Related links

2017 General Instructions for Forms W-2 and W-3

May 2, 2017 Employer X also must complete Form 1099-MISC as follows. Boxes for recipients name, address, and TINthe estates name, address, and TIN.Read more

Learn more

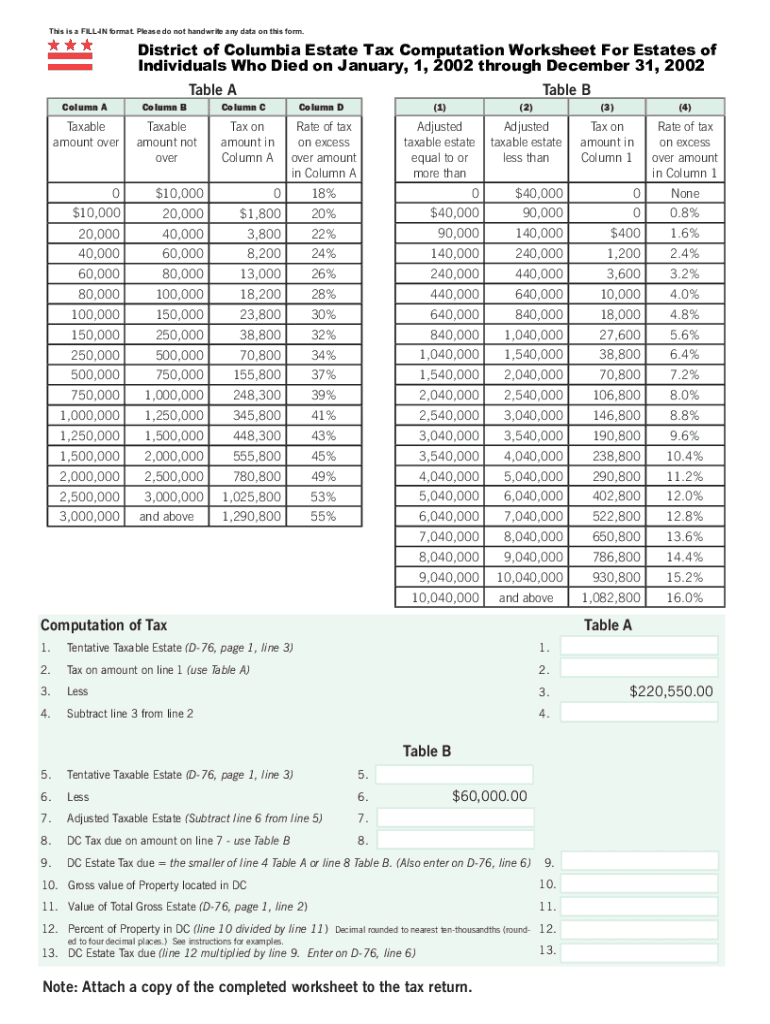

DC Inheritance and Estate Tax Forms | otr

The DC Estate Tax Return (D-76, D-76 EZ, D-77) must be filed and paid electronically via MyTax.DC.gov)

Learn more

Instructions for Form 706 - (Revised July 1999)

File Form 706 for the estates of decedents who were either U.S. citizens or U.S. residents at the time of death. For estate tax purposes, a resident is someoneRead more

Learn more