Definition and Purpose of Form 1065

Form 1065, also known as the U.S. Return of Partnership Income, is used by partnerships in the United States to report their financial information to the IRS. For the 2014 tax year, it requires reporting a partnership’s income, deductions, credits, and other significant financial details. The purpose of this form is to ensure that partnerships accurately declare financial activities as they affect each partner's tax obligations, allocating profits and losses among them.

Detailed Breakdown of the Form

Form 1065 is composed of several sections, each capturing different financial aspects of a partnership. Key elements include:

- Income: Details on gross receipts or sales, cost of goods sold, and total income.

- Deductions: Lists potential business expenses such as salaries, wages, and interest expenses.

- Tax and Payments: Information about tax due and any payments made.

Application and Compliance

Filling out Form 1065 accurately is crucial as partnerships do not pay taxes at the entity level; instead, profits and losses are passed through to partners. Completing this form correctly informs individuals about their share of earnings, guiding them in filing their personal tax returns. Partnerships must ensure compliance to avoid penalties and ensure each partner pays the correct amount of taxes on their share of the income.

Steps to Complete Form 1065 for 2014

Completing Form 1065 involves a multi-step process that partnerships must follow diligently to ensure accuracy and compliance.

- Collect Financial Information: Gather all pertinent data on the partnership's income, deductions, and credits.

- Fill Out Basic Information: Enter the partnership name, address, employer identification number, and type of return.

- Detail Income and Deductions: Provide comprehensive data on total income and allowable deductions.

- Complete Schedule K: Summarize the total income, credits, and other financial activities distributable to partners.

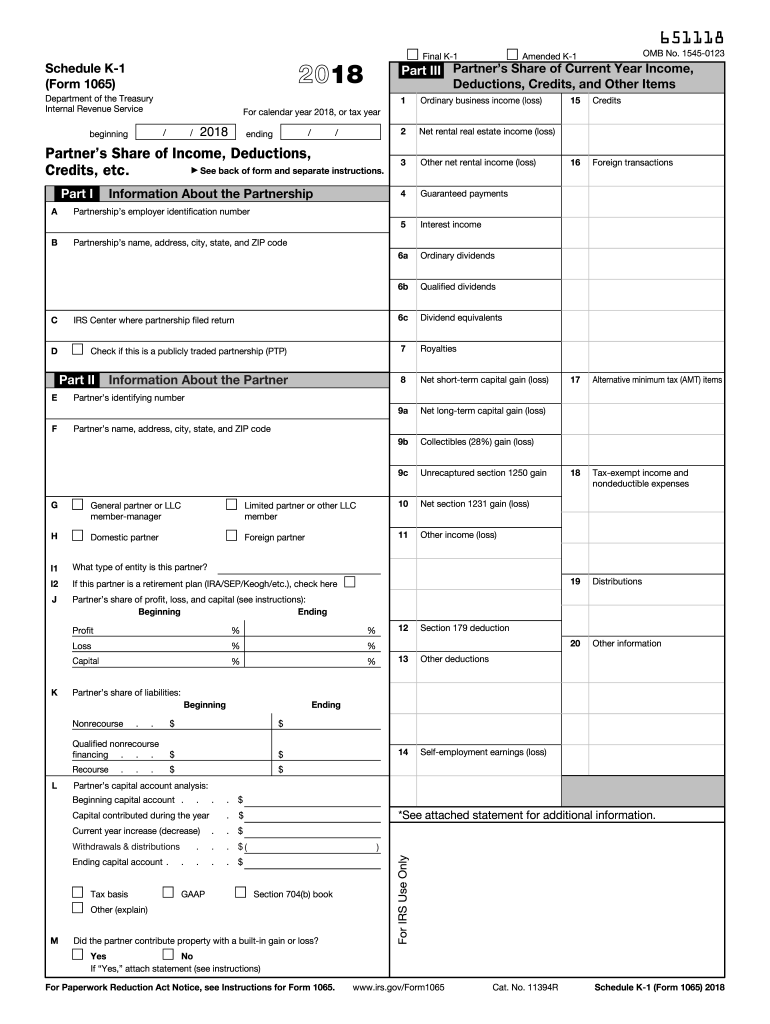

- Prepare Schedule K-1: Allocate financial data on a Schedule K-1 for each partner, detailing their respective shares of the income and deductions.

- Review and Submit: Ensure all information is accurate, complete any necessary schedules, and file the form by the tax deadline.

Filing Deadlines and Important Dates

For the 2014 fiscal year, partnerships needed to file Form 1065 by March 16, 2015. Filing on time is essential to avoid late penalties. If more time was needed to compile the necessary information, partnerships could have filed for an extension, which provided until September 15, 2015, to submit the complete form.

Important Terms Related to Form 1065

Understanding certain key terms is fundamental in effectively handling Form 1065.

- Partnership: A business agreement between two or more parties who share profits and losses.

- Partner: An individual or entity participating in the partnership with defined shares of income and losses.

- Schedule K-1: A document associated with Form 1065, provided to each partner to report their share of the earnings and deductions.

Conceptual Clarification

For example, a partnership might consist of three partners: two individuals and one corporation. Each partner receives a Schedule K-1 outlining their portion of the income and expenses, which they subsequently use when filing their individual or corporate tax returns.

Legal Use and Compliance with Form 1065

Legal adherence to Form 1065 processes ensures correct payment of taxes and limits liability for inaccuracies that can attract penalties. Partnerships must follow IRS guidelines diligently to prepare and file the form, ensuring they maintain records that can verify income and deductions reported.

IRS Guidelines for Compliance

- Ensure accuracy in reported income and deductions.

- Timely filing and submission of the form.

- Distribution of Schedule K-1 to each partner in a timely manner.

Partners should consult with tax professionals or use reputable tax software to ensure compliance and accuracy.

Form Submission Methods: Paper vs. Electronic

Partnerships can submit Form 1065 through traditional mail or electronically. Each method has its benefits and considerations.

- Paper Submission: Traditional, involves mailing the completed form to the IRS. Provide proof of mailing in the form of registered mail or similar.

- Electronic Filing: Faster and often more secure, with immediate confirmation of receipt by the IRS. Recommended for its efficiency and error-checking capabilities.

Electronic filing is usually preferred for its speed and the convenience of direct confirmation from the IRS.

Potential Penalties for Non-Compliance

Failing to comply with IRS requirements can lead to significant penalties for a partnership. Common infractions include late filing, providing incorrect information, or failing to furnish Schedule K-1 to partners on time. Each violation brings a financial penalty, underscoring the importance of careful adherence to filing procedures.

Specific Penalties Explained

- Late Filing: A fine imposed for failing to file by the deadline without requesting an extension.

- Incorrect Information: Penalties for inaccuracies in reported income or deductions, affecting both the partnership and individual partners.

Ensuring compliance is vital to minimizing financial penalties and maintaining a smooth filing process.