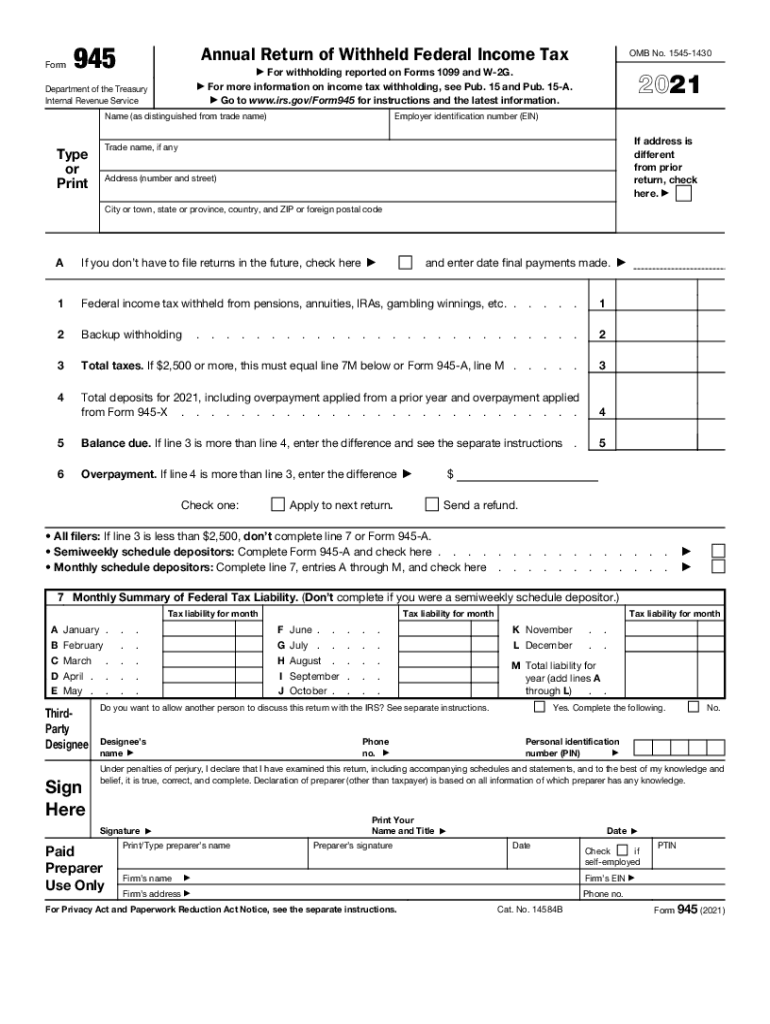

Definition and Purpose of Form 945

Form 945, officially known as the Annual Return of Withheld Federal Income Tax, is used by employers in the U.S. to report federal income tax withheld from nonpayroll payments. Nonpayroll payments typically include withheld taxes from gambling winnings, pensions, annuities, IRAs, and other similar disbursements. This form consolidates reporting for these specific tax liabilities, making it an essential tool for businesses managing various forms of income withholding.

Key Elements of Form 945

- Nonpayroll Payments: Covers withholding on pensions and annuities, as well as gambling winnings.

- Annual Reporting: Unlike payroll taxes reported more frequently, Form 945 is filed annually, summarizing nonpayroll tax withholding.

- Includes Form 945-V: A payment voucher for any outstanding balance, ensuring amounts are paid in tandem with filing.

Steps to Complete the Form 945

Completing Form 945 requires attention to detail and a clear understanding of applicable tax laws. The following steps provide guidance to accurately fill out the form:

- Gather Required Information: Collect details on all nonpayroll payments subject to withholding made through the year.

- Calculate Total Taxes Withheld: Sum the total amount of each type of withholding to ensure accurate reporting.

- Complete the Identification Section: Fill in the employer identification number (EIN), name, and address as registered with the IRS.

- Enter Financial Details: Record the total amount withheld from each category such as pensions and gambling winnings.

- Review IRS Instructions: Follow the tax tables and instructions provided by the IRS specific to the year being reported.

- Attach Form 945-V if Needed: Include the payment voucher with any additional taxes owed.

- Sign and Date: Verify accuracy before signing and dating the form to affirm all information is correct.

Filing Deadlines and Important Dates

The filing deadline for Form 945 is crucial to avoid penalties:

- Annual Deadline: Form 945 must be filed by January 31st of the year following the tax period.

- Payment Due: Any taxes due should accompany the form if not previously deposited. Late payments are subject to interest and penalties.

- Next Business Day: If the deadline falls on a weekend or legal holiday, the form is due the next business day.

Why Use Form 945

Employers must use Form 945 to comply with federal tax obligations when they have withholding responsibilities for nonpayroll payments. This form ensures:

- Accurate Reporting: Facilitates correct and IRS-compliant reporting of taxes withheld.

- Avoidance of Penalties: Shields businesses from penalties related to unreported or underreported withholdings.

- Efficient Record-Keeping: Streamlines the process of tax documentation and reconciliation for nonpayroll payments.

Who Typically Uses Form 945

Most commonly, Form 945 is used by:

- Businesses with Retirement Plans: Entities offering pensions or IRAs apply for withheld taxes.

- Gambling Establishments: Casinos and gaming businesses utilize this form for tax withheld on winnings.

- Trusts and Estates: These entities may report withheld income from beneficiaries.

IRS Guidelines for Completing Form 945

The IRS offers detailed instructions and guidelines to aid in the completion of Form 945. Critical aspects include:

- Understanding Thresholds: Knowing the withholding thresholds for different payment types.

- Using Correct Tax Tables: Applying the accurate tax tables for the year and specific nonpayroll payments.

- Compliant Record-Keeping: Ensuring thorough documentation of all reported figures.

Penalties for Non-Compliance

Failure to complete Form 945 correctly or timely can result in penalties:

- Late Filing Penalty: Charged if the form is not filed by the due date; based on the amount owed.

- Underpayment Penalty: Incurred if insufficient tax is reported or paid.

- Interest Charges: Applied to any unpaid tax balance post the filing deadline.

Form Submission Methods

Form 945 offers flexibility in submission:

- Electronic Filing: The IRS e-file system supports electronic submission, providing a faster and traceable method.

- Postal Mail: Forms can also be sent via mail to the specified IRS mailing address.

- In-Person: Submission at IRS Taxpayer Assistance Centers is possible, typically by appointment.

Each method requires careful consideration of deadlines and documentation to ensure compliance with IRS regulations.