Definition and Meaning of Schedule K-1 (Form 1041) for 2016

The Schedule K-1 (Form 1041) for the 2016 tax year is used by estates and trusts to report a beneficiary's share of income, deductions, credits, and other items. This form is critical for beneficiaries to accurately prepare their individual tax returns. It includes detailed sections that address various types of income, such as dividends, capital gains, and rental income. Each section provides specific instructions for reporting these amounts on federal income tax returns. Understanding the nuances of the 2016 Schedule K-1 form is essential for both beneficiaries and those responsible for administering estates or trusts.

How to Use the 2016 Schedule K-1 Form

To effectively use the 2016 Schedule K-1 form, beneficiaries should focus on accurately transcribing the information provided into their tax return forms. Here are essential steps to ensure proper usage:

-

Review each section: Look at the detailed breakdown of income categories and attributes specified by the estate or trust.

-

Incorporate income types: Make sure each type of income reported on the K-1, such as dividends or rental income, is correctly included on corresponding line items of personal tax forms like the 1040.

-

Transfer deductions and credits: Some forms of deductions and credits reported on the K-1 may directly impact your total tax liability and should be factored accurately.

-

Consult the IRS guidelines: The IRS provides specific instructions on how to report items from a K-1, which helps avoid errors in reporting.

Steps to Complete the 2016 Schedule K-1 Form

Those responsible for filling out the 2016 K-1 form must carefully follow a sequence of steps:

-

Accumulate relevant income data: Gather all income received or accrued by the estate or trust during the year.

-

Detail deductions and credits: Calculate and note any deductible expenses or credits generated through trust or estate activities.

-

Allocate income and deductions: Properly distribute these amounts to beneficiaries according to the trust or estate agreement stipulated.

-

Validate all information: Ensure accuracy of the entered data to reduce errors and potential IRS scrutiny.

-

Sign and distribute: After completion, distribute the finalized K-1 form to beneficiaries for their tax returns.

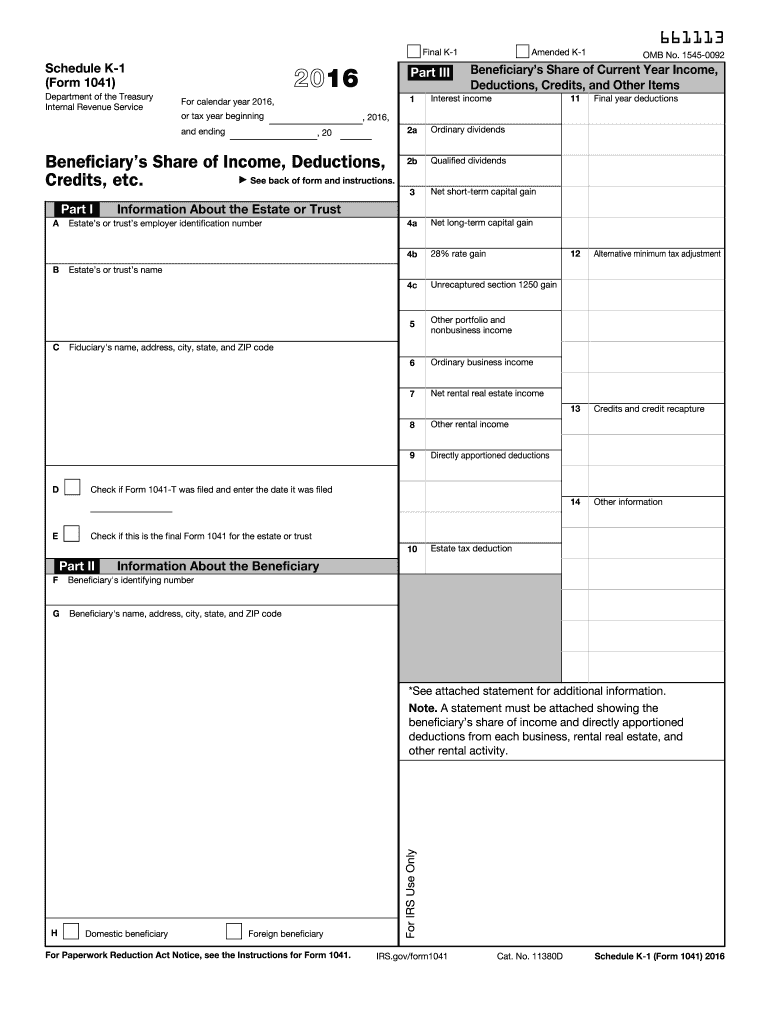

Key Elements of the 2016 Schedule K-1 Form

The 2016 Schedule K-1 form includes different sections that provide extensive information crucial for tax reporting:

-

Part I - Information about the Estate or Trust: Details about the entity providing the K-1, including its name, address, and Tax Identification Number (TIN).

-

Part II - Information about the Beneficiary: Beneficiary’s identity details, such as Social Security Number and address.

-

Part III - Beneficiary’s Share of Current Year Income, Deductions, Credits, and Other Items: Comprehensive breakdown of all income categories, deductions, and credits applicable to the beneficiary.

Understanding these elements helps in the completion and review process, ensuring compliance and accurate tax reporting.

Important Terms Related to the 2016 Schedule K-1 Form

Certain terms are vital to understanding and using the 2016 Schedule K-1 form effectively:

-

Trust: A fiduciary arrangement allowing a third party to hold assets on behalf of beneficiaries.

-

Beneficiary: An individual who receives income or assets from a trust or estate.

-

Fiduciary: A person legally appointed to manage and protect assets for another party.

Those dealing with Schedule K-1 should familiarize themselves with these and other related terms to navigate the form efficiently.

IRS Guidelines for the 2016 Schedule K-1 Form

According to IRS guidelines, entities issuing the 2016 Schedule K-1 form must ensure its distribution to beneficiaries. Beneficiaries should report amounts accurately on their income returns, following IRS instructions:

-

Reporting Income: Various sections of the form dictate where to report particular types of income on individual tax returns.

-

Due Dates: Typically, the Schedule K-1 must be received by the beneficiary in alignment with other tax return deadlines, commonly by April 15.

-

Handling Errors: If errors in data are found, both issuers and beneficiaries should follow IRS procedures for amendments.

These guidelines promote accuracy and compliance with federal tax regulations.

Penalties for Non-Compliance

The IRS enforces penalties for non-compliance related to the Schedule K-1 form:

-

Late Filing or No Submission: Failure to file the form appropriately or within due deadlines can lead to monetary fines.

-

Inaccurate Reporting: Providing false or erroneous data can result in penalties, including interest charges or additional fees.

Understanding and adhering to filing requirements helps avoid these repercussions.

Digital vs. Paper Version of the 2016 Schedule K-1 Form

With the advancement of technology, the choice between digital and paper versions of the 2016 Schedule K-1 is significant:

-

Digital Submission: Allows for quicker completion and distribution but requires access to appropriate software and electronic filing platforms.

-

Paper Form: While traditional, it may be necessary for those without digital capabilities. Completing and mailing physical forms remains an option.

Individuals and entities must decide the best format that suits their needs, considering the potential convenience and efficiency of digital over paper.

Who Typically Uses the 2016 Schedule K-1 Form?

The 2016 Schedule K-1 form is most often utilized by:

-

Beneficiaries of Estates and Trusts: Individuals inheriting assets or income from these entities are required to incorporate K-1 data into their personal tax returns.

-

Estate and Trust Administrators: Responsible for generating and distributing the form, ensuring accurate representation of income distribution.

By understanding the typical users, the form's application can be more accurately predicted and utilized in tax preparation.