Definition & Meaning

Schedule F (Form 990) is a form required by the Internal Revenue Service (IRS) in the United States for nonprofit organizations that engage in foreign activities. Specifically, the 2016 version of this form is used to report such activities for that tax year. The primary purpose of Schedule F is to increase transparency and accountability for organizations operating outside the U.S. It captures crucial data on activities, including grants, assistance provided to foreign groups, individuals abroad, and foreign financial interests. By understanding and correctly filling Schedule F, organizations ensure compliance with federal regulations, illustrating their commitment to lawful and transparent operations.

How to Use the Schedule F 2016

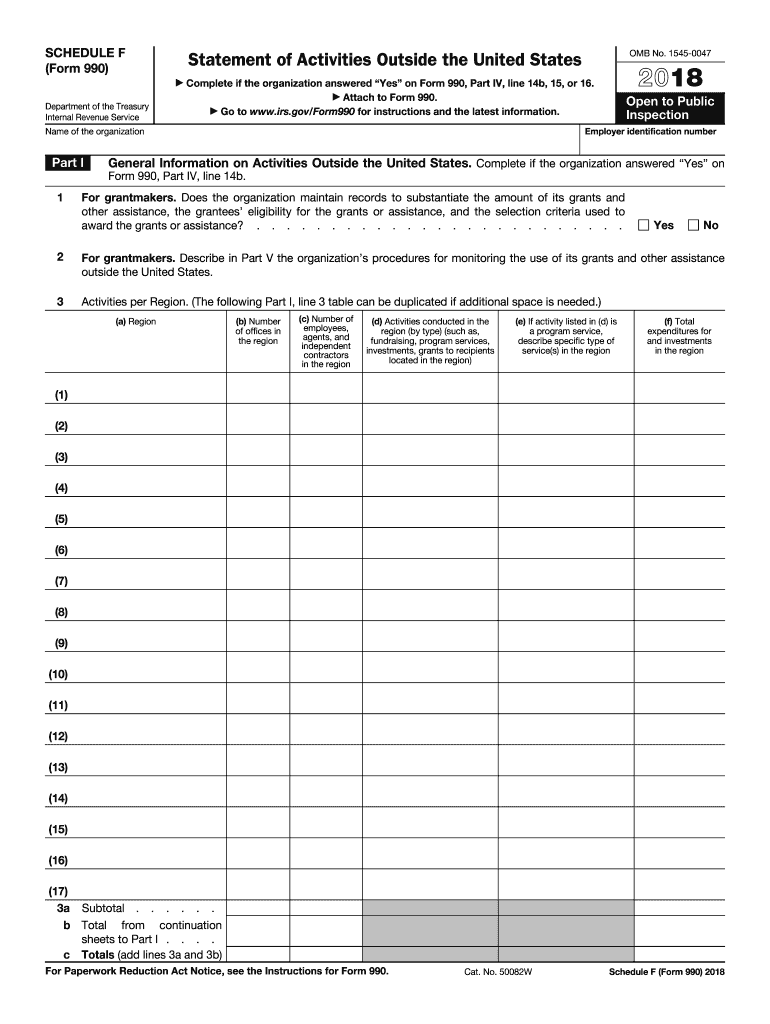

Utilizing Schedule F 2016 involves detailing overseas operations of a nonprofit organization. Organizations must list all foreign activities, breaking them down into regions and describing the nature of the work. For example, if a nonprofit provides educational grants in Africa, it must specify the countries involved, the grants’ objectives, and the amount disbursed. Furthermore, organizations should report any service, assistance, or financial holdings maintained outside the U.S., as well as detail any collaborative efforts with foreign entities. The information gathered aids in tracking financial flows and assessing engagement levels across global regions, necessary for compliance.

Steps to Complete the Schedule F 2016

- Gather Necessary Information: Organize data regarding all foreign activities, including grants, investments, and projects conducted outside the U.S.

- Identify Regions: Categorize activities by region and provide comprehensive descriptions of operations in each area.

- Detail Grants and Assistance: Record each grant or assistance program, noting purpose, amount, and recipient.

- Financial Activities: Include any foreign bank accounts or investments and their respective balances or values.

- Collaborative Efforts: Detail any partnerships or joint ventures with foreign organizations.

- Review for Accuracy: Double-check all entries for correctness to ensure compliance with IRS guidelines.

- Submit with Form 990: Attach the completed Schedule F 2016 form to the organization's annual Form 990 filing with the IRS.

Key Elements of the Schedule F 2016

- Part I: General Information on Activities Outside the U.S.: Requires disclosure of the types of activities conducted and a breakdown by regions.

- Part II: Grants and Other Assistance: Must include a detailed account of all assistance provided to foreign organizations or individuals.

- Part III: Foreign Operations and Investments: Covers detailed information about the organization's operations and financial activities in foreign markets.

- Reporting Thresholds: Instructions on thresholds that trigger the requirement for detailed reporting.

- Nonprofit Specific Details: Information reflecting the nature and scope of each activity concerning the nonprofit’s mission.

Who Typically Uses the Schedule F 2016

Nonprofit organizations, particularly those with international operations, are the primary users of Schedule F 2016. This includes educational nonprofits offering scholarships overseas, humanitarian groups providing foreign aid, or organizations conducting research in partnership with foreign institutions. Primarily, any tax-exempt organization subject to the Form 990 requirement and engaged with international activities must utilize Schedule F to report such undertakings.

IRS Guidelines

The IRS provides clear guidelines on completing Schedule F. Nonprofits must report their foreign activities with specificity, detailing countries involved, type of work performed, and financial contributions made. Organizations are instructed to ensure accuracy and completeness to meet compliance requirements. The form mandates listing individual grants exceeding specific monetary thresholds, capturing the breadth and depth of overseas engagements.

Penalties for Non-Compliance

Non-compliance with Schedule F reporting requirements can lead to significant penalties. Organizations may face monetary fines, revocation of tax-exempt status, or increased scrutiny by the IRS. Persistent failure to comply can also harm the organization's reputation, affecting donor trust and support. Hence, accurate and timely submission of Schedule F within the required Form 990 filing is crucial for maintaining regulatory and public confidence.

Filing Deadlines / Important Dates

Typically, Schedule F, as part of Form 990, is due by the 15th day of the 5th month after the end of the organization’s accounting period—usually May 15th for those following the calendar year. Nonprofits can apply for a six-month extension if necessary. It is vital to adhere to these timelines to avoid late filing penalties, safeguard tax-exempt status, and uphold organizational integrity.