Definition and Purpose of Form 941-SS

Form 941-SS is an Employer's Quarterly Federal Tax Return specifically designed for employers operating in American Samoa, Guam, the Northern Mariana Islands, and the U.S. Virgin Islands. It is used to report wages paid to employees, tips received, and other taxable compensations. The form also calculates social security and Medicare taxes owed by both the employer and employees. Moreover, it includes adjustments for prior tax periods and accounts for credits applicable to employment taxes.

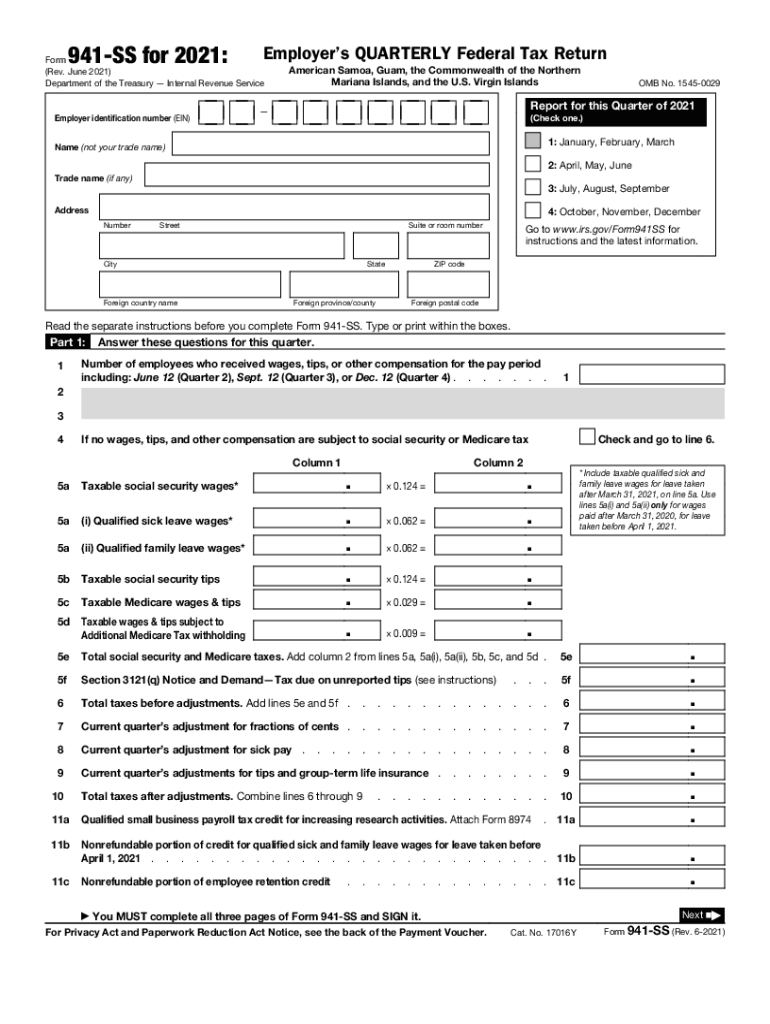

Key Components of the Form

- Employee and Employer Information: This section requires accurate personal and business details, including the Employer Identification Number (EIN).

- Wage Reporting: Employers must declare total wages, tips, and other forms of compensation paid within the quarter.

- Tax Calculation: This involves determining the correct amount of social security and Medicare taxes due.

- Adjustments and Credits: Employers can adjust for overpaid or underpaid taxes from previous quarters and claim credits for eligible causes.

How to Use Form 941-SS Effectively

Filling out Form 941-SS correctly requires a methodical approach. Employers should begin by gathering accurate payroll data for the entire quarter. This data will ensure precision in declaring total wages and calculating taxable amounts. Using payroll software often simplifies this process by automatically tallying totals and taxes.

Best Practices for Form Completion

- Review Prior Returns: Check previous Form 941-SS submissions for accuracy in reporting and adjust current filings accordingly.

- Ensure Consistency with Payroll Records: Compare wages reported on the form with payroll records to catch any discrepancies.

- Use Financial Software: Leverage tools like QuickBooks or other accounting software to automate calculations and minimize errors.

Steps to Complete Form 941-SS

Completing Form 941-SS involves several clear steps to ensure compliance and accuracy:

- Gather Necessary Documentation: Payroll records, tax withholding details, and other pertinent financial documents.

- Fill Employer Details: Carefully complete business information including EIN and company name.

- Report Wages and Tips: Enter total wages, tips, and any other compensation paid during the quarter in the designated sections.

- Calculate Taxes Owed: Use the form to compute total taxes owed, including social security and Medicare contributions.

- Adjustments for Previous Quarters: Include any necessary adjustments for corrections from previous quarters.

- Review and Sign: Carefully check the entire document for errors before signing and dating the form.

Accuracy Tips

- Double-check Numbers: Before submission, verify all amounts for accuracy.

- Consult with a Tax Professional: For complex situations, seek expertise to avoid errors.

Important Deadlines and Dates

Filing deadlines for Form 941-SS are critical to avoid penalties. The form must be filed quarterly with specific deadlines: April 30 for the first quarter, July 31 for the second, October 31 for the third, and January 31 for the fourth.

Late Filing Consequences

- Penalties: Late submissions may result in financial penalties.

- Interest on Unpaid Taxes: Accrued interest on outstanding tax amounts begins after the due date.

Obtaining Form 941-SS

Employers can obtain Form 941-SS through the IRS website, where it is available as a downloadable PDF. It can also be requested by mail from the IRS or picked up from local IRS offices.

Methods of Submission

There are multiple ways to submit Form 941-SS:

- Electronic Filing: The most efficient and secure method, often done via IRS-approved software providers.

- Mail Submission: Hard copies can be mailed to the designated IRS address.

- In-Person: Submission at an IRS office if necessary.

Legal Obligations and Compliance

Employers must comply with federal tax laws when using Form 941-SS, adhering to all guidelines regarding reportable wages, tax rates, and applicable credits. The IRS provides detailed instructions on their website to aid in compliance.

Penalties for Non-Compliance

Failure to file Form 941-SS or underreporting can lead to hefty penalties. Misreporting may elicit fines ranging from 2% to 15% of the underreported amount, depending on the timeliness of corrections.

- Non-Filing Penalty: An additional charge of 5% of the unpaid tax for each month or part of a month that a return is late.

- Fraudulent Intent: In cases where the IRS detects intent to defraud, penalties increase significantly.

Variants and Alternatives to Form 941-SS

While Form 941-SS is specific to certain U.S. territories, employers in other regions typically use Form 941, which serves a similar purpose. It's important to select the correct form to reflect regional tax obligations accurately.

Eligibility for Using Form 941-SS

Employers in American Samoa, Guam, the Commonwealth of the Northern Mariana Islands, and the U.S. Virgin Islands who pay wages subject to social security and Medicare taxes are required to use this form. Specific guidelines apply to the eligibility for credits and adjustments detailed within the form.