Definition and Meaning

The 1098 form is primarily used for tax reporting purposes in the United States. It reports various types of payments made by individuals or entities, which may affect tax calculations. The most common variants include 1098-E for student loan interest, 1098-T for tuition payments, 1098-C for charitable contributions of property, and 1098-MORT for mortgage interest. Each variant serves to document specific transactions and inform taxpayers of potential deductions or credits, aiding them in preparing accurate tax returns.

How to Use the 1098 Form

To effectively use a 1098 form, recipients should understand the type of expenses it covers and how this information can be leveraged during tax filing. For example:

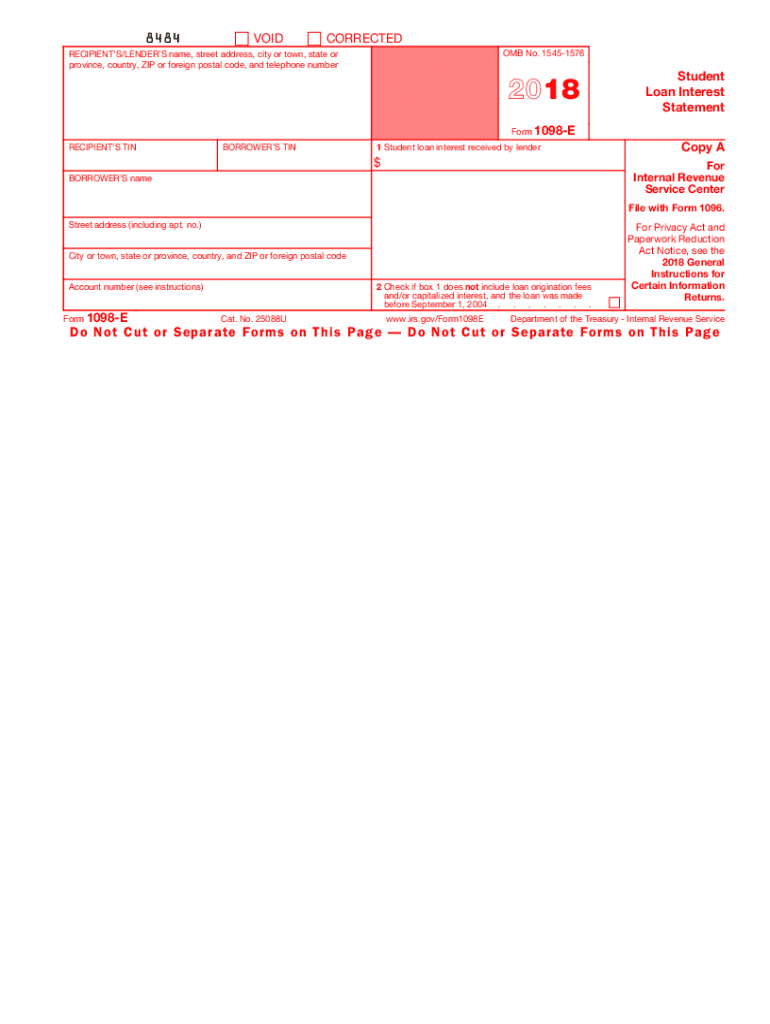

- 1098-E: Reports student loan interest. Taxpayers can use this to potentially deduct up to $2,500 of interest paid on qualified student loans.

- 1098-T: Details amounts billed for tuition and educational expenses, which may qualify for education tax credits.

- 1098-MORT: Provides information on mortgage interest paid, which can often be deducted if taxpayers itemize deductions.

Individuals should compare the information on these forms with their records to ensure accuracy. This verification prevents discrepancies during tax submission and assists in maximizing eligible deductions.

How to Obtain the 1098 Form

Typically, the institutions involved in the reported transactions issue the necessary 1098 form by January 31 each year. For example:

- 1098-E: Issued by student loan servicers.

- 1098-T: Issued by educational institutions.

- 1098-MORT: Issued by financial institutions or mortgage lenders.

Taxpayers can receive these forms through mail or digitally, depending on their preference and the issuer's policies. If the form isn't received by early February, individuals should contact the relevant institution to request a copy.

Steps to Complete the 1098 Form

The completion of the 1098 form typically involves detailing information given by the issuer, but for informational filing:

- Verify Personal Information: Ensure your name and taxpayer identification number are correct.

- Check Payment Details: Match the amounts reported with your personal records for consistency.

- Understand Deductions/ Credits: Identify which amounts could influence your tax return, like eligible interest or tuition payments.

For businesses or large entities issuing the form, precise record-keeping and adherence to IRS guidelines regarding reportable transactions and thresholds are crucial.

Key Elements of the 1098 Form

Every 1098 form includes specific fields and information unique to its purpose:

- Payer's Information: Includes the name, address, and EIN of the organization reporting the payments.

- Recipient's Information: Includes the taxpayer's name and identification number.

- Box Descriptions: Lines detailing amounts paid, such as interest amounts, tuition, or donations relevant to the specific form variant.

Each element provides the IRS and taxpayers with structured data to accurately assess applicable deductions or credits.

Who Issues the Form

The entity directly associated with the financial transaction is responsible for issuing the 1098 form:

- 1098-E: Issued by lenders or student loan servicers.

- 1098-T: Provided by accredited colleges or universities.

- 1098-MORT: Supplied by mortgage providers or financial institutions.

These entities are responsible for ensuring the forms are accurate and distributed to taxpayers and the IRS within the specified timeframes.

IRS Guidelines

The Internal Revenue Service sets out specific rules regarding the issuance, filing, and use of the 1098 forms. These guidelines specify thresholds for reported payments, deadlines for form distribution, and acceptable uses for tax deductions or credits. Taxpayers and issuers alike must adhere to these requirements to ensure compliance and avoid potential penalties or audits.

Filing Deadlines and Important Dates

Understanding the timeline associated with the 1098 forms is crucial:

- January 31: Deadline for issuers to provide the form to taxpayers.

- February 28: Deadline for paper filing of the form with the IRS.

- March 31: Deadline for electronic filing of the form with the IRS.

Failure to file or distribute forms by these dates may result in penalties for the issuing institution, and potential delays in taxpayer filings.

Penalties for Non-Compliance

Failure to accurately file or distribute the 1098 forms can result in severe penalties. For institutions that fail to meet IRS deadlines, fines can range based on the delay's duration and the number of forms involved. Taxpayers who inaccurately report or omit these forms when filing can face audits, fines, or denied deductions. Prompt and accurate compliance helps avoid these consequences and ensures that tax processes run smoothly.

Digital vs. Paper Version

Taxpayers and institutions can choose between digital and paper options for receiving or filing the 1098 forms. Digital versions are often preferred for their convenience and eco-friendliness, yet paper forms remain a staple for those less comfortable with technology. Regardless of the format, both forms hold the same validity and should be securely stored for future tax-related purposes or audits.

Examples of Using the 1098 Form

Individual scenarios illuminate the form's practical application:

- A taxpayer receiving a 1098-E form deducts eligible student loan interest from their taxable income, reducing their tax liability.

- A college student with a 1098-T claims the American Opportunity Tax Credit, reducing their owed taxes up to $2,500.

- A homeowner uses the 1098-MORT to deduct mortgage interest, increasing their itemized deductions.

These examples highlight the form's value in providing accurate tax benefits.