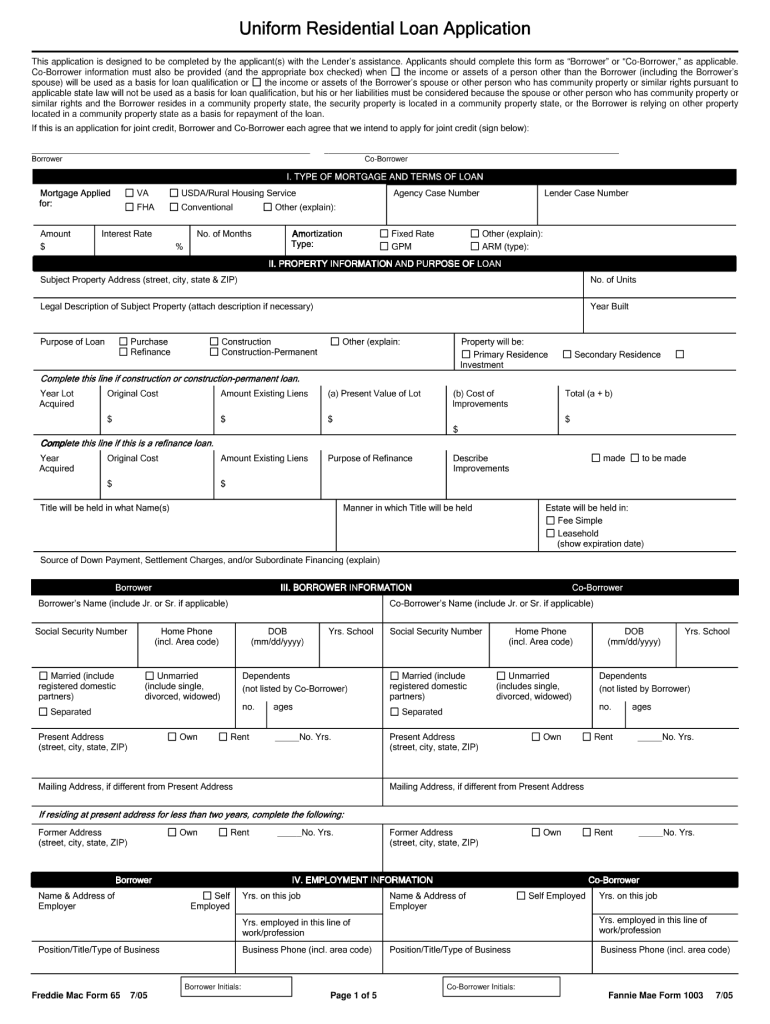

Definition and Purpose of the New 1003 Loan Application

The new 1003 loan application, often referred to as the Uniform Residential Loan Application (URLA), is a standard form used by lenders in the United States to evaluate mortgage loan applicants. Its purpose is to uniformly collect necessary financial and personal information from borrowers, assisting lenders in processing and underwriting loan applications efficiently. The redesigned 2021 version of this form includes updates that aim to streamline the information-gathering process, making it more user-friendly while ensuring compliance with governmental regulations.

Components of the 1003 Loan Application

-

Personal Information: This section requires the borrower's name, address, and contact information. Borrowers must also provide details about their marital status and the number of dependents.

-

Income Information: Applicants must detail their income sources, including salary, bonuses, and other forms of income. This information is critical for assessing the borrower's ability to afford loan repayments.

-

Asset Declaration: Borrowers need to list their assets, including bank account balances, investments, and any other financial assets. This section helps lenders evaluate overall financial health.

-

Loan and Property Details: This part of the application captures information about the property being financed or purchased and the specific loan requested.

Steps to Complete the New 1003 Loan Application

Completing the new 1003 loan application requires careful attention to detail. Here are the steps borrowers should follow to ensure accuracy:

-

Gather Necessary Documentation: Collect required documents such as W-2 forms, pay stubs, bank statements, and tax returns. These documents will help substantiate the information on the application.

-

Enter Personal Information: Fill out the first section with your personal details and those of any co-borrowers, ensuring that names are spelled correctly and contact information is up-to-date.

-

Detail Income: Provide comprehensive income details. This may involve monthly income calculations and listing any additional income sources, including rental payments or alimony.

-

List Assets and Liabilities: Accurately report assets and liabilities. Ensure that all debts, such as credit cards and other loans, are disclosed, as this will affect the debt-to-income ratio assessment.

-

Review and Sign: After filling out the application, review all sections for errors or omissions. Once confirmed, sign the application and prepare it for submission to the lender.

Benefits of Using a Fillable 1003 Form

The fillable version of the 1003 form offers several advantages over traditional paper forms:

-

Convenience: Users can complete the application from any device with internet access, making it easy to fill out at their own pace.

-

Error Reduction: Fillable forms often include validation checks that reduce common errors, ensuring that no crucial information is overlooked.

-

Easy Submission: Once completed, the application can often be submitted electronically, expediting the loan process and eliminating the need for physical mailing.

Important Sections of the 1003 Application

Each section of the 1003 application plays a vital role in assessing creditworthiness and loan eligibility. Understanding these sections helps to prepare applicants for inquiries during the approval process:

-

Declarations: Borrowers must respond to specific questions about their financial history, including any bankruptcies or foreclosures, which can impact approval.

-

Mortgage and Loan Terms: This section outlines the type of mortgage requested, loan amount, interest rate, and duration. Clear parameters here help lenders assess the risk involved.

-

Additional Borrower Information: If there are multiple borrowers, each must provide personal and financial details, as their combined information can strengthen the application.

Legal Considerations of the 1003 Form

The 1003 loan application complies with federal regulations and guidelines set forth by agencies like Fannie Mae and Freddie Mac. Adhering to these regulations is crucial for ensuring that lenders process applications fairly and without discrimination. Borrowers should be aware of their rights under laws such as the Equal Credit Opportunity Act, which protects against discrimination based on race, color, national origin, religion, sex, marital status, or age.

Common Scenarios Involving the 1003 Application

Many borrowers will encounter unique situations when completing the 1003 application:

-

Self-Employed Individuals: Those who are self-employed may need to provide additional documentation, such as profit and loss statements, to validate income.

-

Non-Traditional Income Sources: Applicants who receive income from rental properties or investments should be prepared to document and explain these income streams thoroughly.

-

First-Time Home Buyers: First-time home buyers may have specific programs available to them, requiring an understanding of different eligibility criteria that may appear on the application.

By focusing on these essential blocks of the new 1003 loan application, borrowers can navigate the mortgage process effectively, understanding the importance of each component while ensuring a smooth application experience.