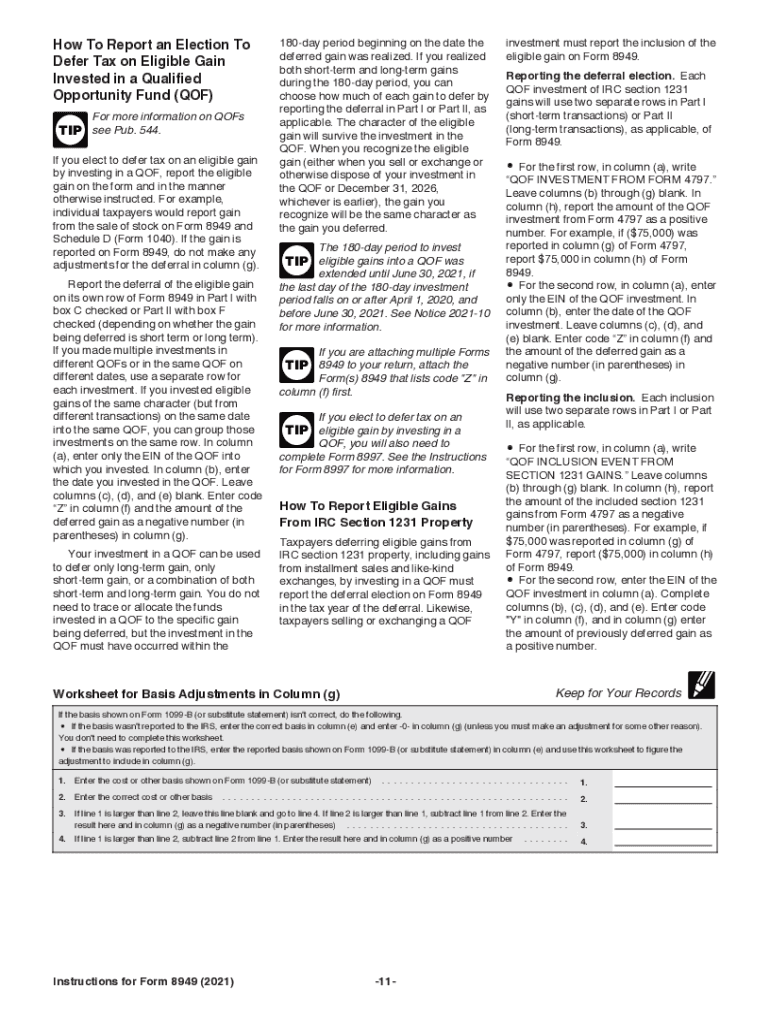

Definition and Meaning

Form 8949, officially known as "Sales and Other Dispositions of Capital Assets," is used to report capital gains and losses from the sale or exchange of property. Individuals, corporations, partnerships, estates, and trusts must accurately complete this form, especially when they have realized gains or losses on capital assets throughout the tax year. The form is integral to calculating adjustments to income when it comes to the selling price or cost basis of the sold property. Ensuring accuracy here is crucial as these figures directly affect the taxpayer's liability or refund status. Additionally, Form 8949 serves to detail transactions that are otherwise not fully covered on Schedule D, which is specifically for capital gains and losses.

How to Use Form 8949 Instructions

Using Form 8949 instructions effectively requires familiarity with the various parts and columns of the form. The instructions guide users through listing all sales, exchanges, and dispositions of capital assets. Each transaction should be entered on a separate line, along with the corresponding details such as description of property, date acquired, date sold, and sales price. Additionally, the cost or other basis must be recorded, which includes any necessary adjustments. Taxpayers must also determine whether a transaction falls under short-term or long-term. Short-term covers assets held for one year or less, while long-term pertains to those held for over one year. The instructions facilitate this process by explaining the purpose and use of specific codes that denote adjustments and necessary calculations for precise reporting.

Steps to Complete Form 8949

-

Gather Required Information: Collect documents and records such as brokerage statements and purchase and sale receipts, which provide essential details for each transaction.

-

Identify Transaction Type: Determine whether each transaction is a short-term or long-term gain or loss based on the period the asset was held.

-

Enter Transaction Details: For each sale or exchange, fill out relevant columns, including description, dates, selling price, and original purchase cost or basis.

-

Apply Adjustments: Use IRS codes for any necessary adjustments due to returned capital, disallowed loss, or wash sale rules, and enter these adjustments in their respective columns.

-

Calculate Totals: Add up all entries for each type of transaction and input these figures at the bottom of each section (Part I for short-term and Part II for long-term).

-

Transfer Totals to Schedule D: Once Form 8949 is completed, summarize the totals on Schedule D to report capital gains and losses on the tax return.

-

Review and Submit: Carefully review all entries for accuracy, and submit the form alongside Schedule D as part of your tax return submission.

IRS Guidelines

The IRS provides detailed guidelines for filing Form 8949, emphasizing accuracy and completeness in reporting. Taxpayers must include each sale or disposition that cannot be reported directly on Schedule D due to adjustments or atypical circumstances. The IRS mandates that each entry must be supported by documentation such as broker statements or Form 1099-B, which reports proceeds from broker transactions. Furthermore, taxpayers must follow IRS instructions for categorizing transactions correctly into short-term or long-term classifications and applying appropriate codes for adjustments. Compliance with these guidelines ensures correct tax computation and minimizes the risk of penalties due to errors or omissions in reporting.

Penalties for Non-Compliance

Failing to comply with IRS requirements for Form 8949 can result in penalties, including fines and additional scrutiny under audits. Misreporting capital gains and losses, neglecting to file the form altogether, or omitting necessary information are common triggers for penalties. The IRS may impose fines based on the degree of non-compliance, and unpaid taxes resulting from underreporting may accrue interest and late fees. Additionally, consistent or serious filing issues could attract more comprehensive investigations. To avoid such consequences, ensuring accurate and thorough completion of Form 8949 as per the guidelines is imperative.

Software Compatibility

Several accounting software platforms, including TurboTax and QuickBooks, support Form 8949 preparation by streamlining data entry and calculating necessary adjustments. These platforms offer step-by-step assistance, importing information directly from financial institutions or uploading documents like Form 1099-B, to accurately auto-populate Form 8949 fields. This compatibility reduces manual input errors and ensures calculations align with IRS standards. By leveraging such tools, users can simplify complex reporting requirements, maintain accurate tax records, and efficiently finalize their tax responsibilities.

Required Documents

Completing Form 8949 requires an array of documents:

- Brokerage Statements (e.g., Form 1099-B): Detail proceeds and cost basis from securities transactions.

- Purchase Receipts: Confirm original purchase price and date of acquisition for each asset.

- Sales Records: Provide details such as sale price and date of disposition.

- Adjustment Evidence: Proof for any applied adjustments, like wash sale losses or return of capital events. Maintaining organized documentation helps ensure accuracy and supports figures stated on Form 8949 in the event of an IRS query.

Important Terms Related to Form 8949 Instructions

Familiarity with specific terms is crucial when filling out Form 8949:

- Capital Asset: Any asset owned for personal or investment purposes, including stocks, bonds, real estate, and collectibles.

- Short-term Gain/Loss: Results from selling assets held for one year or less.

- Long-term Gain/Loss: Derives from assets held longer than a year.

- Cost Basis: The original value of an asset, including purchase price, commissions, and other relevant adjustments. Understanding these terms aids in accurately categorizing and reporting transactions according to IRS requirements.