Definition and Function of the 2009 Form 941

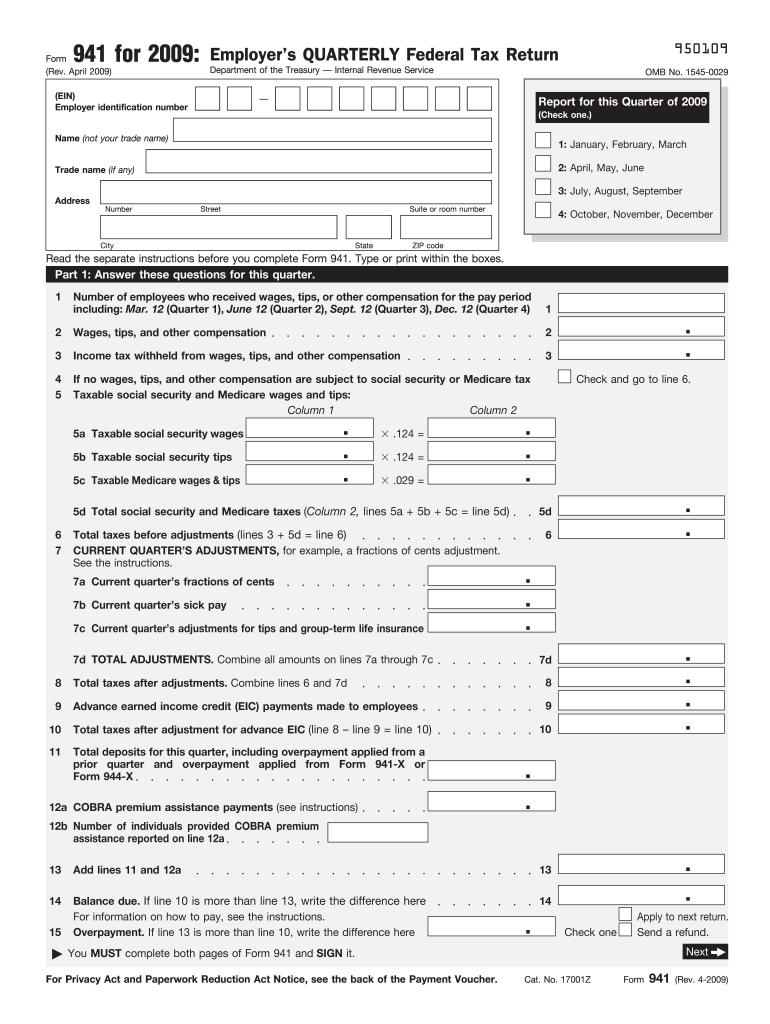

The 2009 Form 941, officially known as the Employer's Quarterly Federal Tax Return, is utilized by employers in the United States to report wages, tips, and other forms of compensation paid to employees. It also details the federal tax withholdings, including income, social security, and Medicare taxes from these wages. The form is vital for ensuring compliance with federal tax regulations, as it helps the IRS track tax liabilities and payments made throughout the year.

How to Obtain the 2009 Form 941

Securing a copy of the 2009 Form 941 is straightforward. Employers can access this form through the IRS website, where they can download and print it for free. Alternatives include requesting a physical copy directly from the IRS, though this may take additional time. Some tax preparation software might also include historical forms, like the 2009 version, for convenience.

Steps to Complete the 2009 Form 941

Filling out the 2009 Form 941 involves several specific steps:

-

Enter Employer Information: Include the employer’s name, address, and Employer Identification Number (EIN).

-

Report Employee Wages and Taxes: Document total wages paid, as well as federal income taxes withheld.

-

Calculate Tax Liability: Detail social security and Medicare taxes due, including any adjustments needed for current and prior quarters.

-

Adjustments for Prior Quarters: Include adjustments for fractions of cents, sick pay, tips, and group-term life insurance.

-

Deposit Schedule and Tax Liability for the Quarter: Report the tax deposit schedule and tax liability for each month of the quarter.

-

Sign and Date: Ensure the form is signed by an authorized individual before submission.

Key Elements of the 2009 Form 941

This form comprises essential sections that need careful completion:

-

Part 1: Contains questions about the number of employees and payroll details.

-

Part 2: Focuses on the tax deposit schedule and the quarterly tax liability.

-

Part 3: Requests additional information like adjustments and any overpayments.

-

Part 4: Designation of a third-party designee if applicable.

Legal Use and Compliance of the 2009 Form 941

Employers must accurately report all employee compensation and associated tax liabilities on Form 941 to maintain legal compliance. Failing to submit the form or misreporting information can lead to significant legal consequences, including fines and penalties. The form serves as an acknowledgment of the employer's responsibility to withhold and pay federal taxes on behalf of their employees.

Filing Deadlines for the 2009 Form 941

Form 941 is a quarterly filing requirement, with deadlines falling at the end of the month following the quarter's end:

- First Quarter: April 30

- Second Quarter: July 31

- Third Quarter: October 31

- Fourth Quarter: January 31 of the following year

Timely filing ensures compliance and avoids potential penalties.

Penalties for Non-Compliance

Failure to file the 2009 Form 941 or late submission can result in penalties. The IRS may impose fines that accumulate over time, based on the duration of the delay and the outstanding tax amount. Employers can also face penalties for unpaid taxes or filing inaccuracies, underscoring the importance of careful form completion and on-time submission.

Business Entity Types That Use the 2009 Form 941

Several types of business entities are required to file Form 941. These include:

- Corporations and LLCs that have employees.

- Partnerships engaging in payroll activities.

- Small businesses and startups with workforce wages to report.

Each entity must accurately complete the form to reflect their specific wage reporting and tax responsibilities.