Definition and Meaning of Schedule K-1 (Form 1065)

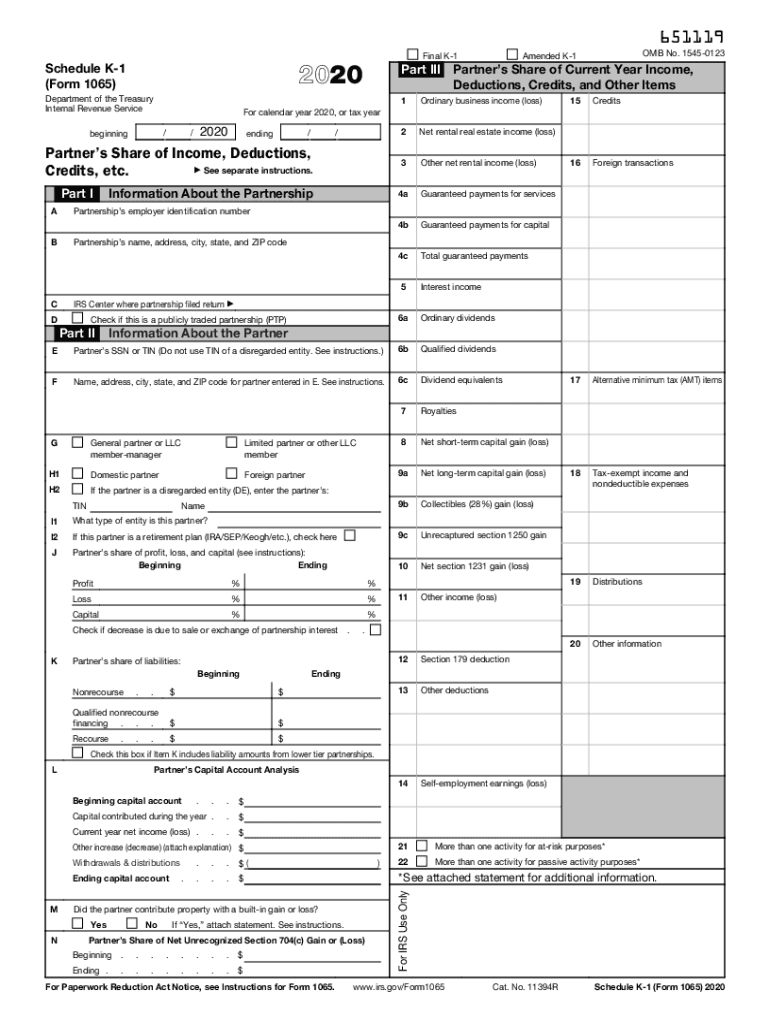

The Schedule K-1 (Form 1065) is issued by the Internal Revenue Service (IRS) to report a partner's share of income, deductions, credits, and other items from a partnership. It is a crucial form within the U.S. tax system, as it facilitates the distribution of financial information from partnerships to their partners. Each partner uses this information to report their share of the partnership's income on their individual tax return. The form includes details about ordinary business income, guaranteed payments, interest income, and dividends.

Key Components of Schedule K-1

- Partner Information: Includes basic identification data such as the partner's name and taxpayer identification number.

- Income and Deductions: Lists the partner's share of various types of income and deductions, critical for accurate tax reporting.

- Capital Account Analysis: Provides a summary of the partner’s beginning and ending capital account balance, which is essential for understanding investment value changes.

How to Use the Schedule K-1 Form

Using the Schedule K-1 correctly involves understanding each section and accurately reporting the information on your tax return. The form is designed for clarity, ensuring that partners can match the data with corresponding sections on their 1040 tax return.

- Identify Relevant Sections: Determine which parts of the Schedule K-1 apply to your situation. Ordinary income, capital gains, and any special deductions should be noted.

- Transfer Information to Tax Return: Accurately transfer the reported information to the corresponding lines on your Form 1040, ensuring consistency and accuracy.

- Consult the IRS Instructions: The IRS provides detailed instructions for Schedule K-1, offering line-by-line assistance to help you understand each field.

Steps to Complete the Schedule K-1

Successfully completing the Schedule K-1 involves following specific steps to ensure all financial data is accurately captured and reported.

- Collect Necessary Financial Data: Gather all financial documents related to the partnership’s activities during the tax year.

- Complete Income and Expense Details: Fill in the sections for income, such as business income and dividends, and any deductions your partnership has incurred.

- Verify Capital Account Updates: Ensure your capital account changes are correctly recorded, which include allocations for profits, losses, and distributions.

- Consult with a Tax Professional: Given the complexity of tax legislation, consider consulting a tax advisor to verify the accuracy of the form and ensure compliance with IRS requirements.

Importance of the Schedule K-1 Form

The Schedule K-1 is vital for ensuring that a partner's tax liabilities are calculated based on their actual share of the partnership's financial activities. It promotes transparency and ensures that all income types and deductions are accounted for.

- Transparency: Provides partners with a clear view of their share in the partnership's financial activities.

- Compliance: Helps prevent errors in personal tax filing by providing structured guidelines for reporting partner income and expenses.

- Financial Overview: Aids partners in understanding their fiscal position as part of the partnership, including potential tax obligations or refunds.

Who Typically Uses the Schedule K-1 Form

The Schedule K-1 Form is typically used by individuals who are partners in a partnership or members of certain pass-through entities such as S corporations.

Common Users

- Business Partners: Individuals who have invested in partnerships and need to report their share of income, losses, and credits.

- Members of LLCs: Those in Limited Liability Companies (LLCs) that are treated as partnerships for tax purposes.

- S Corporation Shareholders: Shareholders of S corporations receive a similar form, allowing them to account for their share of the entity's income.

Key Elements of the Schedule K-1 Form

Understanding the key components of the Schedule K-1 is essential for accurate reporting and compliance.

- Ordinary Business Income: Reportable income from partnership operations, excluding investment income.

- Capital Gains: Gains or losses derived from the sale of partnership assets.

- Guaranteed Payments: Payments made to partners for services or the use of capital, regardless of the partnership's profitability.

- Credits and Deductions: Tax credits and deductible amounts that may affect the partner’s individual tax obligations.

IRS Guidelines for Schedule K-1

The IRS provides specific guidelines for handling and filing Schedule K-1. Compliance with these guidelines is essential to avoid errors or penalties.

- Filing Requirements: Partnerships must file a Form 1065, along with individual Schedule K-1 forms for each partner.

- Timing: Forms must be provided to partners by the due date of the partnership's return, which is March 15 for calendar-year filers.

- Documentation: All relevant financial documentation and calculations should be retained to support the information provided on the form.

Penalties for Non-Compliance

Failure to comply with IRS rules regarding the Schedule K-1 can result in significant penalties for both the partnership and individual partners.

Potential Penalties

- Late Filing Penalties: For partnerships that fail to file Form 1065 on time, a penalty may be assessed per partner per month for each month the return is late.

- Incorrect Information Penalties: Providing inaccurate information can lead to penalties, emphasizing the need for accuracy and diligence when completing the form.

- Additional IRS Scrutiny: Non-compliance may increase the likelihood of IRS audits, which can further complicate tax obligations.

Taxpayer Scenarios Involving Schedule K-1

The Schedule K-1 is applicable in various taxpayer scenarios, each with distinct compliance and reporting requirements.

Common Scenarios

- Self-Employed Individuals: Partners who derive their primary income from partnership operations.

- Retirees with Partnership Investments: Retired individuals receiving income from past investments in partnerships.

- Students with Partnership Interests: Students who have inherited partnership stakes and must report income, even without direct management involvement.