Definition & Purpose of Form 990 Schedule A

Form 990 Schedule A is a critical component of the IRS Form 990 series, designed specifically for organizations classified as 501(c)(3) public charities and certain nonexempt charitable trusts. It serves to outline the requirements for determining public charity status and to provide detailed information on public support. The form helps in assessing the compliance of an organization with IRS regulations to maintain its tax-exempt status. Key components of this form include the demonstration of public support received and an overall assessment of the organization's financial practices in line with IRS transparency requirements. By completing Schedule A, organizations can confirm they are meeting their public support tests and aligning with legal expectations.

Who Typically Uses Form 990 Schedule A

The primary users of Form 990 Schedule A are 501(c)(3) public charities and nonexempt charitable trusts. These entities include charitable, religious, educational, scientific, and literary organizations, along with some amateur sports organizations and groups focused on the prevention of cruelty to children or animals. Additionally, universities, hospitals, and other publicly supported entities must file this form to underscore their compliance with public support and operational standards. This form is essential for these organizations to maintain their favorable tax status by demonstrating adherence to public charity requirements.

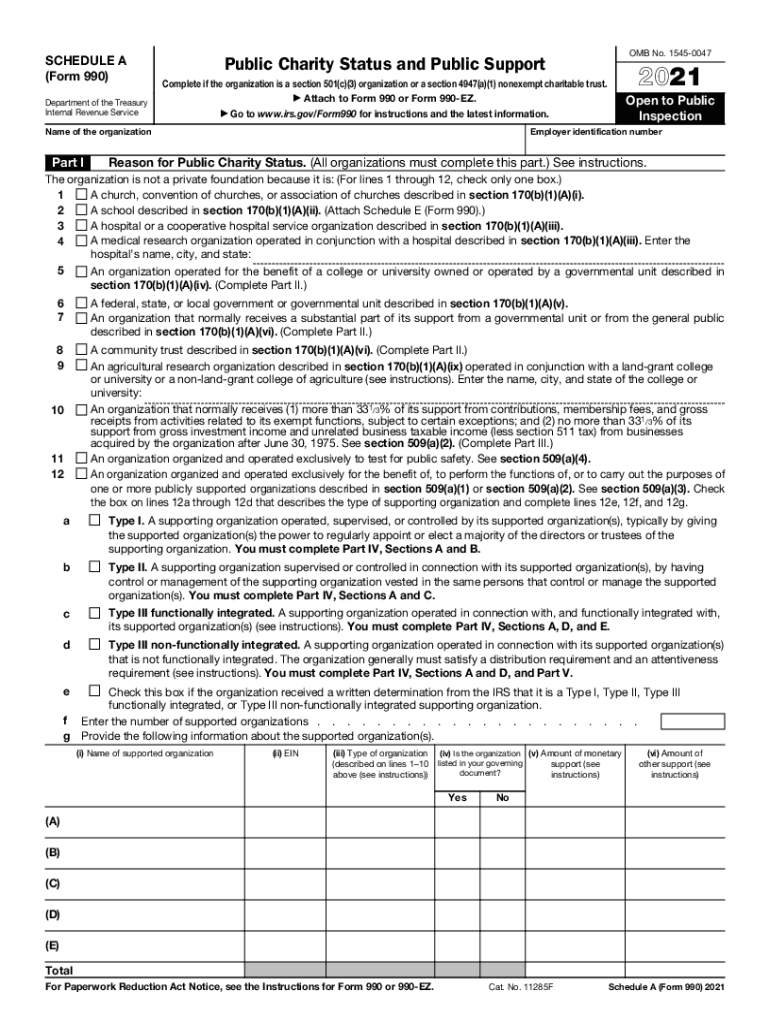

Key Elements of Form 990 Schedule A

Form 990 Schedule A is structured to collect extensive data on an organization's public support. The key elements include:

- Public Support Test: Organizations must calculate their public support percentage over a specific period, typically five years, to prove they are primarily supported by the public or the government.

- Support Schedule: A detailed account of the different types of public support received, such as donations from individuals, government grants, and other contributions.

- Compensation and Expense Disclosure: Information about compensation to board members, officers, and other key employees to ensure compliance with the limitations on private benefits.

- Supplementary Information: Potential additional data on lobbying activities, if applicable, which helps the IRS determine the adherence to necessary activities pertinent to tax-exempt operations.

Steps to Complete Form 990 Schedule A

- Gather Financial Data: Collect detailed financial records of all contributions, membership fees, and grants received over the applicable measurement period.

- Determine Public Support Percentage: Use the form’s worksheets to calculate the public support percentage, which helps in establishing the qualification as a public charity.

- Documentation of Miscellaneous Income: Record any unrelated business income and its purpose.

- Review Supplementary Schedules: Provide additional information as required in various schedules, including lobbying activities and compensation disclosures.

- Verify Compliance: Confirm that all figures and information align with the IRS's legal expectations and disclosure requirements.

- Submit: Ensure all parts are completed accurately before submission through the appropriate channels.

Important Terms Related to Form 990 Schedule A

Understanding various terms is crucial when completing Form 990 Schedule A:

- Public Charity: An entity primarily supported by public interests, including government or community contributions.

- Public Support Test: A criterion determining the extent of public support an organization receives relative to their total support.

- Nonexempt Charitable Trust: Trust organizations with charitable intents, which are not fully exempt from taxes.

- Qualifying Support: Contributions, grants, and other support from the general public or government entities that aid in passing the public support test.

Filing Deadlines & Important Dates

Organizations required to file Form 990 Schedule A must pay close attention to IRS deadlines. Typically, this schedule must be submitted in conjunction with Form 990 by the 15th day of the 5th month following the close of the entity's fiscal year. Extensions may be granted under certain conditions, but penalties can apply for late or incomplete submissions. Keeping track of these timelines is vital to avoid jeopardizing an organization's tax-exempt status.

Penalties for Non-Compliance

Failing to properly complete Form 990 Schedule A or missing submission deadlines may result in significant penalties. The IRS imposes financial penalties based on the size and nature of the organization, and prolonged non-compliance could result in revocation of tax-exempt status. It is essential for organizations to ensure their financial data and declarations are accurate and submitted on time to avoid these repercussions.

Examples and Practical Scenarios

To understand the utility of Form 990 Schedule A, consider the scenario of a community-based educational charity. This organization, seeking to maintain its public charity status, must demonstrate through Schedule A that a significant portion of its funding comes from governmental grants and public donations. Another example is a hospital using this form to illustrate compliance by tracking public and private funding streams, thereby cementing its tax-exempt status by evidencing public support over several years. These examples highlight the form's role in sustaining organizational legitimacy and protecting tax advantages.