Definition and Meaning of Form 6765

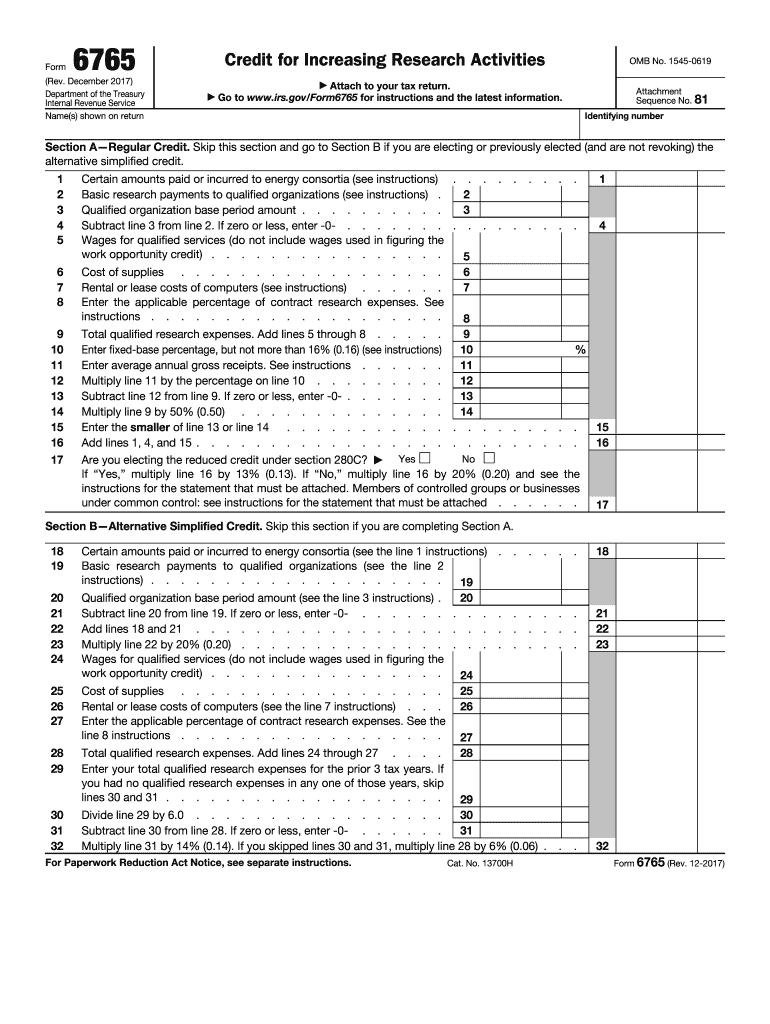

Form 6765, officially known as the "Credit for Increasing Research Activities," is a tax form used by businesses in the United States to claim tax credits for eligible research and development (R&D) expenses. This incentive is designed to encourage businesses to invest in research and innovation. The form allows companies to calculate their allowable credit by providing detailed sections for Regular and Alternative Simplified Credits based on qualifying expenses.

Key Components

- Regular Credit: Calculated using complex criteria that require detailed tracking of R&D expenditures across base and current years.

- Alternative Simplified Credit (ASC): Offers a more straightforward calculation method without requiring historical expense data.

- Eligible Expenses: Includes wages, supplies, contract research costs, and other relevant expenses directly linked to research activities.

How to Obtain Form 6765 for 2017

Obtaining Form 6765 is a straightforward process. For the 2017 tax year, businesses can access the form through several channels:

- IRS Website: The most reliable source is the IRS website, where downloadable PDF versions are available.

- Tax Preparation Software: Platforms like TurboTax and QuickBooks often include access to relevant tax forms, including Form 6765.

- Tax Professionals: Certified public accountants or tax preparers may provide copies of required forms for their clients.

Additional Sources

- Print Copies: Businesses can request paper copies directly from the IRS, though this may take more time compared to digital downloads.

- Library Resources: Some public libraries maintain tax form repositories, especially during the tax season.

Steps to Complete Form 6765 for 2017

Completing Form 6765 involves a structured approach to accurately report eligible R&D expenses and calculate the credit. Follow these steps:

- Compile Financial Records: Gather all documents related to R&D expenditures, including wages, supplies, and vendor contracts.

- Choose a Credit Calculation: Decide between the Regular Credit or ASC based on available data and computation ease.

- Complete Sections I and II: Focus on gathering data consistent with each section’s requirements, ensuring all figures are accurate.

- Calculate Base Amounts: For the Regular Credit, determine historical R&D expenses to establish a base amount.

- Finalize the Credit Calculations: Use the information gathered to compute the total eligible credit.

- Review and Sign: Double-check the completed form for accuracy before signing and submitting.

Example Calculations

- Regular Credit Example: Demonstrates using past expenditure data, calculating base years and incremental increases.

- ASC Example: Shows calculations applying a fixed percentage to current-year expenses without a detailed base period.

Who Typically Uses Form 6765 in 2017

Form 6765 is mainly used by businesses engaged in qualifying research activities, ranging from small startups to large corporations. Specific industries that commonly utilize the form include:

- Technology Firms: Continuous investment in innovative software and product development.

- Manufacturing Companies: Engagement in process improvements and development of new materials.

- Pharmaceuticals: Extensive R&D efforts in drug development and testing.

User Categories

- Small Businesses: Often benefit from tax savings through minor R&D investments.

- Corporations: Utilize substantial R&D budgets and engage in large-scale projects.

- Consulting Firms: Claim credits on behalf of clients engaged in eligible research activities.

Important Terms Related to Form 6765

Understanding key terms is crucial when dealing with Form 6765:

- Qualified Research Expenses (QREs): Any cost directly related to eligible research activities.

- Base Amount: Historical R&D expenses used to benchmark current credit eligibility.

- Incremental Research Credit: The difference between current-year expenses and a defined base period spending.

Detailed Explanations

- QREs: Include a breakdown of wages, materials, and R&D service contracts.

- Base Period Calculation: Explains different base periods for new vs. established companies.

- Credit Calculation Methods: Provides detailed comparisons between Regular Credit and ASC.

Legal Use of Form 6765

Legal compliance is essential when filing Form 6765 to avoid penalties or disallowance of claimed credits. Guidelines include:

- Accurate Reporting: Ensure all eligible expenses are backed by proper documentation.

- Compliance with IRS Regulations: Follow IRS stipulations regarding qualifying expenses and calculation methods.

- Audit Preparation: Maintain comprehensive records to justify all claimed credits in case of an IRS audit.

Compliance Tips

- Detailed Documentation: Keep thorough records of all research projects and associated costs.

- Regular Updates: Stay informed of any regulatory changes that could affect credit calculations for future filings.

Filing Deadlines and Important Dates for 2017

Adhering to deadlines is critical to ensure eligibility for claiming credits via Form 6765:

- Standard Filing Deadline: Aligns with corporate tax return deadlines, usually March 15 for corporations.

- Extensions: If a tax extension is filed, the form should be submitted by the extended deadline, typically six months later.

- Amended Returns: Businesses can file amended returns within three years of the original submission to correct any errors.

Strategic Considerations

- Planning: Ensure all necessary paperwork is ready before filing deadlines.

- Consultation: Engage tax professionals early to avoid last-minute inaccuracies or omissions.

Eligibility Criteria for Form 6765

Determining eligibility is the first step towards claiming the research tax credit:

- Qualified Research Activities: Must involve technological or scientific experimentation intended to create new or improved business components.

- Direct Nexus to Business: Activities should be pertinent to new product development or significant functional advancements.

- Economic Risk: The company should bear the risk of R&D execution, not relying on third-party outcomes.

Specific Guidelines

- Technological Uncertainty: Projects must involve resolving unknowns related to product design or methodology.

- Process of Experimentation: Activities should utilize tried-and-tested scientific methods for problem-solving.

By adhering to the above guidelines, businesses can fully maximize the benefits offered by Form 6765 while maintaining compliance and accuracy throughout the filing process.