Definition and Purpose of the 2-Q 2017 Form

Form 1099-Q is used in the United States to report distributions from qualified education programs, specifically under Sections 529 and 530 of the Internal Revenue Code. These sections pertain to college savings plans and Coverdell ESAs. The form is crucial for taxpayers who receive money from these accounts, as it helps determine tax liabilities related to educational payments. Understanding the form’s purpose aids recipients in correctly reporting educational distributions on their tax returns and aligning with IRS guidelines.

How to Use the 2-Q 2017 Form

The 2015 version of Form 1099-Q for 2017 filings involves several use cases. Recipients must accurately report the total distributions received from their educational savings accounts. Here’s a step-by-step on how to utilize the form:

- Verify Information: Check personal information, like your Social Security Number, for accuracy.

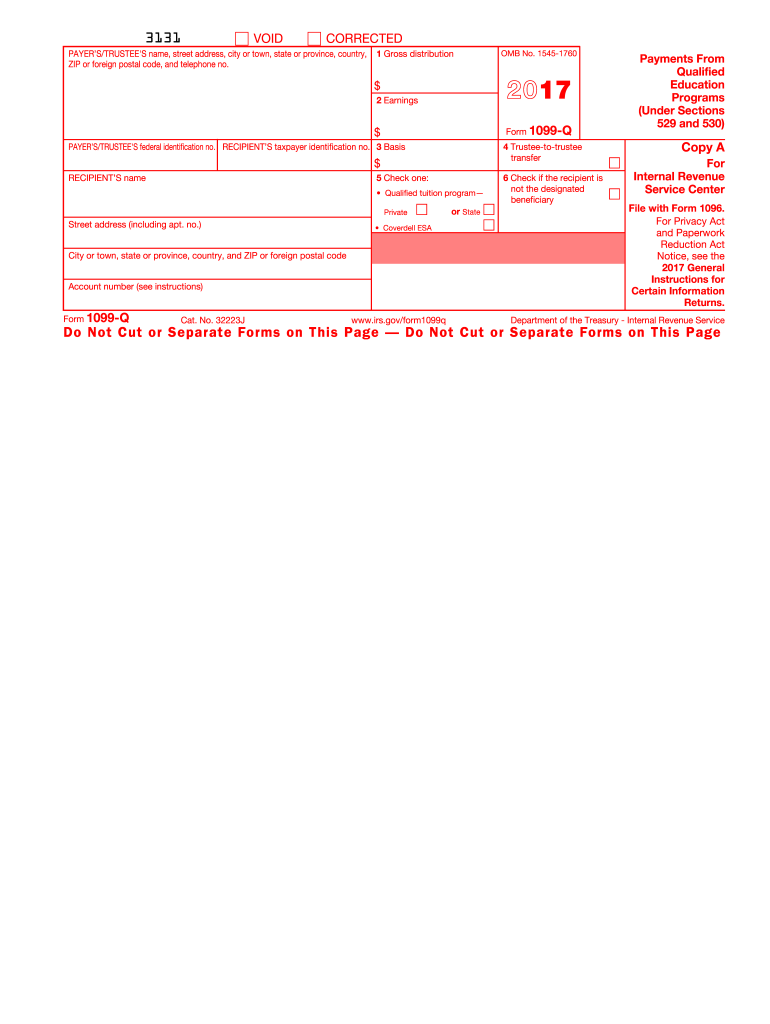

- Review Box 1: Total gross distributions from the account.

- Check Box 2: Earnings portion of the distribution.

- Assess Box 3: Basis, or contributions made to the account.

- Determine Taxability: Consult IRS Publication 970 to assess whether the earnings are taxable based on qualified educational expenses.

Obtaining the 2-Q 2017 Form

Generally, the financial institution or account trustee responsible for managing the 529 plan or Coverdell ESA issues Form 1099-Q. It is typically sent to taxpayers by January 31 following the tax year in question. If you do not receive the form, it is vital to contact the issuing institution. Alternatively, some institutions may offer online access to the form through their secure account portals.

Steps to Complete the 2-Q 2017 Form

While the form itself is completed by the issuer, taxpayers receiving Form 1099-Q should follow these steps:

- Receive and Review: After receiving the form, validate all information for accuracy.

- Consult Tax Information: Use the details in Boxes 1 through 3 to calculate any taxable portion of the distribution.

- Report on Tax Return: Include relevant figures on your federal tax return under lines designated for additional income and tax computation.

- Documentation: Retain all related documents such as account statements and receipts for educational expenses for audit purposes.

Key Elements of the 2-Q 2017 Form

The key elements included in Form 1099-Q are essential to accurately reporting and recording distributions:

- Box 1: Lists the total amounts distributed from the qualified accounts.

- Box 2: Shows the portion representing earnings, which may be subject to taxes.

- Box 3: Details the contribution basis, vital for calculating non-taxable amounts.

- Payer’s Details: Includes necessary contact information of the financial institution.

- Recipient Information: Ensures the form correctly identifies the taxpayer receiving the distribution.

Important Terms Related to the 2-Q 2017 Form

Understanding the terminology used in the form is critical:

- Qualified Educational Expenses: Expenses that may make the distribution tax-free if used accordingly.

- 529 Plans: State-run or state-affiliated institutions that provide tax advantages for college savings.

- Coverdell ESA: Savings accounts designated for education-related expenses.

- Distribution: Withdrawn amounts from a savings account.

IRS Guidelines and Compliance

IRS guidelines specify that Form 1099-Q should be used to report distributions that may have tax implications. Taxpayers must differentiate between qualified and non-qualified distributions. Qualified expenses can include tuition, books, and supplies. Non-compliance or incorrect reporting can lead to penalties. Taxpayers are advised to review IRS Publication 970 for comprehensive rules and examples.

Filing Deadlines and Important Dates

The Form 1099-Q must be issued by January 31 to recipients for distributions made in the previous calendar year. When filing personal taxes, taxpayers should incorporate information from this form into their returns by the April 15 tax filing deadline. Late submissions can incur penalties, so timely reporting is essential.