Definition and Meaning

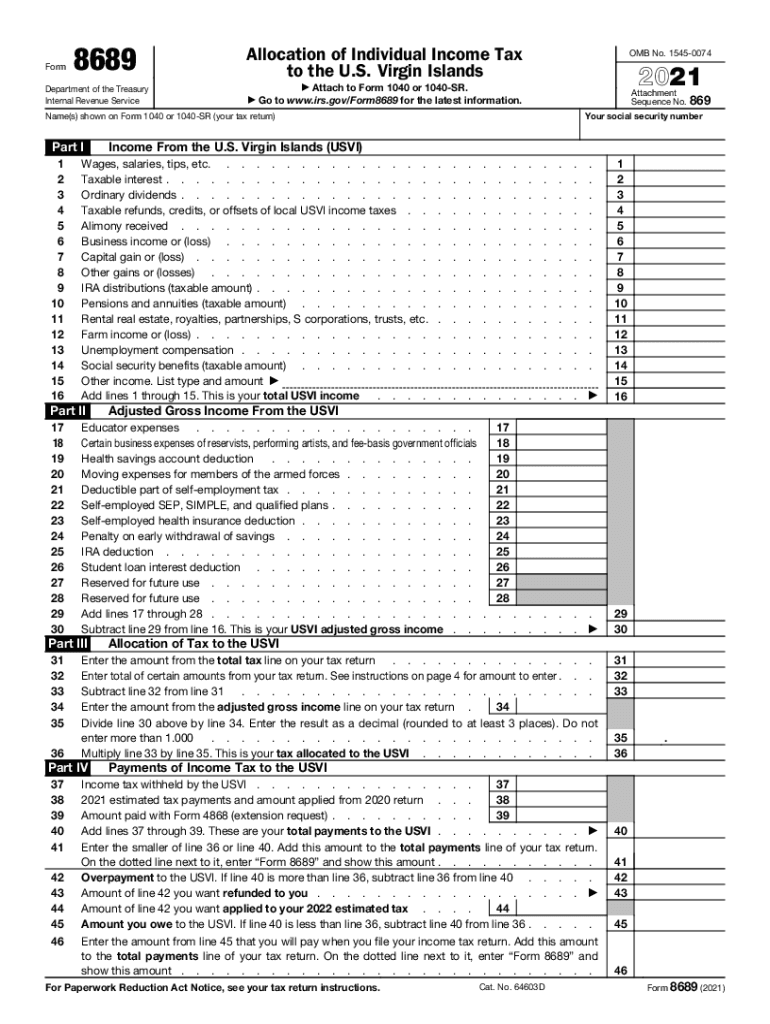

Form 8689 is a specific tax document utilized by U.S. citizens or resident aliens who need to calculate the portion of their individual income tax that applies to the U.S. Virgin Islands (USVI). This form is unique as it is used when an individual has income sourced from the USVI, and it helps determine the tax liabilities accordingly.

Purpose of Form 8689

- It identifies the amount of tax owed to the USVI based on the income earned there.

- It helps reconcile tax liabilities between the U.S. and the USVI.

- It ensures compliance with federal tax regulations for individuals with dual residency in the U.S. and USVI.

Key Terminologies

Income Sourced from USVI

- Income earned directly within the U.S. Virgin Islands, including wages, business revenues, and other income types sourced there.

Adjusted Gross Income (AGI)

- The total income of an individual, minus specific deductions, as recognized by the IRS and adjusted for USVI income specifics.

How to Use Form 8689

Understanding the proper use of Form 8689 involves recognizing its primary function in calculating taxes attributable to the USVI. It's essential for U.S. citizens with economic activities linked to the USVI.

Step-by-Step Instructions

-

Gather Income Information:

- Collect all relevant income documents from both the U.S. and the USVI.

- Determine the portion of income specifically garnered from activities or employment in the USVI.

-

Calculate Adjusted Gross Income:

- Follow the IRS guidelines and instructions provided with the form to adjust the gross income for any applicable deductions.

-

Complete Form Fields:

- Accurately fill out all required sections of the form, reflecting the calculated tax liabilities and income sources.

Practical Scenarios

- An individual employed in the USVI for part of the year must use this form to allocate part of their annual taxes to the USVI.

- A business owner with operations in both the U.S. and the USVI needs to separately calculate the tax responsibilities per jurisdiction.

Steps to Complete Form 8689

Completing this form requires attention to detail and an understanding of specific tax codes. The following subsections offer a comprehensive guide.

Gathering Necessary Information

- Ensure all income documents, tax returns, and financial records from the USVI and the U.S. are accessible.

- Include any previous adjustments or credits applicable to federal taxes.

Filling Out the Form

-

Personal Information:

- Enter your full name, Social Security Number, and address.

-

Income Allocation:

- Distinguish income amounts between those earned in the USVI and the U.S.

-

Deduction Entries:

- Apply allowable deductions for accurate AGI calculations.

-

Tax Computation:

- Use the form's guidelines to compute the tax allocated to the USVI.

Verifying and Submission

- Double-check all entries for accuracy.

- Attach Form 8689 with your primary tax forms, such as Form 1040 or 1040-SR.

Important Terms Related to Form 8689

Several terms are pivotal for correctly understanding and using Form 8689, including:

Dual Residency

- Refers to maintaining legal residential status in more than one jurisdiction, particularly the U.S. and USVI.

Foreign Tax Credit

- A tax credit for taxes paid to a foreign government, which can be utilized to avoid double taxation on the same income.

IRS Guidelines

Understanding IRS guidelines specific to Form 8689 is crucial for compliance with federal tax laws. These guidelines determine:

Eligibility for Dual Filings

- Criteria defining who must file taxes with both the U.S. and the USVI.

Correct Calculation Methods

- Mandatory methodologies for calculating taxes attributable to income from the USVI.

Filing Deadlines and Important Dates

Form 8689 adheres to rigid federal deadlines.

Typical Deadlines

- Final submission aligns with federal tax deadline dates, generally April 15th.

Extensions

- Possible extensions available through formal IRS requests, prolonging filing dates without penalties.

Required Documents for Filing

The successful filing of Form 8689 demands assembling requisite documentation.

Core Documents

- Income records from both jurisdictions.

- Previous tax records if available.

Additional Resources

- Access to any form-specific instructions or IRS guidelines available at IRS offices or online portals.

Penalties for Non-Compliance

Consequences for failing to file Form 8689 properly can include significant penalties.

Common Penalties

- Monetary fines based on the outstanding tax owed.

- Potential audits resulting from neglect to disclose income sources accurately.

By adhering to these concise guidelines, taxpayers utilizing Form 8689 can manage and fulfill their dual taxation duties effectively, ensuring legal compliance across jurisdictions.