Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

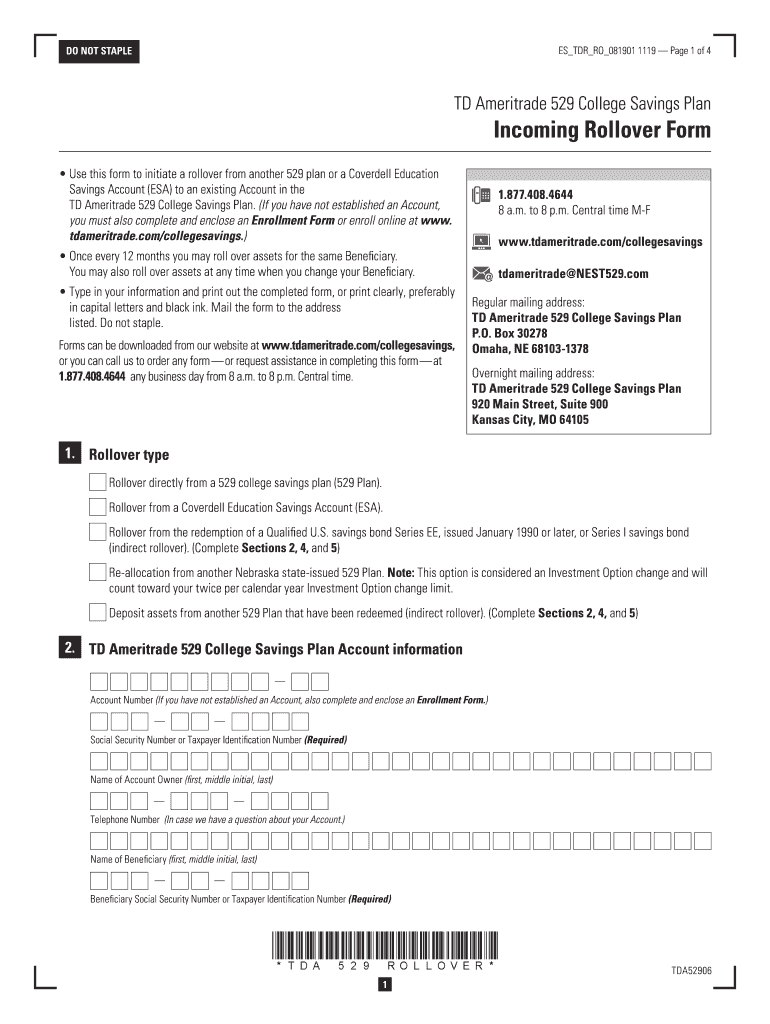

How to use or fill out 529 College Savings Plan Incoming Rollover Form - TD

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open it in the editor.

Begin by selecting the type of rollover you are initiating. Choose from options such as a direct rollover from another 529 plan or a Coverdell ESA.

Fill in your TD Ameritrade 529 College Savings Plan account information, including your account number and Social Security Number. Ensure that all details are accurate.

Provide the current 529 plan or ESA custodian's information if applicable. This is crucial for direct rollovers.

If assets have been redeemed, include the total amount of redemption and specify the principal and earnings amounts.

Sign and date the form at the bottom to certify your understanding of the terms and conditions.

Start using our platform today to complete your form online for free!

Fill out 529 College Savings Plan Incoming Rollover Form - TD online It's free

See more 529 College Savings Plan Incoming Rollover Form - TD versions

We've got more versions of the 529 College Savings Plan Incoming Rollover Form - TD form. Select the right 529 College Savings Plan Incoming Rollover Form - TD version from the list and start editing it straight away!

The QBI deduction was reported on Schedule 1 last year. Also see the new Form 8995 and Form 8995-A required to be attached to the 2019 return when claiming theRead more

Rollover your old retirement plan. If you have pre-tax retirement savings in another employers plan or in an individual retirement account (IRA), you canRead more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.