Definition and Purpose of Schedule M (Form 990)

Schedule M (Form 990) is an informational form used by tax-exempt organizations in the United States to report noncash contributions. It serves to provide the IRS with details regarding the types and values of noncash donations received and is a critical component for transparency in nonprofit operations. Organizations that file Form 990 and receive substantial noncash contributions are required to complete this schedule, illustrating the nature and valuation process of these contributions. Understanding its purpose helps ensure compliance and accurate reporting for tax-exempt entities.

How to Obtain Schedule M (Form 990)

Accessing the Schedule M (Form 990) can be done through several avenues. Organizations can directly download the form from the official IRS website, which offers the most updated version. Additionally, tax software solutions often include Schedule M as part of their tax filing packages, facilitating its completion alongside other necessary forms. Local IRS offices can also provide physical copies upon request, though this method may require additional time for mailing or in-person pickup. Ensuring access to the form is the first step in complying with tax reporting obligations.

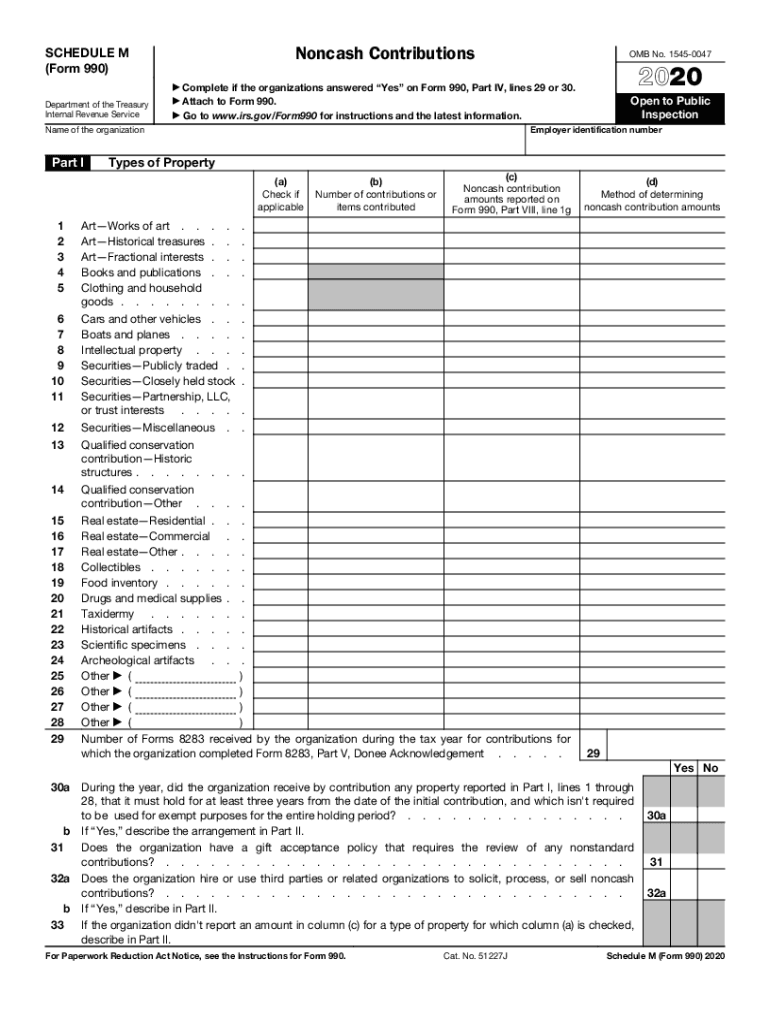

Key Elements of Schedule M (Form 990)

The form comprehensively captures various elements of noncash donations. Organizations are required to categorize contributions based on types of property, such as securities, inventory, or intellectual property. Specific details like fair market value, the method used for valuation, and any related conditions or restrictions on use must be specified. Additionally, organizations need to disclose policies regarding the acceptance and handling of noncash contributions, which adds an extra layer of accountability and clarity for both the IRS and potential donors.

Steps to Complete Schedule M (Form 990)

Completing Schedule M involves several steps, beginning with gathering information on all noncash donations. Organizations must:

- Identify each type of noncash contribution received throughout the year.

- Determine the fair market value of each contribution, using appropriate valuation methods.

- Categorize contributions according to IRS-defined property types.

- Fill out the relevant sections detailing the quantity and types of property, along with their valuations.

- Provide explanations for significant valuation methods and any policies on accepting noncash contributions.

This structured approach ensures accurate and compliant reporting.

Who Typically Uses Schedule M (Form 990)

Schedule M is primarily used by tax-exempt organizations that regularly receive noncash contributions exceeding $25,000 during the fiscal year. This includes charities, educational institutions, cultural organizations, and certain private foundations. The requirement to file is contingent on the nature and volume of noncash contributions, focusing specifically on those entities that leverage in-kind assets as a significant part of their operational funding.

Important Terms Related to Schedule M (Form 990)

To fully understand Schedule M, several key terms need clarification:

- Noncash Contributions: Donations made in forms other than monetary, such as property or goods.

- Fair Market Value: The estimated market price at which property would change hands between a willing buyer and seller.

- Valuation Methods: Techniques used to determine the worth of noncash contributions, including appraisals and comparable sales.

Familiarity with these terms is crucial for accurately completing the form.

IRS Guidelines and Compliance for Schedule M

The IRS provides comprehensive guidelines to assist organizations in completing Schedule M. These directives outline acceptable valuation techniques and detail the documentation required to substantiate reported values. Additionally, guidelines specify record-keeping standards to ensure transparency and facilitate auditing processes. Organizations must adhere to these standards to avoid penalties or potential issues with tax compliance.

Filing Deadlines and Important Dates for Schedule M

Schedule M must be submitted as an attachment to Form 990, adhering to the corresponding filing schedules. Generally, Form 990 is due five and a half months after the end of the organization's fiscal year. Extensions are available upon request, providing a six-month extension period if needed. Organizations must keep track of these deadlines to ensure timely compliance and avoid late filing penalties.

Penalties for Non-Compliance with Schedule M

Failure to properly complete or file Schedule M can result in penalties from the IRS. These may include fines per incomplete or inaccurate return. Continued negligence can lead to an organization's tax-exempt status being jeopardized. Maintaining accurate records and ensuring the integrity of reported information are critical to avoiding such consequences.

Digital vs. Paper Version of Schedule M

Organizations can choose between filing Schedule M electronically or as a paper submission. Digital submission via IRS-approved e-file providers is generally encouraged for its efficiency and reduced processing time. However, some organizations may opt for paper filing due to preference or resource constraints. Each method has its protocol, but the accuracy and completeness of information remain paramount in either format.