Definition and Meaning of Form 6

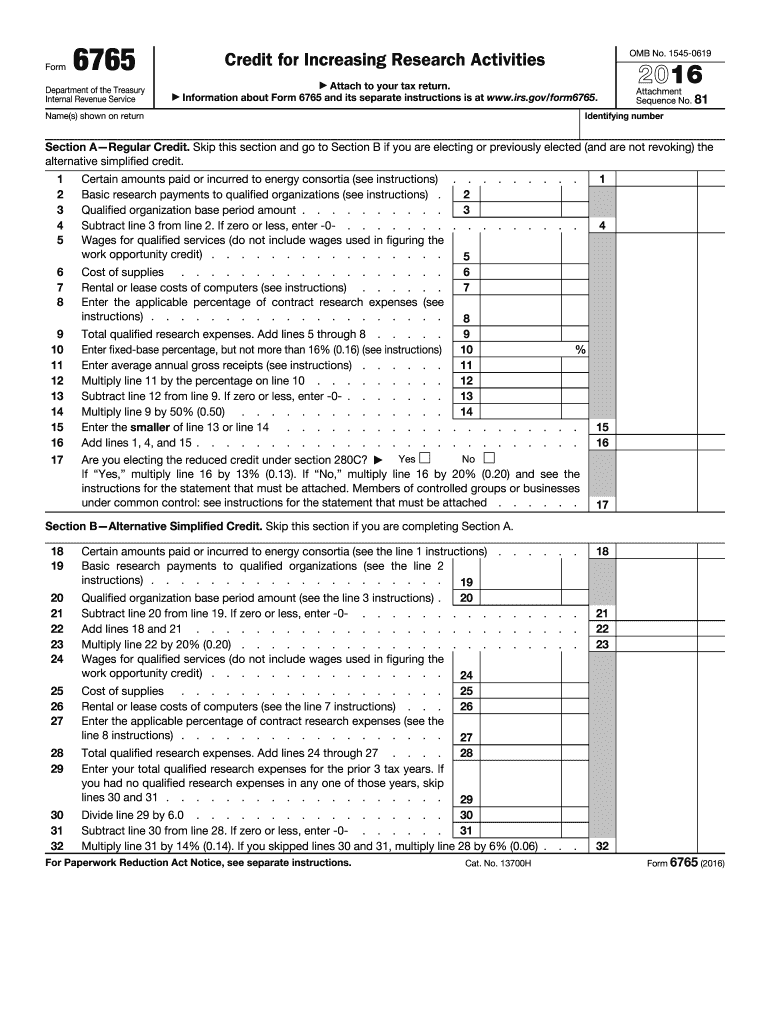

Form 6765 is a tax form used by businesses in the United States to claim the Credit for Increasing Research Activities. This form applies to both the Regular Credit and the Alternative Simplified Credit, which incentivize companies to invest in research and development (R&D) by providing a tax credit. For the 2016 tax year, this form captures important information about the business's qualified research expenditures, which must align with IRS definitions to meet eligibility.

Qualified Research Expenditures

When filling out the form, it's crucial to understand what counts as "qualified research expenditures." These expenses typically include wages for employees directly involved in R&D activities, costs of supplies used in the research, and payments to third-party contractors conducting research on behalf of the company.

Importance of the Credit

The credit provided by Form 6765 can significantly reduce a business's taxable income, promoting greater investment in innovative activities. This tax credit encourages economic growth by supporting advancements in technology and scientific research.

How to Use Form 6

Completing Form 6765 involves several steps that align with reporting the company's research activities and expenses accurately.

-

Calculate the Credit: Determine the total qualified research expenses and decide whether to use the Regular Credit method or the Alternative Simplified Credit (ASC) method. Each method requires different calculations and documentation.

-

Record Keeping: Maintain detailed records of all research activities, including supporting documentation for claimed expenses. This is vital for compliance and to substantiate claims in case of an IRS audit.

-

Attach to Tax Return: Once completed, Form 6765 must be attached to the business's tax return. Carefully review all sections for accuracy to avoid costly errors or delays in processing.

Choosing the Right Calculation Method

The choice between Regular Credit and ASC often depends on the availability of historical data and the complexity of calculations. Businesses with substantial R&D activities but less historical data may benefit from using the ASC method.

Steps to Complete Form 6

Completing the form involves several precise steps to ensure accuracy and compliance.

Step 1: Gather Information

- Employee Wages: Document wages paid to employees engaged in R&D.

- Supply Costs: Record costs of materials used directly in the research process.

- Contract Research Costs: Include up to 65% of payments to third-party entities conducting research.

Step 2: Perform Calculations

- Regular Credit: Uses a fixed base percentage and requires historical data on R&D spending.

- Alternative Simplified Credit (ASC): Simplified calculation based on current-year expenses, useful when less historical data is available.

Step 3: Complete the Form

- Part I: Determine total qualified research expenses.

- Part II: Choose the calculation method and compute the credit accordingly.

- Part III: Provide any additional required information, including carryforward credits.

Key Elements of Form 6

The form is structured to systematically gather necessary information and ensure correct credit calculation.

Section Breakdown

- Identification Information: Business name, tax identification number.

- Calculation Sections: Separate parts for Regular Credit and ASC.

- Expense Documentation: Fields for detailed entry of wages, supplies, and contract research costs.

Additional Considerations

Taxpayers must ensure that all information entered is consistent with their tax return to avoid discrepancies that could trigger audits or compliance checks by the IRS.

Eligibility Criteria for Form 6

To qualify for the credit, businesses must engage in specific types of research and adequately document their expenses.

Basic Requirements

- Qualified Research Activity: The activity must be aimed at discovering technological information intended to be useful in developing new or improved business components.

- Process of Experimentation: It should include a methodology of experimentation to resolve scientific or technological uncertainties.

Ineligible Activities

Not all research activities qualify. For example, activities related to market research, social sciences, or funded by another entity are not eligible.

IRS Guidelines for Form 6

Following IRS guidelines is crucial to avoid errors in the form and ensure the tax credit is granted.

Compliance with Regulations

- Documentation Requirements: Keep exhaustive records of all R&D activities to substantiate claims.

- IRS Publications: Refer to specific IRS publication guides for detailed explanations related to R&D credits and associated forms.

Audit Preparedness

Having thorough and organized documentation aids businesses in defending their claims if audited by the IRS. Regular audits require precise substantiation of the activities and expenses reported.

Business Types That Benefit Most from Form 6

Certain types of businesses are better positioned to take advantage of this credit due to the nature of their operations.

Beneficial Business Entities

- Technology Firms: Companies developing new software or innovative technologies.

- Manufacturers: Those carrying out substantial research to develop new products or enhance existing ones.

- Biopharmaceutical Companies: Engaging in drug development and clinical trials.

Case Studies and Examples

There are many real-world instances where businesses have leveraged Form 6765 to advance their research objectives, enabling significant tax savings which were then reinvested into further innovation.

Filing Deadlines and Important Dates for Form 6

Meeting filing deadlines is essential to claiming the credit without penalties.

Key Deadlines

- Regular Filing Deadline: Usually aligns with the company’s standard tax filing deadline.

- Extension Options: Businesses can request extensions, but it's critical to understand accompanying requirements like possible interest on tax due amounts.

Impact of Late Filings

Missing the deadline can result in fines or forfeiture of the credit. It's vital for businesses to integrate this awareness with their financial planning practices, allowing enough lead time to gather and prepare all necessary documentation.