Definition and Purpose of Form 14157

Form 14157, established in 2014, serves as a formal avenue for filing complaints with the IRS against tax return preparers or tax preparation firms. It is an essential tool for taxpayers seeking to report misconduct or malpractice in tax preparation services. The form specifically addresses potential violations of tax laws, fostering compliance among tax preparers. By documenting grievances, this form aids the IRS in investigating and enforcing regulations to maintain the integrity of tax administration.

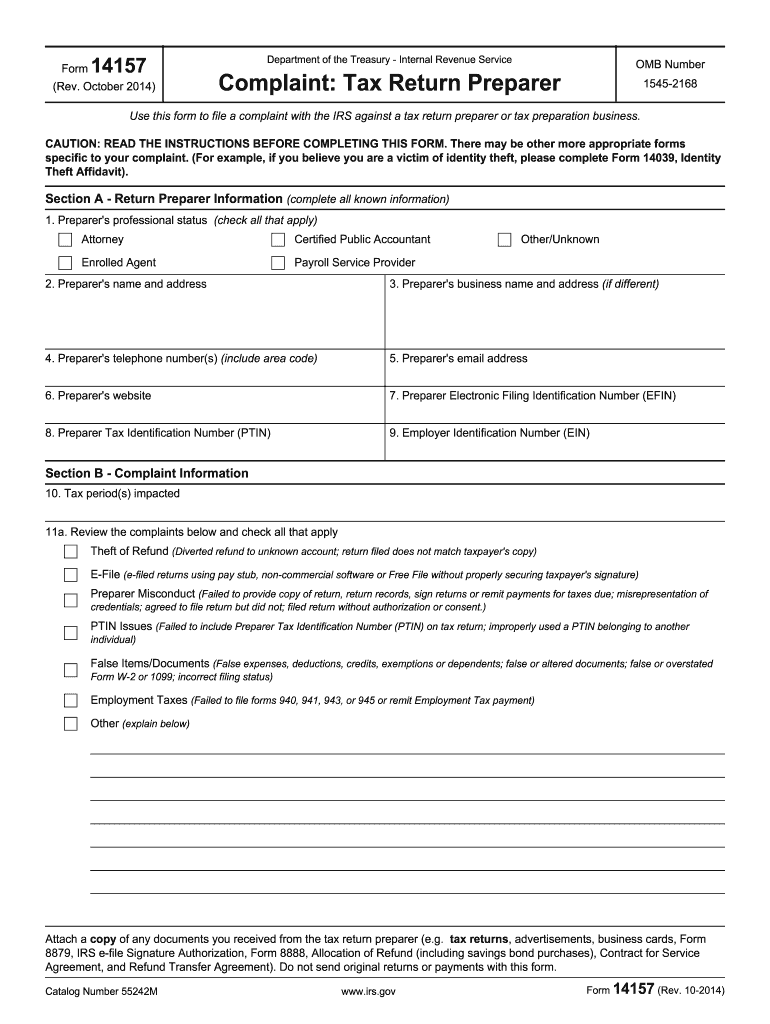

Key Elements of the Form

Form 14157 comprises several critical sections designed to capture comprehensive information:

- Preparer Information: Details of the tax preparer or firm in question, including name, address, and PTIN (Preparer Tax Identification Number).

- Complaint Details: A narrative section allowing the taxpayer to describe the misconduct or issue in detail.

- Taxpayer Information: The complainant provides personal information for follow-up.

- Supporting Documentation: Attachments of any evidence, such as correspondence, receipts, or erroneous tax filings, to back the complaint.

Understanding these elements is crucial for effectively completing and submitting the form to ensure the IRS receives the necessary information for investigation.

How to Use Form 14157

Publishing a complaint using Form 14157 involves several key steps:

- Collect Information: Gather all relevant details about the tax preparer and the nature of the complaint.

- Fill Out the Form: Enter your personal information, the preparer's details, and specific complaint information.

- Attach Evidence: Include any supporting documents that substantiate your complaint.

- Submit to the IRS: Choose a suitable submission method — either by mail or electronic submission if available.

This process emphasizes transparency and accuracy to facilitate proper handling and resolution of complaints.

Steps to Complete Form 14

Filing Form 14157 requires meticulous attention to detail:

-

Section One – Preparer’s Information:

- Provide the name, address, and identification numbers of the tax preparer.

-

Section Two – Complaint Details:

- Clearly state the nature of the misconduct, including dates and outcomes.

-

Section Three – Your Information:

- Enter your personal data, ensuring all contact information is up-to-date if IRS follow-up is needed.

-

Section Four – Evidence Submission:

- Attach documentation supporting your claim such as emails or financial statements.

-

Verification and Signature:

- Sign the form to authenticate your complaint before submission.

Following these steps ensures that your complaint is precise and complete, allowing for effective IRS intervention.

Who Typically Uses Form 14157

Form 14157 is primarily utilized by:

- Individual Taxpayers: Those who suspect wrongdoings by their tax preparer or errors in their processed returns.

- Tax Professionals: Tax consultants and advisors who identify malpractice and wish to uphold industry standards.

- Consumer Advocacy Groups: Entities that act on behalf of clients who have experienced misconduct.

This form empowers these groups to hold tax professionals accountable for their actions, contributing to a fairer tax system.

Legal Use and IRS Guidelines

The legal foundation of Form 14157 lies in its alignment with IRS regulatory standards:

- Compliance with IRS Procedure: Ensures that complaints are systematically reviewed and resolved in accordance with legal and procedural protocols.

- Confidential Handling: The IRS guarantees confidentiality for all submissions, safeguarding complainants' identities.

- Adherence to E-Sign Act: Digital signatures comply with federal laws ensuring legal legitimacy.

These guidelines are critical for maintaining trust and integrity within the tax filing landscape.

Filing Deadlines and Important Dates

While Form 14157 itself does not have an explicit deadline, timely submission is advisable to expedite the resolution process. Taxpayers should aim to file as soon as a discrepancy is identified. Key tax season dates, such as filing deadlines, can impact the processing time and should be taken into consideration when filing a complaint to the IRS.

Penalties for Non-Compliance

Filing Form 14157 is an essential step in addressing tax preparer misconduct, as failure to report such issues can lead to the perpetuation of errors:

- Tax Liability: Incorrect filing might result in increased tax liabilities or missed refunds.

- Legal Implications for Preparers: Tax preparers may face sanctions, fines, or revocation of their filing privileges if found non-compliant.

These outcomes underscore the importance of using Form 14157 to correct preparer misconduct and protect taxpayer interests.

Submission Methods for Form 14157

Form 14157 can be submitted using various methods:

- Mail: Send the completed form and any attachments to the designated IRS address for manual processing.

- Digital Channels: If available, electronic submission options offer a faster, more secure way to deliver your complaint.

Each method has distinct benefits, with digital submissions providing faster delivery and simplified tracking of form status.