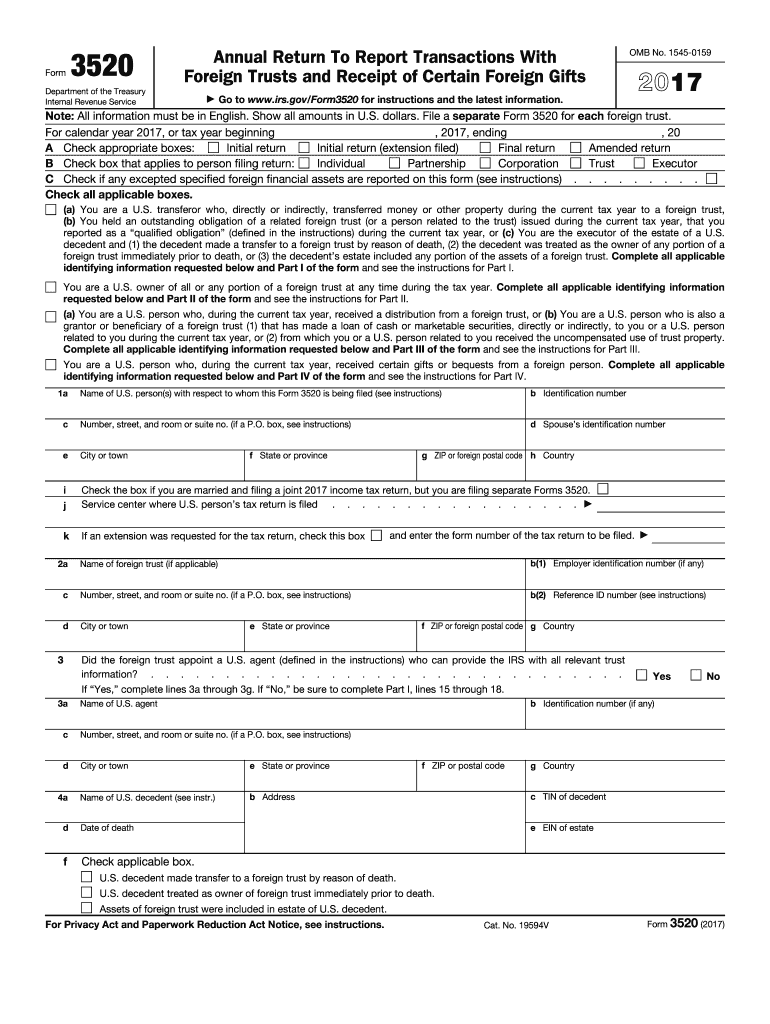

Definition and Purpose of Form 3520

Form 3520, officially titled the "Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts," serves as a reporting mechanism for U.S. persons who engage in transactions with foreign trusts or receive foreign gifts. The form aims to provide the Internal Revenue Service (IRS) with necessary information about these transactions to ensure compliance with U.S. tax laws. Specifically, it requires detailed reporting from individuals who have transferred money or property to foreign trusts, received distributions from such trusts, or obtained gifts from foreign entities or individuals.

Eligibility and Who Uses Form 3520

Form 3520 is relevant for individuals who engage in cross-border financial activities involving trusts or foreign gifts. U.S. persons, including citizens and certain non-citizens who reside in the U.S., must file this form if they are responsible for creating or transferring assets to a foreign trust, own equivalent financial interests, or receive gifts exceeding specific thresholds from foreign sources. While the form tailors to individuals, businesses such as LLCs or partnerships with relevant foreign interactions may also find it applicable in ensuring comprehensive reporting to the IRS.

Obtaining Form 3520 for Tax Year 2017

U.S. individuals can access Form 3520 for the 2017 tax year through the official IRS website, where a downloadable PDF version is available for those who prefer to fill out a physical copy. Additionally, tax preparation software such as TurboTax and QuickBooks may offer electronic versions integrated into their platforms, assisting users in aligning their forms with other tax filings. It's crucial to use the correct tax year version to avoid discrepancies during submission and review.

Key Elements of the Form

Form 3520 consists of several essential sections designed to capture detailed data about the filer’s financial activities with foreign entities. These include:

- Identifying Information: Personal details of the filer, including name, address, and Social Security Number.

- Information on Foreign Trusts: Details about the foreign trust, its activities, and trustee information.

- Transaction Summaries: Specific transactions with the foreign trust, including distributions and contributions.

- Foreign Gifts: Comprehensive reporting of gifts from foreign entities, detailing the nature and value of such gifts.

Step-by-Step Guide to Completing Form 3520

- Gather Required Information: Collect all relevant documents, such as trust agreements, bank statements, and gift details, required for accurate reporting.

- Complete the Identifying Information Section: Start with basic personal information, ensuring all details match IRS records.

- Report Foreign Trust Transactions: Fill out sections detailing contributions to and distributions from foreign trusts, providing transaction dates and amounts.

- Document Received Gifts: List all eligible foreign gifts, especially those exceeding IRS reporting thresholds.

- Sign and Date the Form: Ensure the form is accurately signed, which represents compliance and authenticity of provided information.

Important Terms Related to Form 3520

Understanding specific terms is crucial:

- Foreign Trust: A trust that has a U.S. trustee and is overseen by non-U.S. individuals or entities.

- U.S. Person: Refers to U.S. citizens, residents, and certain foreign individuals engaging in U.S. tax liable activities.

- Distribution: Any conveyance of money or property from a trust to a beneficiary.

- Foreign Gift: Transfer of money or property received from non-U.S. donors.

Filing Deadlines and Important Dates

Form 3520 must be filed alongside the U.S. individual’s tax return by the April filing deadline, typically April 15, unless an extension is granted. If extended, the form is due on October 15. Missing these deadlines can result in penalties categorized under non-compliance.

Penalties for Non-Compliance

Failure to file Form 3520 accurately and timely may lead to significant penalties, including:

- Monetary Penalties: A minimum penalty starting at $10,000 may be imposed for each unfiled form.

- Percentage-Based Penalties: Penalties can increase based on percentages of the unreported amounts tied to foreign trusts or gifts.

Legal and Secure Submission Methods

Submitters can send completed Form 3520 via mail to the IRS service center designated for their state. Digital submissions are recommended through authorized channels that comply with IRS protocols, ensuring minimal errors and secure data handling.