Definition and Purpose of the 1997 IRS Form

The 1997 IRS Form 1040 is the official document used by U.S. taxpayers to file their annual federal income tax returns. This form enables individuals to report their income, claim deductions and credits, and calculate their tax obligations or potential refunds for the tax year 1997. It is a comprehensive form that includes sections for various types of income, allowed deductions, and credits, making it essential for ensuring compliance with federal tax laws.

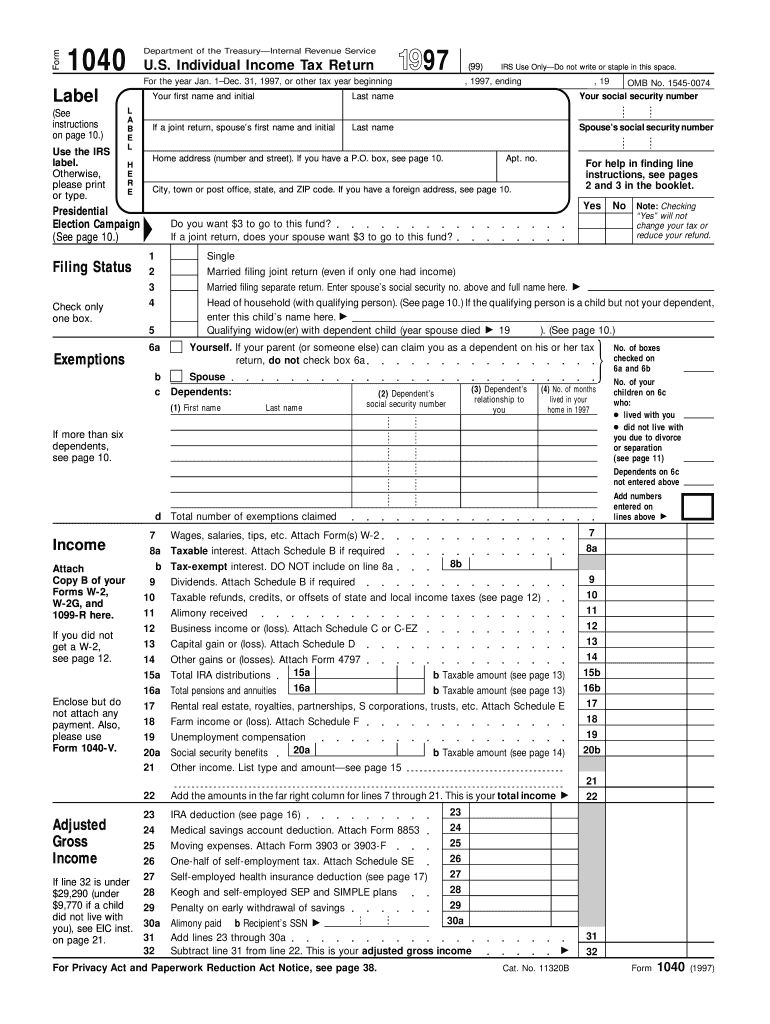

Key Components of the 1997 IRS Form

The 1040 form for 1997 includes several critical sections:

- Personal Information: Requires your name, Social Security number, and filing status.

- Income Reporting: Captures all income types such as wages, interest, dividends, and capital gains.

- Tax Computation: Involves calculating your adjusted gross income and taxable income.

- Tax Credits and Payments: Allows you to claim available tax credits and report any taxes already paid.

Understanding these components is vital for accurate completion and compliance.

How to Obtain the 1997 IRS Form

To obtain the 1997 IRS Form 1040, taxpayers could order a copy from the IRS by mail or download it from the IRS website if available in the archives. Alternatively, some tax preparation software and services may offer access to prior-year forms, ensuring historical compliance.

Steps to Complete the 1997 IRS Form

- Gather Required Documents: Collect your W-2s, 1099s, and any other income documentation.

- Fill Out Personal Information: Enter your name, social security number, and address.

- Report Income: Input your earnings from various sources, ensuring accuracy.

- Calculate Deductions and Credits: Determine the deductions and credits you qualify for to reduce taxable income.

- Compute Final Tax Liability: Use the form’s instructions to calculate your total tax owed or refund due.

- Verify and Sign: Double-check all entries for accuracy and sign the document.

Understanding the Legal Use of the 1997 IRS Form

The 1997 IRS Form 1040 is legally required for any individual who earned above a certain threshold in 1997 and needs to report their income to the IRS. It ensures that taxpayers fulfill their legal obligations by accurately reporting and paying their federal taxes.

IRS Guidelines for Completing the 1997 IRS Form

The IRS provides extensive guidelines which include:

- Eligibility Criteria: Clarifies who must file, based on income and other factors.

- Deductions and Credits: Outlines which ones are available and the associated limits.

- Filing Instructions: Provides specific instructions on how to fill out each section and where to send the completed form.

These guidelines are crucial for preventing errors and ensuring compliance.

Critical Filing Deadlines for the 1997 IRS Form

Typically, the deadline for filing the 1997 IRS Form was April 15, 1998. If you were unable to meet this deadline, the IRS offered extensions; however, these required timely application. Missing the deadlines could lead to penalties and interest charges on any taxes owed.

Penalties for Non-Compliance with the 1997 IRS Form

Failure to file the 1997 IRS Form 1040 or pay the due taxes can result in various penalties:

- Late Filing Penalty: Imposed on taxpayers who fail to file by the deadline.

- Late Payment Penalty: Charged if taxes are not paid by the due date.

- Interest Charges: Accrue on unpaid tax balances from the original deadline until paid in full.

Understanding these penalties emphasizes the importance of timely and accurate filing.

Taxpayer Scenarios and the 1997 IRS Form

Different taxpayer scenarios affected how one might interact with the 1997 IRS Form:

- Self-Employed Individuals: Required to report income and expenses using additional forms such as Schedule C.

- Retirees: Needed to include distributions from retirement accounts.

- Students: May be eligible for specific education-related credits or deductions.

Knowing these differences can aid in precise completion and maximize tax benefits.