Definition & Meaning

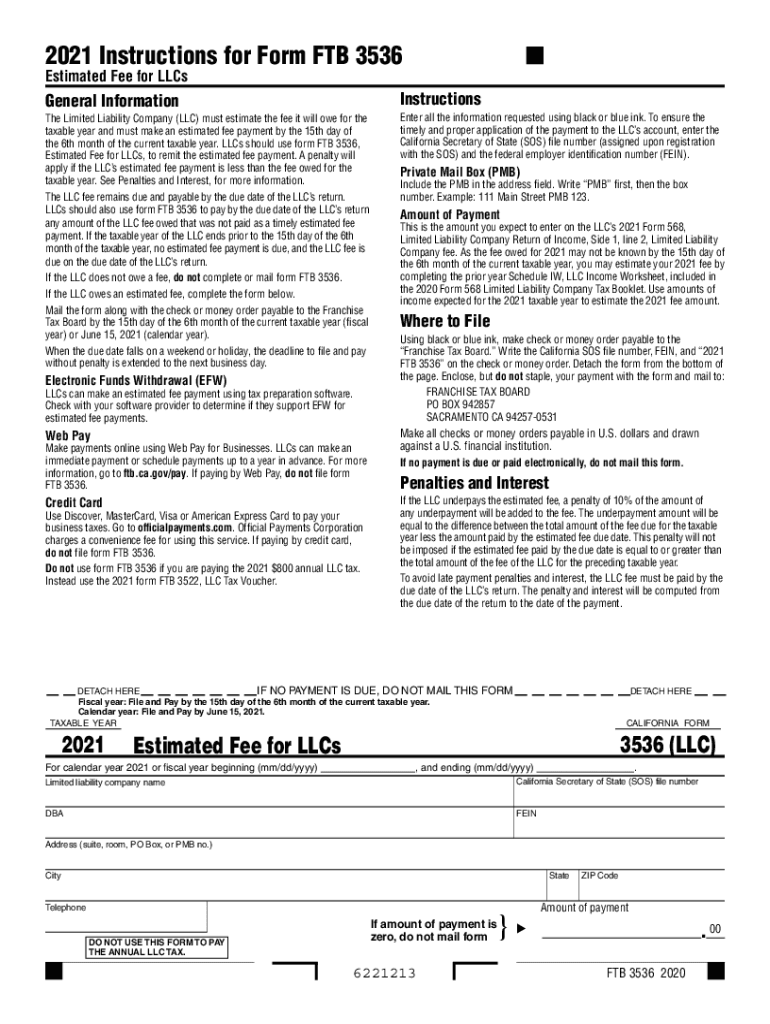

The FTB 3536 form is a document utilized by Limited Liability Companies (LLCs) in California to estimate and pay the LLC fee due for the taxable year. This form is mandated by the California Franchise Tax Board (FTB) and serves as a mechanism to ensure that LLCs remit their estimated fees in a timely manner. The form holds significance for LLCs as it is directly tied to the income and operations of the business within California. Failure to properly estimate and remit these fees can result in penalties.

How to Use the FTB 3536

LLCs in California can use Form FTB 3536 to estimate and pay the appropriate fee based on their total income. The process involves calculating the estimated fee for the current taxable year by considering the company's estimated income derived from or attributable to sources within California. It is essential to accurately project expected income to avoid potential underpayment penalties. Once calculated, the estimated fee is submitted using the form, ensuring compliance with state requirements.

Steps to Complete the FTB 3536

- Calculate Estimated Income: Determine the expected total income for the taxable year that is sourced from California.

- Determine Estimated Fee: Based on the income, refer to the fee schedule provided by the FTB to determine the applicable fee.

- Fill Out Personal and Company Information: Include details such as the LLC name, entity number, and contact information.

- Indicate Fee Amount: Clearly indicate the calculated fee amount on the form.

- Submit the Form and Payment: Choose an appropriate submission method and send the completed form along with the fee payment by the specified deadline.

Why the FTB 3536 is Necessary

The FTB 3536 is necessitated by California law to ensure that LLCs contribute their fair share towards state revenues based on their business activities and income. This form assists in the timely collection of fees, which supports state budgets and infrastructures. By requiring an estimate, California helps LLCs avoid large tax bills at the end of the year, promoting financial predictability and compliance.

Penalties for Non-Compliance

Failing to submit the FTB 3536 or miscalculating the estimated fee may lead to penalties for underpayment. The California FTB assesses penalties based on the difference between the estimated fee paid and the actual fee due. Interest may also accrue on unpaid amounts. To avoid such penalties, LLCs are encouraged to carefully estimate their income and remit payments before the deadline.

Filing Deadlines / Important Dates

The FTB 3536 form must be submitted by the 15th day of the fourth month following the end of the LLC's taxable year. This deadline ensures that the estimated fees are paid early in the fiscal year, allowing adjustments if necessary during the annual tax filing. Meeting this deadline is crucial to maintaining good standing with the California FTB and avoiding penalties.

Legal Use of the FTB 3536

The form is legally required for all LLCs operating in California and is governed by state regulations. The California FTB mandates this form as part of the annual financial and compliance responsibilities of LLCs. Legal use of this form ensures that LLCs meet their obligations to state authorities and affirm their business's legal and financial standing in California.

State-Specific Rules for the FTB 3536

California has specific rules that govern the fee estimation and submission process for the FTB 3536. These rules are designed to accurately capture revenue generated by LLCs operating within the state. Understanding these rules is critical for accurately completing the form and mitigating the risk of audit or penalties. State-specific guidelines outline the thresholds for applicability of fees for different income brackets, and guidance is provided in FTB publications for detailed compliance.

Business Entity Types (LLC, Corp, Partnership)

The FTB 3536 primarily applies to LLCs in California, but understanding its implication across different business entity types is crucial for compliance. Each entity might have different state filing obligations, affecting the application and relevance of specific forms like the FTB 3536. Corporations and partnerships may have distinct filing requirements, emphasizing the importance of verifying eligibility and requirements for specific business structures operating in California.