Definition and Purpose of Form 941-PR

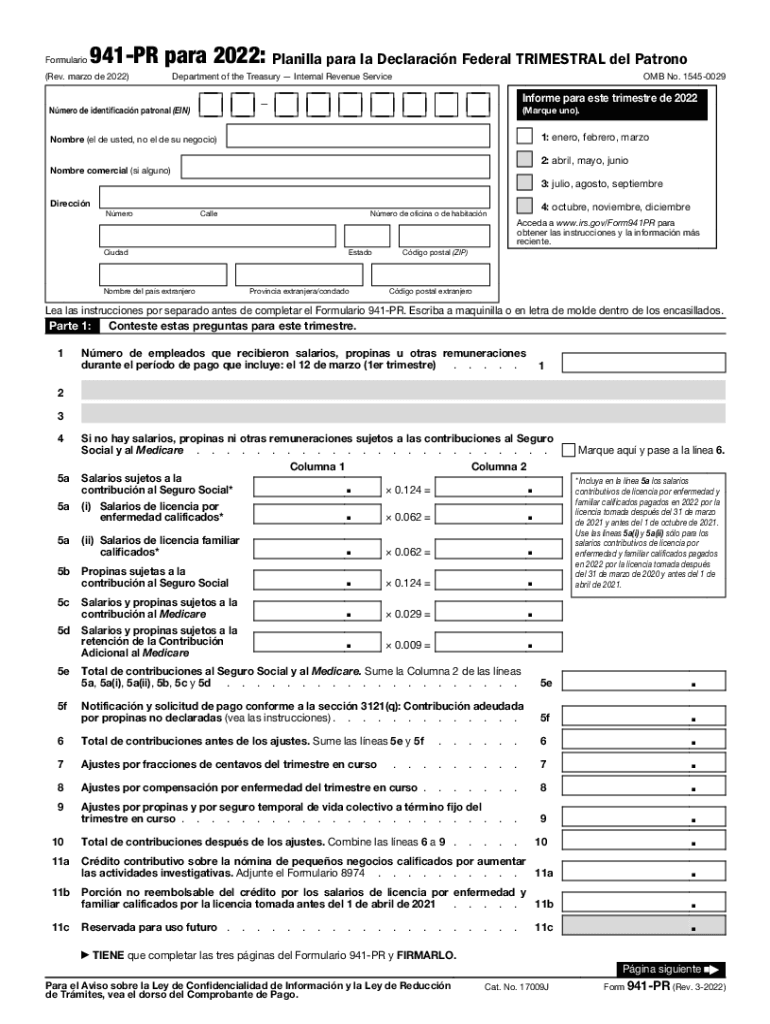

Form 941-PR, also known as the Employer’s Quarterly Tax Return for Puerto Rico, is used by employers in Puerto Rico to report federal taxes. These include contributions for Social Security and Medicare. This form helps the Internal Revenue Service (IRS) track payroll taxes specific to employers operating in Puerto Rico, ensuring accurate financial record-keeping and tax compliance.

Employers must detail wages paid, tips received, and other compensation, while calculating the employer's share of Social Security and Medicare taxes. Understanding the purpose of Form 941-PR encourages accurate submission and assists in avoiding penalties due to late or incorrect filings.

How to Obtain Form 941-PR

Employers can access Form 941-PR through the IRS website, where the PDF version of the form is available for download. It is crucial to use the correct version of the form corresponding to the reporting year. Printed copies can also be obtained by calling the IRS and requesting a mailed version.

Digital integration allows employers to utilize tax preparation software like TurboTax or QuickBooks, which often include the ability to generate and e-file this form. Accessing the form through official channels ensures its legitimacy and compliance with federal requirements.

Steps to Complete Form 941-PR

-

Accumulate Necessary Information: Gather all relevant payroll data, including total wages paid, taxes withheld, and employee information.

-

Calculate Payroll Taxes: Compute Social Security and Medicare taxes, ensuring accuracy by cross-referencing payroll records.

-

Complete Each Section: Follow form instructions closely. Include details like the employer identification number (EIN) and address.

-

Review and Verify: Double-check figures for accuracy and completeness to prevent common errors.

-

Submit: Choose between mailing the physical form or submitting it electronically through approved IRS e-file services.

Completing Form 941-PR demands attention to detail and verification against payroll data to ensure accuracy in reporting.

Filing Deadlines and Important Dates

Form 941-PR is a quarterly filing requirement. The due dates are typically:

- First Quarter (January - March): Due by April 30

- Second Quarter (April - June): Due by July 31

- Third Quarter (July - September): Due by October 31

- Fourth Quarter (October - December): Due by January 31 of the following year

Understanding these deadlines is crucial for timely submissions to avoid penalties. If the due date falls on a weekend or federal holiday, the IRS extends the deadline to the next business day.

Legal Use and Compliance of Form 941-PR

Form 941-PR adherence ensures compliance with federal tax laws specific to Puerto Rican employers. Employers calculate and report employee withholdings and employer contributions for Social Security and Medicare. Legal compliance protects companies from potential audits and fines.

The ESIGN Act supports the legal acceptance of electronic submissions for this form, providing flexibility in filing methods.

Key Elements of Form 941-PR

- Employer Identification Number (EIN): Ensures proper tracking of the employer's tax account.

- Total Wages and Compensation: A detailed report of all salaries disbursed.

- Taxes Reported: Include Social Security and Medicare contributions.

- Adjustments for Prior Quarters: Corrects any errors from previous filings, if necessary.

In-depth understanding of these elements fosters accurate and complete form submissions.

Who Typically Uses Form 941-PR

The primary users of Form 941-PR are employers operating within Puerto Rico who are responsible for federal tax obligations for Social Security and Medicare. This includes:

- Small and Medium Enterprises (SMEs): Regular filers due to employee payroll.

- Corporate Entities: Required to report larger payroll taxes.

- Non-profit Organizations: Must comply if employing staff in Puerto Rico.

Understanding user demographics aids accurate targeting of instructional resources.

IRS Guidelines and Instructions

The IRS provides comprehensive instructions for completing Form 941-PR, including:

- Filing Requirements: Criteria defining who must file.

- Payment Instructions: Methods for any taxes owed.

- Adjustment Entries: Guidelines for correcting previously submitted data.

Adhering to these guidelines ensures completeness and accuracy, reducing chance of error. Employers are encouraged to regularly consult IRS publications for any updates or changes to filing procedures.