Definition & Meaning

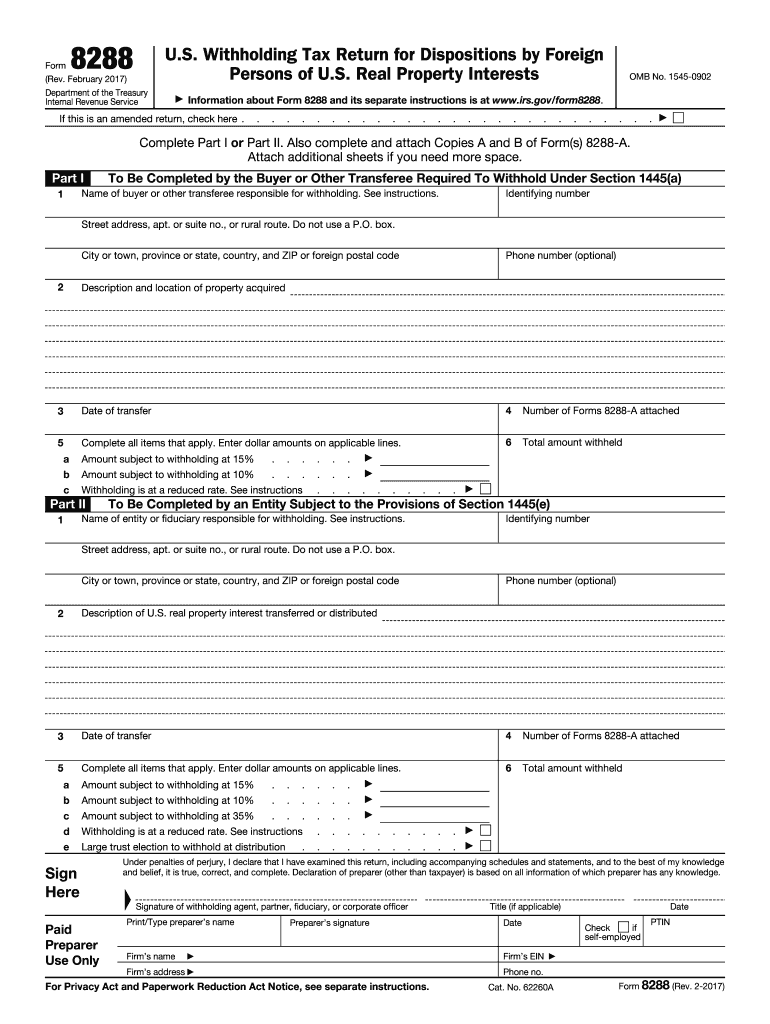

Form 8288, also known as the "U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests," is a critical IRS document used by buyers or transferees of U.S. real property from foreign sellers. Its purpose is to ensure compliance with the Foreign Investment in Real Property Tax Act (FIRPTA) under Section 1445 of the Internal Revenue Code. This form facilitates reporting and remittance of the necessary withholding tax to the IRS when a foreign person disposes of a U.S. real property interest.

How to Use the Form 8288

Using Form 8288 begins with accurately identifying the transaction's participants and providing all required information about the property involved. The form requires specifics about the buyer and seller, including their names, addresses, and relevant taxpayer identification numbers. Additionally, detailed information on the property, such as address, description, and the type of interest being transferred, must be accurately filled in. Compiling all necessary financial data, including withholding amounts, is essential to ensure correct submission and compliance.

Steps to Complete the Form 8288

-

Gather Necessary Information: Collect detailed information about the buyer, seller, and the property transaction.

-

Fill Out Identification Sections: Complete sections related to the identities of the buyer and seller, including names, addresses, and taxpayer identification numbers.

-

Provide Transaction Details: Enter precise information concerning the property, such as the property's description, transfer date, and sale amount.

-

Calculate Withholding Amount: Determine the withholding amount based on the applicable rate outlined in Section 1445.

-

Submit Payment with Form: Include the calculated withholding tax payment in U.S. dollars using an acceptable form of payment as instructed by the IRS.

-

File Timely: Ensure the form and payment are sent to the IRS by the deadline, typically 20 days from the date of transfer.

Filing Deadlines / Important Dates

Timeliness is crucial when it comes to Form 8288. The submission deadline is typically 20 days following the date of the property transfer. Missing this deadline may result in penalties and interest charges. It is also essential to be aware of any variations in deadlines caused by public holidays or IRS procedural changes to avoid complications.

Required Documents

When preparing Form 8288, certain documents are imperative to facilitate a smooth filing process. The principal document needed is the sales contract or agreement, which verifies the details of the real property transaction. Additional supporting documentation may include identification numbers for both parties and any exemption certificates that could affect the withholding amount.

Important Terms Related to Form 8288

Familiarity with key terms associated with Form 8288 is vital for accurate completion:

- Foreign Person: Any individual or entity not classified as a U.S. taxpayer under IRS definitions.

- U.S. Real Property Interest: Refers to stakes in real estate, land, or associated improvements located within the United States.

- Withholding Agent: Typically the buyer responsible for deducting and remitting withholding tax to the IRS.

Penalties for Non-Compliance

Failure to comply with Form 8288 requirements can lead to significant penalties. These can include monetary fines and interest accruing on unpaid amounts. Neglecting the obligation to withhold or accurately remit the appropriate taxes can also result in legal challenges or increased scrutiny from regulatory agencies.

IRS Guidelines

The IRS provides definitive guidelines on completing and filing Form 8288. These guidelines address eligibility criteria, form instructions, and compliance measures vital for taxpayers involved in transactions with foreign sellers. Adhering strictly to these guidelines ensures compliance and avoids unnecessary penalties or revisions and audits.

Who Typically Uses the Form 8288

The primary users of Form 8288 are purchasers of U.S. real property from non-U.S. sellers. This includes:

- Individuals and entities acquiring property interests from foreign sellers.

- Business entities or corporations engaged in cross-border real estate transactions.

- Title and escrow companies facilitating the completion of real estate transactions involving foreign persons.

By comprehending these components, stakeholders involved in transactions necessitating Form 8288 can ensure compliance and streamline their tax reporting process.