Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send nyc tda withdrawal application via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out ny tda withdrawal with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the ny tda withdrawal document in the editor.

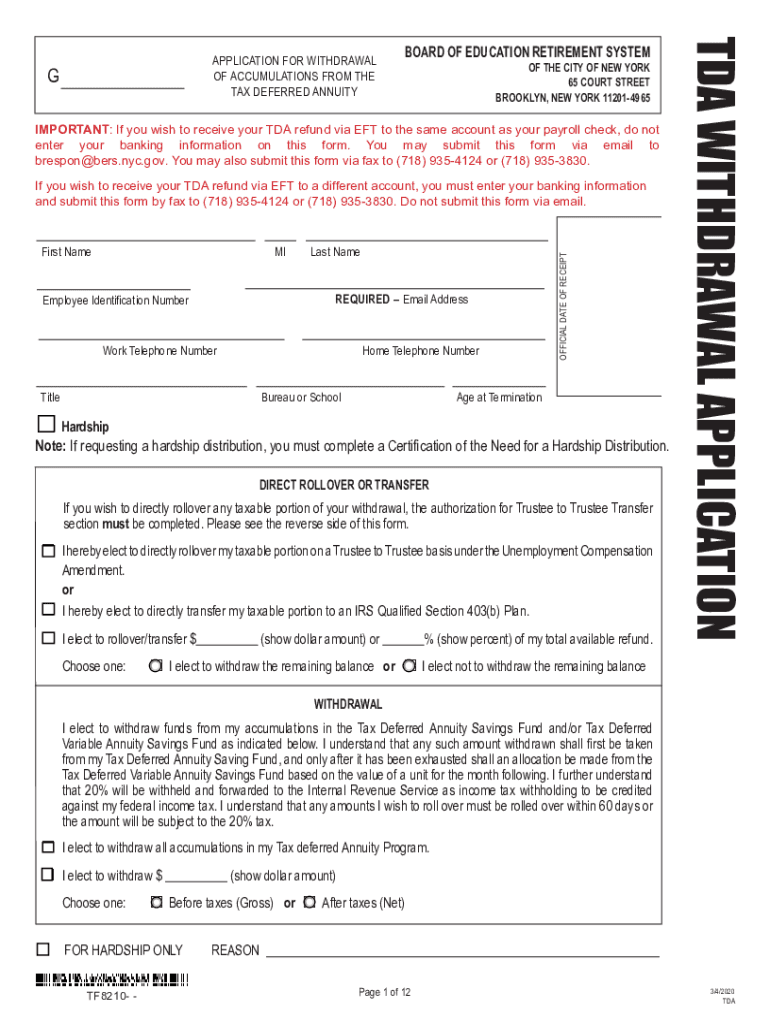

Begin by filling in your personal information, including your First Name, MI, Last Name, Email Address, Employee Identification Number, and Work Telephone Number. Ensure all required fields are completed.

Indicate your choice for receiving the TDA refund. If you want it via EFT to the same account as your payroll check, check 'YES' and skip entering banking information. Otherwise, provide your banking details.

If applicable, complete the Hardship section by checking the appropriate boxes and providing necessary documentation as outlined in the form.

For direct rollover or transfer options, select your preference and specify the amount you wish to roll over or withdraw. Make sure to understand tax implications as detailed in the form.

Review all entered information for accuracy before signing and dating the application at the bottom of the form.

Start using our platform today for free to streamline your ny tda withdrawal process!

Feb 14, 2025 If you elect to defer your TDA accounts, you may withdraw all or part of your TDA funds by filling an Application for. Tax-Deferred AnnuityRead more

Teachers Retirement System of the City of New York

Any amount withheld from a TDA withdrawal may be claimed as tax paid for the year of distribution. Withdrawing Funds from Your. TDA Account. Since the TDARead more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.