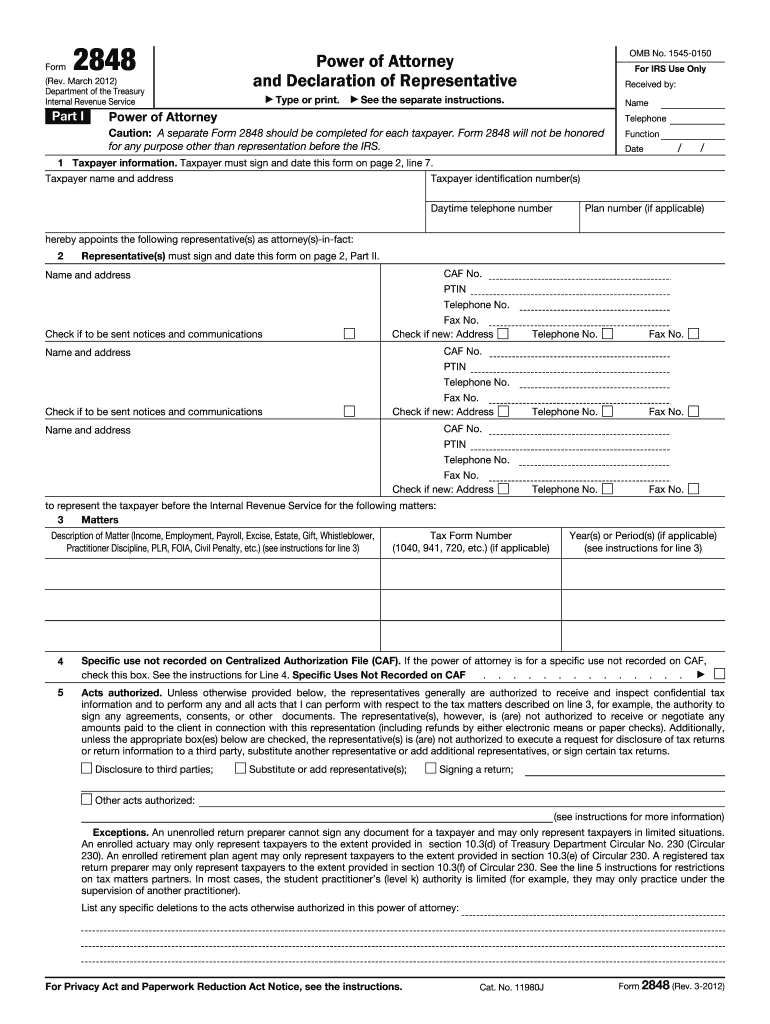

Definition and Purpose of Form 2848

Form 2848 is known as the Power of Attorney and Declaration of Representative. It is used by taxpayers in the United States to appoint one or more individuals to represent them before the Internal Revenue Service (IRS). This form allows designated representatives to perform specific acts on behalf of the taxpayer, including the ability to receive confidential tax information, perform analyses, and engage in tax-related discussions with the IRS. By utilizing this form, taxpayers ensure that their affairs are handled in a professional manner, with representatives who are authorized to act in their best interest.

Key Features

- Authority Granting: Allows a taxpayer to authorize another person to represent them and make tax-related decisions.

- Identification: Requires detailed information about both the taxpayer and the representative, ensuring both parties are clearly identified.

- Representation Scope: Outlines the specific tax matters and years covered by the representative's authorized actions.

How to Use the 2848 Form 2012

Using Form 2848 requires careful completion and submission to the IRS. The taxpayer must specify the extent of authority granted to their representative, which can include specific tax years, types of filings, and actions allowed. Once filled out, the form can be submitted through various channels, depending on the urgency and nature of the representation needed.

Submission Methods

- Online Submission: Taxpayers can submit Form 2848 electronically, which ensures a quicker processing time.

- Mail: Forms can be mailed directly to designated IRS offices, but this method may take longer to process.

- In-Person: Submission at an IRS office offers direct communication and confirmation of receipt.

Steps to Complete the 2848 Form 2012

- Enter Personal Information: Begin by filling in the taxpayer's and representative's names, addresses, and identification numbers.

- Define the Scope: Specify the tax matters, years, or periods covered by this power of attorney.

- Signature: Both the taxpayer and the representative must sign and date the form.

- Submit: Choose the preferred submission method and send the completed form to the IRS.

Detailed Instructions

- Identification Details: Include Social Security numbers or Employer Identification Numbers to ensure proper identification.

- Tax Matters: Clearly detail the tax issues and periods involved to prevent any ambiguity.

- Authorized Acts: Define what the representative is allowed to perform, such as negotiations, information disclosure, etc.

Who Typically Uses the 2848 Form 2012

Form 2848 is primarily utilized by individuals who anticipate the need for external representation in dealings with the IRS. This includes:

- Taxpayers who require assistance from professionals in resolving complex tax issues.

- Certified Public Accountants (CPAs) and tax attorneys hired to manage substantial tax disputes.

- Estate Executors or trustees needing to handle the tax affairs of a deceased individual.

- Businesses, such as partnerships or corporations, relying on accountants or legal representatives for IRS communications.

Important Terms Related to Form 2848

Understanding specific terminology is crucial for accurately completing and using Form 2848. Important terms include:

- Power of Attorney: The legal authorization for one person to act on behalf of another.

- Declaration of Representative: The part of the form where the chosen representative asserts their understanding and acceptance of the responsibilities involved.

- Tax Matters: Any specific area of taxation, like audits or appeals, addressed by the form.

Legal Use and Obligations

The authorized representative, once appointed through Form 2848, must adhere to legal and ethical standards. This involves accurately representing the taxpayer's interests, maintaining confidentiality, and not exceeding the powers granted by the form. Misuse or overstepping of boundaries could result in penalties or revocations.

Obligations of a Representative

- Fiduciary Duty: The representative must act in the best interest of the taxpayer.

- Compliance with IRS Regulations: Adhere strictly to the outlined capabilities specified in the form, avoiding unauthorized acts.

Key Elements of the 2848 Form 2012

Several critical sections within the form define its comprehensiveness and ensure it is processed correctly by the IRS:

- Taxpayer Information: Detailed in Part I, ensuring clarity on who is granting the power of attorney.

- Representative Details: Part II catalogs the representative's credentials, ensuring they are eligible to represent the taxpayer.

- Jurisdiction and Authority: Part III is essential for illustrating the scope and limits of the authority granted.

IRS Guidelines for Form 2848

The IRS has specific guidelines that dictate how Form 2848 should be completed and submitted. These include:

- Required Signatures: The necessity for original signatures before the IRS registers the power of attorney.

- Modification and Revocation: Instructions on how to modify existing powers of attorney or revoke them if needed.

Understanding these guidelines ensures that the Form 2848 is completed according to federal tax laws, preventing any unnecessary delays in processing.