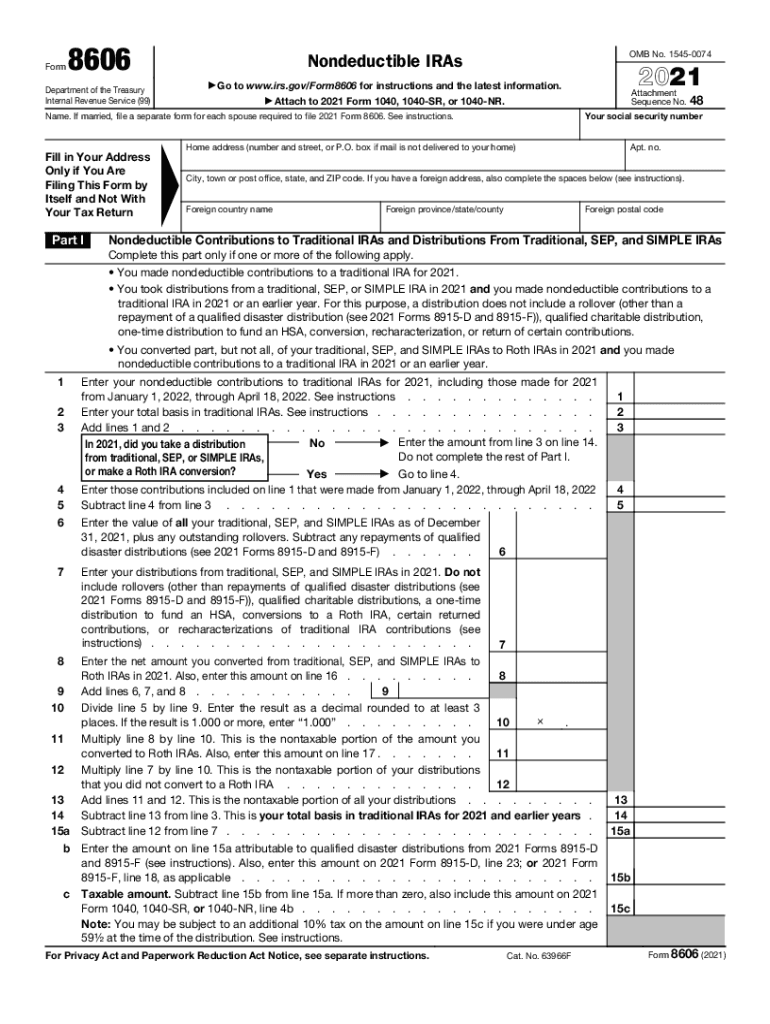

Definition and Purpose of Form 8606

Form 8606, officially titled "Nondeductible IRAs," is integral for U.S. taxpayers to report nondeductible contributions to traditional IRAs along with distributions from various IRAs, including Roth, SEP, and SIMPLE IRAs. It's particularly relevant for taxpayers who make after-tax contributions to a traditional IRA and need to report those contributions to avoid paying taxes on them twice. This form ensures correct reporting for conversions to Roth IRAs and calculating taxes on distributions from Roth IRAs. It’s a vital part of tax filing for individuals managing complex retirement accounts, and understanding its purpose can prevent potential double taxation.

How to Use Form 8606

Using Form 8606 involves several key steps specific to contributing and distributing money from IRAs. The form helps compute different sections:

-

Nondeductible Contributions: Fill in Part I for nondeductible contributions to a traditional IRA. Even if you don't deduct these contributions, reporting them keeps a record of your basis in the IRA.

-

Conversions: Use Part II to report conversions from traditional, SEP, or SIMPLE IRAs to a Roth IRA. This part calculates the taxable portion of the conversion.

-

Distributions: For Roth IRAs, Part III is used to report distributions and calculate any taxable amount. It establishes whether the holding periods for gains are fulfilled.

-

Coordination: Coordinate this form with your Form 1040 or Form 1040-SR, where the primary tax information is filed.

The use of Form 8606 is essential in maintaining accurate records with the IRS regarding IRA contributions and distributions, ensuring that taxpayers are taxed correctly based on their actual economic gains.

Steps to Complete Form 8606

Completing Form 8606 involves several detailed steps, primarily informed by your IRA activities:

-

Gather Required Information: Collect all documentation related to IRA contributions, withdrawals, and conversions, including records from previous years if carry-forward contributions are considered.

-

Fill in Contributions: Input nondeductible contributions in Part I, ensuring all amounts are correctly recorded and reported.

-

Report Conversions and Rollovers: Complete Part II with conversion and rollover amounts to account for any potential taxable portions.

-

Calculate Taxable Amounts: Calculate all taxable elements accurately as parts of the form guide you through figure computation based on regulations.

-

Review and Attach: Attach Form 8606 securely to your income tax return, such as Form 1040, ensuring all figures correlate accurately with your tax filing.

IRS Guidelines and Eligibility Criteria

The IRS provides comprehensive guidelines on who needs to file Form 8606, based on various IRA-related actions:

- Eligibility: Taxpayers with nondeductible contributions to a traditional IRA or those who have taken distributions from a Roth IRA.

- Guidelines: Available on the IRS website, understanding the complete instructions is crucial for accurate reporting. This includes thoroughly reviewing IRS Publication 590 for IRAs, which provides detailed IRA contribution and distribution rules.

- Age and Contribution Limits: Adhering to contribution limits and age-related rules (such as age 59½ for penalty-free distributions) is imperative.

Failure to comply with IRS guidelines for Form 8606 can lead to inaccuracies in tax filings, possible penalties, and additional interest charges.

Important Terms Related to Form 8606

Understanding important terms aids in properly navigating Form 8606:

-

Nondeductible Contribution: A contribution to a traditional IRA that doesn’t qualify for a tax deduction but is reported for basis calculation.

-

IRA Basis: The sum of money in an IRA account not subject to taxes again since taxes have already been paid on it.

-

Conversion: The process of changing a traditional IRA to a Roth IRA, often resulting in taxable income unless basis exists.

-

Distribution: Withdrawals from an IRA, which may be subject to taxes and penalties if the necessary conditions aren't met.

These terms are vital in completing the form accurately and ensuring compliance with IRS regulations.

Filing Deadlines and Important Dates

Understanding the filing deadlines for Form 8606 ensures timely compliance:

-

Federal Tax Deadline: Typically due by April 15th of the year following the tax year, unless an extension is filed.

-

IRA Contribution Deadline: Contributions to be reported on the form should be made by the tax filing deadline (not including extensions), usually April 15th, for the previous tax year.

-

Extensions: Filing an extension using Form 4868 gives extra time to file Form 8606, generally until October 15th.

Meeting these deadlines avoids penalties and interest on underpaid taxes.

Penalties for Non-Compliance

Failing to file Form 8606 when required can result in significant penalties:

-

Monetary Penalties: A $50 penalty for failing to file the form when it's required to report nondeductible contributions or distributions.

-

Interest: Additional interest might accrue due to resulting understated taxes.

-

Compliance Costs: Overlooking compliance can lead to double taxation if nondeductible contributions aren't reported, as well as additional future tax complications.

Ensuring compliance with filing requirements is crucial to avoid unnecessary financial penalties.

Key Elements of Form 8606

Form 8606 comprises several key components that need careful attention:

-

Part I: Covers nondeductible contributions to traditional IRAs, establishing a record of these contributions for taxation purposes.

-

Part II: Deals with the conversion of traditional IRAs to Roth IRAs, ensuring that any converted amounts are reported for tax purposes.

-

Part III: Focuses on Roth IRA distributions, helping calculate taxable portions of distributions.

-

Record-Keeping Sections: Several sections require ongoing records from past filings to corroborate basis and ensure future compliance.

Each section must be completed accurately to ensure that tax obligations are met without errors or omissions, aligning with IRS expectations for IRA management.