Definition and Purpose of Form 8

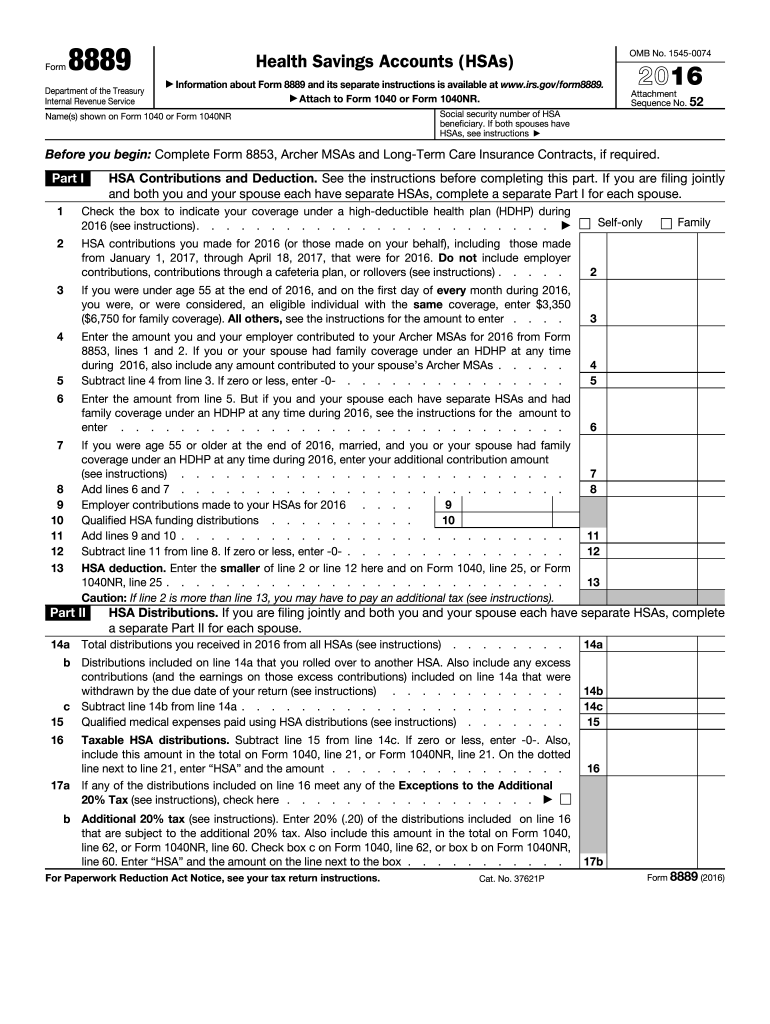

Form 8889, officially titled "Health Savings Accounts (HSAs)," is an IRS tax form for reporting contributions, deductions, and distributions related to HSAs during the 2014 tax year. It encompasses sections for inputting details about contributions made to HSAs, distributions received from HSAs, and any additional taxes applicable due to not maintaining a High Deductible Health Plan (HDHP). This form is essential for taxpayers who have HSAs as part of their healthcare savings strategy.

Practical Examples

- Contributions: If you contributed to an HSA in 2014, you'll report these contributions here, whether they are made by you, your employer, or a third party.

- Distributions: Any money withdrawn from your HSA for qualified medical expenses must be recorded in the appropriate section.

- Additional Taxes: If you used HSA funds for non-qualified expenses, you may owe additional taxes, which are to be documented on this form.

How to Use Form 8

To correctly use Form 8889, a taxpayer must:

-

Gather Information: Collect information on all HSA-related transactions in the 2014 tax year, including contributions and withdrawals.

-

Follow IRS Instructions: Consult the IRS instructions specific to Form 8889 for guidance on filling out each section accurately.

-

Determine Tax Implications: Identify any additional taxes applicable due to non-qualified medical expenses from HSA distributions.

Real World Scenario

Imagine you've contributed $3,000 to your HSA account in 2014. You must report this amount, indicating whether contributions have been made by you or your employer. If you withdrew funds to pay for healthcare services, like a hospital visit or doctor's consultation, these need reporting as distributions, ensuring they align with eligible medical expenses.

Steps to Complete Form 8

Completing Form 8889 involves several systematic steps:

-

Part I – Contributions: Fill in details of contributions made to your HSA during 2014. This includes reporting any employer contributions and contributions made on your behalf.

-

Part II – Distributions: Document any distributions received from your HSA. Confirm that these withdrawals were used for qualifying medical expenses.

-

Part III – Additional Tax: Calculate any additional tax for distributions not used for qualified medical expenses and note exemptions if applicable.

Detailed Breakdown

- Required Information: Include total contributions, deductible contributions, and employer contributions in Part I.

- Assess Distributions: Ensure all distributions align with IRS definitions of qualified medical expenses.

- Calculate Penalties: Apply additional taxes to non-qualified expenses at 20% of the total distribution amount, except in specific instances like disability or reaching age 65.

Important Terms Related to Form 8

Understanding key terms is crucial when dealing with Form 8889:

- HSA (Health Savings Account): A tax-advantaged account used to pay for or reimburse qualifying medical expenses.

- HDHP (High Deductible Health Plan): A health insurance plan with lower premiums and higher deductibles than a typical health plan, integral to maintaining an HSA.

- Qualified Medical Expenses: As defined by the IRS, these include expenses for healthcare services, equipment, and medications.

Examples of Qualified Expenses

- Prescribed medications

- Doctor's visits

- Surgeries

- Certain therapy services

Filing Deadlines and Important Dates

Meeting filing deadlines is critical to avoid penalties:

-

Standard Filing Deadline: The form should be submitted alongside your individual tax return for the 2014 tax year, typically due by April 15, 2015.

-

Extensions: Although an extension might be filed for the overall tax return, the specific deadlines for HSA contributions could differ.

Pro Tip

To maximize HSA benefits, contributions for the 2014 tax year are allowed up until the standard tax filing deadline in April 2015. Be sure to capitalize on this opportunity for additional tax savings.

IRS Guidelines on Form 8

The IRS provides specific guidelines to ensure compliance:

-

Comprehensive Instructions: IRS Publication 969 can offer extensive detail on HSAs, including eligibility requirements, rules for contributions and distributions, and tax implications.

-

Amendments and Corrections: If errors are discovered after initial submission, filing an amended return using Form 1040-X may be necessary.

Example of IRS Compliance

A taxpayer utilizing an HSA for non-qualified expenses will find this reported under Part III for additional taxes. The IRS guidelines require a precise calculation of the additional tax incurred.

Penalties for Non-Compliance

Non-compliance with Form 8889 requirements can result in penalties:

-

Distribution Penalties: Withdrawals for non-qualified expenses are subject to income tax and a 20% additional tax.

-

Missed Contributions: Over-contributions to an HSA may lead to excise taxes unless corrected within a specific timeframe defined by the IRS.

Edge Case

If contributions exceeded permissible limits due to employer error, you can petition for an excess contribution correction to prevent penalties.

Digital vs. Paper Version

Choosing between digital and paper submissions of Form 8889 can affect ease and speed:

-

Digital Submissions: Often simpler and faster, allowing for direct e-filing and integration with tax software such as TurboTax or QuickBooks.

-

Paper Submissions: Require mailing to IRS, possibly resulting in longer processing times.

Software Compatibility

Ensure that your chosen tax software supports Form 8889 for seamless e-filing, reducing chances for user error and improving accuracy.